PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550201

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550201

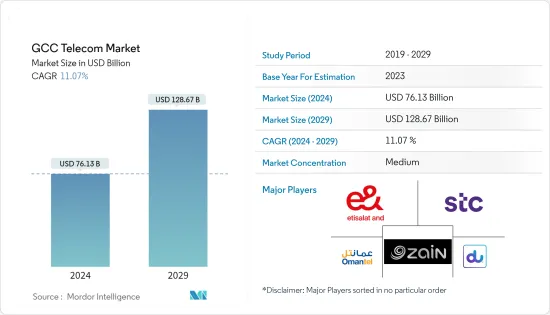

GCC Telecom - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The GCC Telecom Market size is estimated at USD 76.13 billion in 2024, and is expected to reach USD 128.67 billion by 2029, growing at a CAGR of 11.07% during the forecast period (2024-2029).

Key Highlights

- The telecom sector in the Gulf Cooperation Council (GCC) region is anticipated to expand primarily due to the growing urban population and the widespread use of cell phones that enable 3G, 4G, and 5G services. The Internet of Things (IoT), which connects with wired and wireless internet, is predicted to be used more in the telecom industry throughout the forecast period.

- According to the November 2023 Ericsson Mobility Report, mobile subscriptions in GCC are expected to increase from 76 million in 2023 to 81 million by 2029. By the end of 2023, 5G subscriptions were projected to constitute 34% of all mobile subscriptions, totaling 26 million subscriptions. Over the forecast period, 5G subscriptions are projected to grow annually at 19%, reaching 75 million by 2029 and accounting for approximately 90% of total subscriptions.

- The GCC telecommunications market has experienced substantial changes in recent years. These shifts are attributed to government efforts aimed at enhancing internet infrastructure and broadband connectivity, increased data consumption by both businesses and individuals, widespread adoption of 5G technology, and innovations introduced by major telecom vendors.

- In April 2024, Ericsson and Etihad Etisalat (Mobily) signed a memorandum of understanding (MoU) during LEAP 2024 in Riyadh, Saudi Arabia. The collaboration aims to enhance and evolve the network in Saudi Arabia using open radio access network (RAN) principles, with a focus on boosting network flexibility. As part of this initiative, they will explore different 5G deployment options within a flexible network architecture, including purpose-built RAN and Cloud RAN.

- For instance, a crucial platform for Saudi Arabia's Vision 2030 is the National Broadband Network of Saudi Arabia. The central government aims to finance significant resources and policies to create an all-encompassing fiber network. The region is witnessing many partnerships and developments in the fiber and broadband network area, strengthening the nation's overall telecom sector.

- Telecom operators face intensifying market competition. Thus, they are looking to optimize costs and pricing, giving rise to tower sharing amongst the operators. This has led to a significant shift in the focus area of telecom operators from network coverage, branding, and service design to tower sharing. Tower sharing provides potential reductions in operating and capital costs, which helps the telecom operator focus more effectively on marketing and customer satisfaction, thereby increasing the network reach.

- After the COVID-19 pandemic, the GCC telecom market experienced notable growth driven by increased demand for digital services and remote connectivity solutions. Countries like the United Arab Emirates and Saudi Arabia saw a surge in e-commerce and digital payments, boosting telecom revenues. Qatar and Bahrain also witnessed expansion, with investments in 5G infrastructure driving innovation and market competitiveness. Overall, the pandemic accelerated digital transformation, propelling the GCC telecom sector to new heights.

GCC Telecom Market Trends

Mobile Network is Expected to Drive the Market

- Saudi Arabia, the United Arab Emirates, and Oman, among other countries, benefit from a robust infrastructure. To continuously extend their smart cities, the main emphasis is expected to be on envisioning and innovating technology-driven development. In these countries, the population spends most of their time using social and communication apps. Businesses connect with their customers in countless ways, given how frequently and intensely they use their smartphones. Such factors are boosting smartphone adoption in the country.

- In the United Arab Emirates, three companies with unified licenses presently hold a significant market share: Mobile Telecommunication Company Saudi Arabia, Etihad Etisalat Company, and Saudi Telecom Company (STC).

- Other internet service providers (ISPs), mobile virtual network operators (MVNOs), and fixed-line service providers are also present in the market. The creation of a transparent, competitive market that keeps up with advanced infrastructure and technologies has been made possible in large part by the government.

- Moreover, companies like e& Etisalat and Saudi Telecom Company (STC) are key players, providing mobile services to meet the rising demand for data, voice, and messaging. These companies continuously innovate to offer competitive pricing, better coverage, and improved services to attract and retain customers in this expanding market. The emerging players and advancements in technology also contribute to the dynamic landscape of the GCC telecom industry.

- In February 2024, Power International Holding (PIH) reached an agreement to acquire Mobile Telecom Services (MTS) in Kazakhstan. MTS is currently owned by Kazakhtelecom, the National Telecommunications Company.

- In Oman, the mobile ecosystem is transforming at an ever greater scale as 5G technologies become available in the market. New capabilities will be introduced by 5G that enable operators to develop new use cases, applications, services, or revenue streams in consumer, business, and other sectors and markets.

Saudi Arabia is Expected to Witness Significant Growth

- As part of the 2030 Vision's National Transformation Program, the Saudi Ministry of Communications and Information Technology issued policies to encourage the rollout of FTTH ultra-fast broadband networks. The government has subsidized telecom companies to install fiber in underserved areas.

- The Saudi Data and Artificial Intelligence Authority wants to establish Saudi Arabia as a global provider of technology by developing a data and AI-driven economy. The country has made some investments in artificial intelligence, and the government is dedicated to transforming the nation digitally. The investments are primarily driven by local sources, particularly the nation's sovereign wealth fund.

- The major mobile service providers, Saudi Telecom Company (STC), Zain, and Mobily, also continued 5G expansion programs, thus driving the demand for effective, low latency, and high bandwidth mobile data and voice services in Saudi Arabia.

- In April 2024, Saudi Arabia's sovereign wealth fund, The Public Investment Fund (PIF), signed an agreement with mobile network operator Saudi Telecommunications Company (stc Group) for PIF to acquire a 51% stake in Telecommunication Towers Company (TAWAL) from stc Group.

- As per the Communications, Space & Technology Commission, there is a substantial increase in internet speed in Saudi Arabia, from 96.4 Mbps in 2021 to 153.1 Mbps in 2023, which has catalyzed significant growth in the telecom market. This boost enables faster data transmission, enhancing user experience and facilitating the adoption of bandwidth-intensive services like streaming and cloud computing. As a result, telecom providers are witnessing heightened demand for high-speed internet packages, driving competition and innovation in the market.

- Overall, this growth is led by the telecom, finance, government, and oil/gas sectors. Aggressive IT projects to modernize the Saudi Arabian government's IT infrastructure, including an e-government initiative and the telecom industry's liberalization, are increasing competition, service levels, and usage.

GCC Telecom Industry Overview

The GCC telecom market is becoming moderately consolidated. Some major players in the market include e& Etisalat, Saudi Telecom Company (STC), and Oman Telecommunications Company (Omantel), among others. The market also hosts several internet service providers (ISPs), MVNOs, and fixed-line service providers. These players focus on deploying 5G networks and increasing network capacity across the region to remain competitive in the market. For instance,

- In May 2024, Zain KSA invested SAR 1.6 billion (USD 0.43 billion) in expanding its infrastructure, 5G network, and digital services ecosystem. This move is part of an integrated expansion plan aligned with Zain KSA's strategy for achieving digital inclusion across the country. The goal is to enhance the digital infrastructure and provide an exceptional customer experience by expanding the 5G network to cover 122 cities and governorates, up from the current 66 cities.

- In March 2024, Ericsson and Du, from Emirates Integrated Telecommunication Company, entered into a strategic alliance to provide Ericsson with wireless network products, enabling intelligent services to the enterprise sectors and government in the United Arab Emirates. Ericsson and du have formed a strategic partnership to create advanced private 4G and 5G networks. Their collaboration aims to enhance connectivity for government and enterprise customers, enabling Industry 4.0 adoption in the country.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 An Assessment of the impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Huge demand for 5G

- 5.1.2 Significant penetrations of internet and smart phones

- 5.1.3 Rising digital transformation in the industries

- 5.2 Market Restraints

- 5.2.1 Security threats and leaks of private data

- 5.2.2 Heavy Capex associated with advanced telecom infrastructure

- 5.3 Ecosystem Analysis

- 5.3.1 Tower companies

- 5.3.2 OEMS (small cells, DAS etc.)

- 5.3.3 MNOs

- 5.3.4 MVNOs

- 5.3.5 OTT/PayTV

- 5.4 Evolution of GCC Telecom Sector

- 5.4.1 2G, 3G, 4G and 5G connections

- 5.5 Key metrics of GCC Telecom

- 5.5.1 Population

- 5.5.2 Fixed Broadband Subscriptions

- 5.5.3 Cellular Subscriptions

- 5.6 Analysis of Market Entry Strategy Of Vendors

6 MARKET SEGMENTATION

- 6.1 Overall telecom revenue

- 6.1.1 Telecom Subscriptions

- 6.1.2 Average revenue per user

- 6.2 Telecom services

- 6.2.1 Voice Services

- 6.2.1.1 Wired

- 6.2.1.2 Wireless

- 6.2.2 Data and Messaging Services

- 6.2.3 PayTV Services

- 6.2.1 Voice Services

- 6.3 Telecom connectivity

- 6.3.1 Fixed Network

- 6.3.2 Mobile Network

- 6.4 Country

- 6.4.1 Saudi Arabia

- 6.4.2 Kuwait

- 6.4.3 Qatar

- 6.4.4 Oman

- 6.4.5 United Arab Emirates

- 6.4.6 Bahrain

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis Of Key Vendors

- 7.2 Company Profiles

- 7.2.1 e& (Etisalat and)

- 7.2.2 Saudi Telecom Company (STC)

- 7.2.3 Ooredoo Group

- 7.2.4 Zain Group

- 7.2.5 Oman Telecommunications Company (Omantel)

- 7.2.6 Emirates Integrated Telecommunications Company (Du)

- 7.2.7 Mobily (Etihad Etisalat Company)

- 7.2.8 Batelco (Bahrain Telecommunication Company)

8 *The list is tentative and may change during the actual course of study

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS