PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550313

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550313

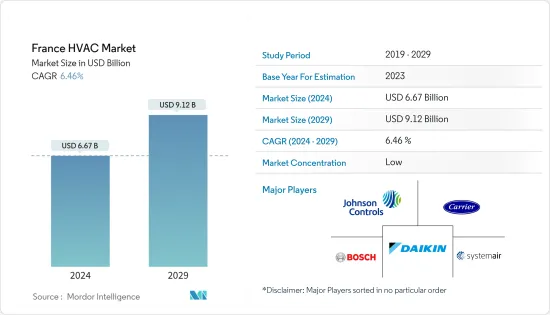

France HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The France HVAC Market size is estimated at USD 6.67 billion in 2024, and is expected to reach USD 9.12 billion by 2029, growing at a CAGR of 6.46% during the forecast period (2024-2029).

Key Highlights

- France has implemented stringent energy efficiency regulations, such as RT and RE, which set high standards for the energy performance of buildings. These regulations promote using energy-efficient HVAC systems to reduce energy consumption and carbon emissions. According to Eurostat, France's final energy demand is attributed mainly to heating and cooling (H&C), accounting for 45% of the total. Surprisingly, households consume approximately 30% of the country's energy, surpassing the industrial sector. The government's dedicated efforts to improve energy efficiency techniques will drive the French HVAC market forward.

- The demand for HVAC systems in France is steadily increasing, driven by climate change, urbanization, and rising living standards. The commercial sector, including office buildings and retail spaces, is also contributing to the growing market for HVAC systems. Moreover, the trend toward renovating and retrofitting existing buildings amplifies the necessity for HVAC upgrades, aligning with modern energy-saving technologies.

- The country is contributing considerably to market growth, primarily due to the increase in urban population, which generates significant demand for HVAC equipment and services. In 2023, the total population of France amounted to over 68 million. The Ile-de-France region was the most populous region in France in the same year. INSEE said more than 12 million French citizens lived in the Ile-de-France. The ile-de-France region was followed by the Auvergne-Rhone-Alpes and Nouvelle-Aquitaine regions in the southern part of the country.

- Furthermore, the demand for new industrial facilities, office buildings, multifamily properties, data centers, and advanced technology manufacturing spaces is soaring. Several organizations are expanding their office space in the country, which will further create high demand for HVAC equipment and services.

- Inflation and supply chain disruptions drive up raw material costs, directly impacting manufacturing costs for HVAC systems. Notably, essential materials like steel, copper, and aluminum are witnessing significant cost hikes, further burdening HVAC manufacturers. As a result, small- and mid-sized HVAC companies face margin limitations, directly impacting profits and hindering the ability to invest in R&D (research and development). This, in turn, hampers the market's growth potential.

- France's macroeconomic landscape saw no respite. It grappled with persistently high inflation and interest rates and looming fears of recession amid escalating geopolitical tensions. This backdrop of uncertainty has left consumers across various sectors exercising caution. While a market rebound is anticipated, its timing and trajectory remain ambiguous. In addition, programs offering financial incentives for retrofitting old systems with new, efficient ones boost market growth.

France HVAC Market Trends

Residential Sector to Witness a Significant Growth

- The growth of the market can be attributed to factors like a strong preference for electric heating systems over gas, a domestic air conditioning industry that has transitioned to heat pumps, and the implementation of government initiatives to promote heat pump installation, including grant schemes like FranceRenov which provides up to EUR 10,000 (USD 10,884.45) per household. New energy-efficiency standards for new homes have also played a role in France's achievements. Moreover, the rise in residential construction in France is expected to drive the market.

- For instance, in September 2023, France spearheaded a push to transition from traditional residential fuel and gas heaters to heat pumps, aiming to establish a domestic industry for these devices. This initiative forms a pivotal part of France's comprehensive, multi-year environmental strategy. The country is looking to retire its last few coal-fired power plants, actively advocating for a shift from thermal engines to electric vehicles and promoting heat pumps as the primary heating solution for households.

- The desire to lower carbon footprints and the rising awareness of environmental concerns lead homeowners to invest in eco-friendly HVAC systems, energy-efficient and renewable energy-based HVAC solutions, such as heat pumps and solar-powered systems, which are becoming more popular in the country. According to Insee, more residential buildings were constructed in terms of floor space in France during the first 10 months of 2023 than non-residential buildings.

- The country's residential HVAC sector has seen a consistent uptick in demand for energy-efficient heating and cooling systems. This growth is primarily propelled by escalating energy costs and government incentives that encourage energy-efficient home upgrades. For instance, in April 2024, the French government officially allocated nearly EUR 1 billion (USD 1.09 billion) to fund the development of 75,000 intermediate housing units. This initiative is part of a broader strategy to address the pressing need for 500,000 more homes nationwide in the coming three years.

HVAC Equipment is Expected to Hold Significant Market Share

- France has stringent energy efficiency regulations and environmental standards for buildings, which drive the demand for HVAC equipment. Building operators and owners must comply with these regulations by implementing energy-efficient heating and cooling systems, ventilation solutions, and air quality management technologies. The need to meet regulatory requirements and achieve energy performance targets creates a significant demand for HVAC equipment focused on energy efficiency upgrades, retrofits, and compliance assessment.

- For instance, by 2027, France targets an annual production of one million new heat pumps within its borders. To bolster demand, the government plans to streamline the regulatory and administrative procedures for installing heat pumps on roofs, aligning with its broader agenda of reducing bureaucratic hurdles. Continuing initiatives like MaPrimeRenov and energy-saving certificates will aid consumers in purchasing heat pumps.

- In September 2023, the French government announced plans to increase subsidies for heat pumps. This move is intended to ensure that the net cost of purchasing a heat pump aligns with that of a gas heater, particularly for low-income families. Additionally, the government is actively working toward bolstering the domestic heat pump industry, with a target capacity set at manufacturing up to 1 million units annually.

- For instance, the EHPA's subsidies for residential heat pumps in Europe report, based on data from early 2023, highlights that property owners are eligible for grants in France. When installed in existing properties, these grants can reach up to EUR 15,000 (USD 16326.67) for ground-source heat pumps and up to EUR 9,000 (USD 9796.00) for air-source heat pumps. The production of many heat pumps stimulates demand for HVAC equipment across multiple industry segments.

France HVAC Industry Overview

The Frech HVAC market is fragmented, with the presence of major players like Johnson Controls International PLC, Carrier Corporation, Robert Bosch GmbH, Daikin Industries Ltd, and System Air AB. Prominent players in the French HVAC market are adopting strategies, including partnerships, mergers, innovations, investments, and acquisitions, to enhance product offerings and gain sustainable competitive advantage.

- April 2024: Mitsubishi Electric is poised to bolster its European HVACR presence by acquiring Aircalo, a prominent air conditioning group based in France. This strategic move enhances Mitsubishi's portfolio, enabling it to cater to a broader spectrum of hydronic systems. These systems are designed to address the rising market demand for heating and cooling solutions that are both efficient and environmentally friendly, focusing on reducing greenhouse gas emissions.

- December 2023: Sonepar acquired Hydeclim, a French company that distributes air conditioning and treatment solutions. This acquisition follows Sonepar's recent acquisitions in France, including Alliantz, focusing on photovoltaics, and CD Sud, specializing in (heating, ventilation, and air conditioning). By acquiring Hydeclim, Sonepar bolstered its presence in the HVAC sector, broadening its air conditioning and heating installers offerings, explicitly focusing on Western and Northern France.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Supportive Government Regulations Including Incentives for Saving Energy through Tax Credit Programs

- 5.1.2 Innovations in HVAC Technology Including Smart Systems and Renewable Energy Integration

- 5.1.3 Increased Construction and Retrofit Activity to Aid Demand

- 5.2 Market Challenges

- 5.2.1 The High Upfront Cost of Energy-efficient and Advanced HVAC Systems

- 5.2.2 Skilled Labor Shortages

6 MARKET SEGMENTATION

- 6.1 By Type of Component

- 6.1.1 HVAC Equipment

- 6.1.1.1 Heating Equipment

- 6.1.1.2 Air Conditioning/Ventilation Equipment

- 6.1.2 HVAC Services

- 6.1.1 HVAC Equipment

- 6.2 By End-user Industry

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.3 Industrial

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Johnson Controls International PLC

- 7.1.2 Carrier Corporation

- 7.1.3 Robert Bosch GmbH

- 7.1.4 Daikin Industries Ltd

- 7.1.5 System Air AB

- 7.1.6 Flaktgroup Inc.

- 7.1.7 LG Electronics Inc.

- 7.1.8 BDR Thermea Group

- 7.1.9 Mitsubishi Electric Hydronics & IT Cooling Systems SpA

- 7.1.10 Danfoss Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET