Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550213

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550213

UK Fixed Connectivity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

PUBLISHED:

PAGES: 120 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

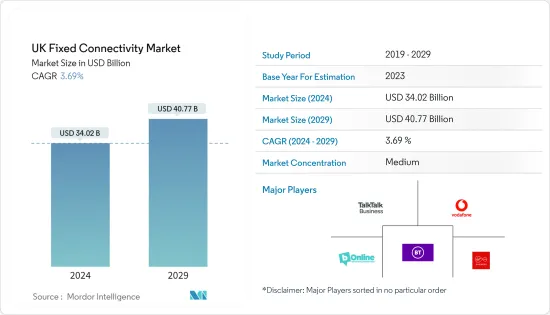

The UK Fixed Connectivity Market size is estimated at USD 34.02 billion in 2024, and is expected to reach USD 40.77 billion by 2029, growing at a CAGR of 3.69% during the forecast period (2024-2029).

Key Highlights

- The UK's fixed connectivity market is propelled by rising digital transformation, infrastructure investments, and government initiatives. The increasing need for reliable, high-speed internet, fueled by trends like remote work, online education, and digital services, underscores the demand for robust connections.

- Substantial investments in fiber optics and the deployment of gigabit-capable broadband are bolstering both the availability and quality of internet services. Government initiatives, such as "Project Gigabit," are specifically targeting the expansion of broadband access, with a focus on underserved regions. Moreover, as consumer demands for smooth streaming and adoption of smart home technologies surge, and businesses increasingly rely on steadfast connectivity, the market is witnessing a notable upswing.

- Ofcom's analysis of ISPs' rollout plans reveals a significant surge in the market's development. The number of properties with full-fiber coverage, also known as fiber to the premises (FTTP), is set to jump from 15.4 million in May 2023 to an estimated 27.0 million by May 2026, encompassing a remarkable 91% of all the properties. Physical Infrastructure Agreements (PIAs) serve as a pivotal enabler, granting ISPs access to Openreach's ducts and poles.

- This access surge is empowering more consumers, offering them a choice between ISPs operating on Openreach's infrastructure and those opting for alternative networks. These alternatives, like Hyperoptic, are increasingly constructing their fiber networks, diverging from reliance on Openreach or Virgin Media.

- Competition in the market is intense, driven by a mix of established and emerging players. These players are adopting a range of strategies to enhance their competitive edge and fuel market growth. For instance, in February 2024, Virgin Media O2 became the major UK provider to publicly introduce a residential 2 Gbps broadband service and present symmetrical download as well as upload speeds throughout all of its speed tiers as an alternative add-on for customers.

- However, the growing concerns about data security and privacy-related issues and Heavy CAPEX associated with advanced telecom infrastructure are some factors that can restrain the market growth over the forecast period.

UK Fixed Connectivity Market Trends

Digital Transformation is Increasing Across the Industries

- The UK's escalating digital transformation significantly boosts the fixed connectivity market's growth. As the nation embraces digital change, the need for high-speed, reliable internet surges. With cloud computing, remote work, online education, and digital services becoming staples for businesses and individuals, the importance of robust fixed connections is paramount.

- Stable and high-capacity networks are becoming increasingly vital due to the rise of advanced digital applications such as video conferencing, streaming, and smart technologies. This shift is fuelling investments in fiber optics and gigabit broadband, guaranteeing enhanced connectivity to meet the rising demand for advanced digital services. Consequently, it is hastening the nationwide enhancement and expansion of fixed connectivity infrastructure.

- In March 2024, Boldyn Networks (Boldyn), a global shared communications infrastructure provider, forged a strategic partnership with G.Network, London's full-fiber provider.

- The collaboration aims to accelerate London's journey toward becoming a global smart city. The partnership, driven by a unified vision of a more connected London, aims to bolster the 'Smarter London Together' initiative. It focuses on improving connectivity, optimizing city services, and promoting sustainable development throughout the capital. The partnership with Boldyn Networks signifies a pivotal juncture in London's digital transformation and a strategic move for G.Network.

- Rising social media utilization in the United Kingdom is propelling digital transformation by amplifying customer engagement, enabling real-time feedback, and fostering brand loyalty. Businesses are increasingly utilizing social media for precise marketing, harnessing data analytics to grasp consumer behaviors and preferences. This trend is increasing the adoption of sophisticated digital tools and platforms aimed at enhancing operational efficiency and elevating customer experiences.

- Social media's impact on e-commerce growth and influencer marketing is reshaping business models and digital strategies, hastening the nation's digital transformation. According to StatCounter, as of May 2024, the overall usage of Facebook in the United Kingdom was 58.75%, whereas in December 2023, it was around 56.44%. This rise in the overall usage of social media is thus anticipated to fuel the growth of digital transformation within the country, driving market growth opportunities significantly.

The Demand for Wireless Access Networks is Rising in the United Kingdom

- The expansion of wireless access networks in the United Kingdom is propelling market growth, fueled by the rising demand for high-speed, reliable backhaul infrastructure. This infrastructure is crucial in bolstering the wireless services' reach. With an increasing number of devices going wireless, the necessity for sturdy fixed connections becomes paramount. These connections facilitate the smooth data flow between wireless access points and the core networks. According to a survey by Ofcom, in 2023, 86% of the UK population used fixed broadband connectivity, and 91% used home internet access.

- The deployment of 5G technology in the United Kingdom necessitates a robust fiber optic infrastructure for its base stations. The UK's wireless access networks are experiencing robust growth, propelled by the surge in mobile device adoption, the rapid deployment of 5G technology, and the escalating need for remote work and online education solutions. According to GSMA Intelligence, in 2022, the United Kingdom predominantly utilized 4G technology for its mobile data connections. However, by 2030, 5G technology is projected to dominate, constituting a substantial 93% of all connections.

- The country is witnessing a strong demand for wireless connectivity, propelled by the expansion of the Internet of Things (IoT) and smart cities. Telecom providers, backed by government infrastructure investments and favorable policies, propel this growth. Consequently, both urban and rural areas in the UK are witnessing a significant improvement in the capacity, speed, and reliability of wireless networks.

- The UK government unveiled its Wireless Infrastructure Strategy with a goal to ensure 5G coverage across all populated regions by 2030. The strategy emphasizes investments in future connectivity technologies. The strategy outlines a comprehensive plan for 6G, positioning the UK as a forerunner in the upcoming wireless technology era. The government, backed by an initial funding of up to GBP 100 million (USD 130 million), also initiated a national mission to solidify the UK's position in "future telecoms" and 6G technologies.

- In January 2024, Access Hospitality, a division of The Access Group, announced its acquisition of Wireless Social, the UK's provider of guest Wi-Fi, analytics, and marketing solutions. The acquisition bolstered Access Hospitality's extensive technology portfolio, offering IT solutions that cover every facet of the hospitality industry. These solutions range from guest booking, EPoS, and table management to marketing, procurement, facilities management, training, and hotel PMS.

UK Fixed Connectivity Industry Overview

The UK fixed connectivity market is moderately competitive due to the presence of significant players like TalkTalk Business Direct Limited, Vodafone Limited, and BT Group. Players in the market are widely adopting strategies such as partnerships and product launches to enhance their overall product offerings and gain sustainable competitive advantage.

- March 2024: Virgin Media O2 and Liberty Global trialed a novel approach to enhance mobile services. They integrated their fixed network infrastructure with advanced 4G and 5G smart poles. This collaboration aims to improve mobile coverage in various UK locales.

- February 2024: Virgin Media O2, in collaboration with its major shareholders, Liberty Global and Telefonica, was spearheading the formation of a national fixed network company (NetCo). This initiative aims to bolster the adoption and deployment of full-fiber technology, introduce innovative financing avenues, and pave the way for potential mergers with alternative network providers. The objective is to position it as a significant competitor in the country's fixed network sector, providing a robust wholesale platform that offers a compelling alternative to BT's Openreach.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50002784

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 UK FIXED CONNECTIVITY MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Regulatory landscape in the UK for telecom-related services

- 4.3 Overview of macro-economic scenarios

- 4.4 Government initiatives related to fiber infrastructure developments

5 UK FIXED CONNECTIVITY MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Huge demand for high-speed connectivity

- 5.1.2 Rising digital transformation in the industries

- 5.2 Market Restraints

- 5.2.1 Data securities and privacy concerns

- 5.2.2 Heavy CAPEX associated with advanced telecom infrastructure

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Fixed Data

- 6.1.2 Fixed Voice

- 6.2 By End Users

- 6.2.1 Consumers

- 6.2.2 Enterprises

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 TalkTalk Business Direct Limited

- 7.1.2 Sky UK

- 7.1.3 Vodafone Limited

- 7.1.4 BT Group

- 7.1.5 bOnline Limited

- 7.1.6 Virgin Media Business Ltd

- 7.1.7 TVNET Limited

- 7.1.8 Eurocoms

- 7.1.9 Full Fibre Limited

- 7.1.10 ITS Technology Group Ltd

- 7.1.11 RUCKUS (CommScope)

- 7.1.12 Openreach Limited

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.