PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1694045

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1694045

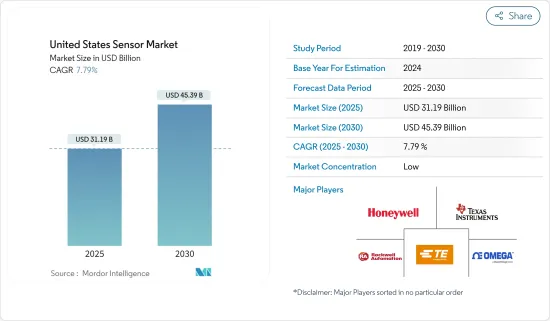

United States Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The United States Sensor Market size is estimated at USD 31.19 billion in 2025, and is expected to reach USD 45.39 billion by 2030, at a CAGR of 7.79% during the forecast period (2025-2030).

A sensor is designed to detect and react to various inputs from the physical environment, such as pressure, heat, light, motion, and moisture. The resulting output typically consists of a signal that can be displayed in a human-readable format at the sensor's location or transmitted electronically over a network for easy reading or additional processing.

The increasing demand for intelligent sensor technology is evident in various industries, from smartphone navigation systems to driver-assistance systems. Sensors are playing a vital role in staying competitive in the technology sector. Major trends like the Internet of Things (IoT), wearable health monitoring systems, and vehicle automation drive this demand. Consequently, intelligent sensors are now more accessible, enabling businesses in various industries to enhance automation, productivity, efficiency, and safety measures.

The evolution of sensing technology is apparent with advancements in process automation, leading to the development of more capable and interconnected sensing devices. As the shift toward digitalization speeds up, there is a growing demand for increased process automation, improved anomaly detection, and predictive maintenance capabilities, prompting a significant uptake of sensing technology.

Due to ongoing technological advancements, the automotive industry in the United States is experiencing a growing need for electronic sensors, especially for position-sensing applications. The industry's focus on technical progress, such as electrification and autonomous driving, has increased the demand for sensors. Additionally, the trend of incorporating position sensors into vehicles demonstrates a promising future for the market's growth.

Additionally, the increasing market for smart vehicles and the growing use of sensors by automotive original equipment manufacturers (OEMs) in the United States also drive the demand for sensors in the automotive sector. The rise in demand for sensors in the automotive industry is further bolstered by the enforcement of regulations requiring the use of specific sensors in vehicles.

While integrating sensors enhances industrial automation, it comes with an added cost that may be a limiting factor in cost-sensitive applications. Furthermore, the high costs associated with research and development for creating new products pose a significant challenge, especially for smaller sensor manufacturers that may lack funds.

United States Sensor Market Trends

Retractable Safety Syringes Segment Expected to Witness Significant Growth During the Forecast Period

- Chemical sensors are analyzers that respond selectively and reversibly to specific analytes, providing an electrical output signal that enables a comprehensive composition analysis. The country's escalating pollution levels have bolstered the demand for these sensors. Rising applications for chemical sensors in analyzing diverse sample compositions drive their adoption. Notably, the market is witnessing a surge in demand for low-cost, portable chemical sensors, including advanced orthogonal variants, underscoring a significant trend poised to propel the market's growth.

- Industrial development has spurred the production of various toxic materials, encompassing carcinogenic, mutagenic, and generally hazardous chemicals. Despite stringent management, these substances continue to endanger human health.

- Furthermore, the healthcare industry is increasingly interested in chemical sensors due to their capability to deliver continuous, real-time physiological and chemical data and non-invasive monitoring of biochemical markers in human biofluids such as tears, saliva, sweat, interstitial fluid, and human volatiles.

- Recent advancements have concentrated on electrochemical biosensors, particularly for monitoring metabolites, proteins, chemicals, and bacteria. Measuring biophysical quantities in the human body has been a significant focus in healthcare and medicine. Numerous flexible, wearable, and detachable sensors have been developed and commercialized to monitor critical parameters in sports, healthcare, and medical applications.

- Furthermore, as diabetes rates surge, the country's governments are ramping up investments in advanced diagnostic methods, fueling the uptake of chemical sensors in healthcare.

- The National Diabetes Statistics Report of 2024 revealed that 38.4 million adults in the United States had diabetes. Among them, 29.3 million had been diagnosed, while a concerning 9.7 million were undiagnosed. Notably, 29.2% of the American population, equating to 16.5 million seniors, were aged 65 and above. Furthermore, an estimated 1.2 million Americans are diagnosed with diabetes each year. The increasing number of diabetes patients in the country every year is expected to fuel the market's growth in the coming years.

North America Expected to Hold Significant Market Share During the Forecast Period

- The consumer electronics segment includes smartphones, laptops, tablets, televisions, gaming consoles, smart home devices, digital cameras, and others. Smart wearables are not considered in this segment.

- Most consumer electronics, such as mobile phones, laptops, game consoles, microwaves, and refrigerators, operate with temperature, proximity, motion sensors, etc. The high demand for these devices is a crucial factor contributing to the market's growth.

- Sensors in consumer electronics play a crucial role in improving the functionality, user-friendliness, and overall performance of a wide range of consumer electronic products, including smartphones, tablets, wearables, gaming consoles, home appliances, and others. These sensors enable these devices to interact with their surroundings and offer touch-sensitive interfaces, motion detection, image capture, environmental monitoring, and more capabilities.

- Sensing devices are used in more smart home applications as smart structures gain popularity. The demand for sensors is expected to increase due to the growing popularity of smart consumer electronics, IoT devices for smart homes, and technological advancements and innovations. Additionally, the growing use of wireless technologies, propelling the market for smart consumer electronics, is anticipated to open up new market opportunities for sensors.

- For instance, according to the Consumer Technology Association (CTA), in the United States, total revenue from the sales of smart home devices was estimated to reach USD 23.5 billion in 2023, compared to USD 19.7 billion in 2018. It is anticipated that the market for smart technology will witness rising demand for energy-saving appliances and increasing demand for sensors with applications.

- The adoption of smart home appliances will be fueled by sensor technology, AI, big data analytics, and IoT-enabled devices. Projections indicate that 2024 retail sales in the United States for consumer electronics will hit a significant USD 512 billion. In 2023, OLED TVs were on track to rake in USD 2.3 billion, while portable gaming consoles were eyeing a revenue of USD 1.5 billion.

United States Sensor Industry Overview

The United States Sensor market is fragmented, and the increasing presence of prominent manufacturers in the sensor industry is expected to intensify competitive rivalry during the forecast period. Market incumbents, such as Texas Instruments Incorporated, TE Connectivity Ltd, Omega Engineering Inc., Honeywell International Inc., Rockwell Automation Inc., etc., considerably influence the overall market.

February 2024 - STMicroelectronics introduced an all-in-one, direct Time-of-Flight (dToF) 3D LiDAR module boasting a market-leading 2.3k resolution. Additionally, the company has disclosed an early design win for the world's smallest 500k-pixel indirect Time-of-Flight (iToF) sensor. The VL53L9, a novel direct ToF 3D LiDAR device, offers a resolution of up to 2.3k zones. Featuring a dual scan flood illumination, which is unparalleled in the market, this LiDAR can detect small objects and edges while simultaneously capturing 2D infrared (IR) images and 3D depth map information.

January 2024 - ams OSRAM announced the showcase of the latest member of the Mira product family, the Mira016 CMOS image sensor, at Photonics West in San Francisco. The Mira016 boasts a resolution of 400 x 400 pixels for a backside illuminated (BSI) double-stack sensor that comes in a compact 1.8 mm x 1.8 mm package. It operates at a power of 20 mW at full resolution and 90 fps and also offers high quantum efficiency in the near-infrared, providing high performance with low power consumption.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain/Supply Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for IoT and Connected Devices

- 5.1.2 Increasing Adoption of Advanced Sensor Technologies in Automotive Industry

- 5.2 Market Restraints

- 5.2.1 High Initial Cost Involved

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Pressure

- 6.1.2 Level

- 6.1.3 Flow

- 6.1.4 Proximity

- 6.1.5 Environmental

- 6.1.6 Chemical

- 6.1.7 Inertial

- 6.1.8 Magnetic

- 6.1.8.1 Hall Effect Sensors

- 6.1.8.2 Other Magnetic Sensors

- 6.1.9 Position Sensors

- 6.1.10 Current Sensors

- 6.1.11 Other Types

- 6.2 By Mode of Operation

- 6.2.1 Optical

- 6.2.2 Electrical Resistance

- 6.2.3 Biosensor

- 6.2.4 Piezoresistive

- 6.2.5 Image

- 6.2.6 Capacitive

- 6.2.7 Piezoelectric

- 6.2.8 Lidar

- 6.2.9 Radar

- 6.2.10 Other Modes of Operation

- 6.3 By End-user Industry

- 6.3.1 Automotive

- 6.3.2 Consumer Electronics

- 6.3.3 Energy

- 6.3.4 Industrial and Other

- 6.3.5 Medical and Wellness

- 6.3.6 Construction, Agriculture and Mining

- 6.3.7 Aerospace

- 6.3.8 Robotics

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Texas Instruments Incorporated

- 7.1.2 TE Connectivity Ltd

- 7.1.3 Omega Engineering Inc.

- 7.1.4 Honeywell International Inc.

- 7.1.5 Rockwell Automation Inc.

- 7.1.6 Siemens AG

- 7.1.7 STMicroelectronics Inc.

- 7.1.8 AMS Osram AG

- 7.1.9 NXP Semiconductors NV

- 7.1.10 Infineon Technologies AG

- 7.1.11 Bosch Sensortec GmbH

- 7.1.12 Sick AG

- 7.1.13 ABB Limited

- 7.1.14 Omron Corporation

- 7.1.15 Allegro MicroSystems Inc

8 MARKET OUTLOOK