PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550157

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550157

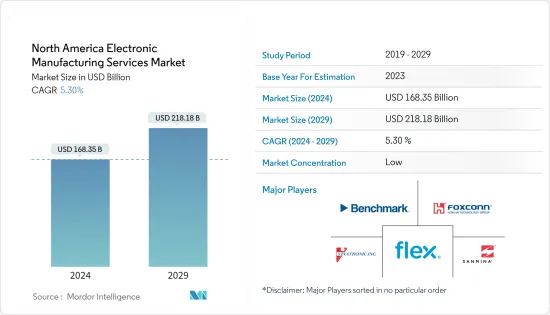

North America Electronic Manufacturing Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The North America Electronic Manufacturing Services Market size is estimated at USD 168.35 billion in 2024, and is expected to reach USD 218.18 billion by 2029, growing at a CAGR of 5.30% during the forecast period (2024-2029).

Companies engaged in electronic manufacturing provide a wide range of value-added services such as product designing, engineering, and manufacturing for original equipment manufacturers (OEMs), allowing them to focus primarily on R&D and other core activities like marketing and sales. Electronic manufacturing services (EMS) are also interchangeably used with a more generic term, "contract manufacturing."

With the growing proliferation of emerging technologies such as the Industrial Internet of Things (IIoT), increasing miniaturization of electronic components, and enhanced communication posed by 5G, the need for revolutionizing electronic component design and assembly has been felt for years. Also, the demand for EMS in North America has been increasing owing to the higher labor cost, forcing OEMs operating in the electronics industry to outsource manufacturing activities.

In North America, the Industrial Internet of Things (IIoT) and Industrial 4.0 are central to the new technological approaches for developing, producing, and managing the entire logistics chain, otherwise known as smart factory automation. They dominate the industrial sector trends, with machinery and devices being connected via the Internet.

As a result of such trends, the demand for advanced electronic devices/components has been growing significantly. This creates a favorable ecosystem in the market as it becomes difficult for OEMs to cover all aspects of the electric device production process, ranging from design to engineering to production. Hence, some outsource the manufacturing to EMS providers offering specialized manufacturing services.

The growing demand for electronic devices in the consumer segment is another major factor supporting the market's growth in the region. Significant demand growth makes it hard for OEMs to scale their operations quickly, considering the higher complexity of developing electronic device/component manufacturing facilities. Hence, some OEMs outsource the production activities to EMS companies.

However, factors such as higher investment required in developing electronics manufacturing facilities are among the significant challenges for the market's growth. Also, the presence of stringent industry regulations and guidelines challenges the market's growth in the region as companies must follow various local, state, federal, and foreign environmental laws and regulations for manufacturing processes, as well as the storage, treatment, discharge, emission, and disposal of hazardous waste by-products of these processes.

Also, the electronics assembly process can generate lead dust, and companies are responsible for remediating lead dust from the interior of the manufacturing facility while vacating the space. Companies must also monitor for airborne lead concentrations in the buildings and are unaware of any significant lead concentrations over the applicable OSHA or other local standards.

North America Electronic Manufacturing Services Market Trends

Consumer Electronics to Hold a Significant Market Share

- North America is among the major consumer electronic goods markets. The proliferation of devices such as personal computers, smartphones, and other electronic home appliances is significantly higher in countries such as the United States and Canada than in developing countries, which creates a favorable ecosystem for the growth of electronic manufacturing services in the country. OEMs take support from third-party contract manufacturers to ensure the availability of products as per market demand.

- According to the Consumer Technology Association, revenue from consumer electronics and technology sales in the United States is estimated to reach USD 512 billion in 2024, compared to USD 413 billion in 2018. The growing acceptance of digital technologies further supports this trend, driving the region's demand for consumer electronic products.

- Another major factor supporting the growth of the consumer electronics industry in the region is the growing availability of supporting infrastructure. For instance, the United States and Canada have witnessed a notable increase in the expansion of 5G and other connectivity networks such as IoT and LoRa, creating a favorable ecosystem for the market's growth.

- Considering a higher demand and future growth prospects, the number of vendors offering electronic manufacturing services in the region is also increasing. For instance, August Electronics and Avalon Technologies Ltd are some vendors providing electronic manufacturing services in Canada. Similarly, several vendors operating in the same domain are present in the United States, which supports the market's growth in the region.

The United States To Witness Significant Growth

- The United States is expected to continue to be one of the leading markets for electronic manufacturing services in the North American region. The primary factor behind this is the presence of many OEMs engaged in the research and design of electronic devices and components.

- Also, a higher demand for electronic products in the country is another major factor influencing the demand for electronic manufacturing services. For instance, the United States is one of the major markets for industrial automation solutions. According to the International Federation of Robotics, the United States is among the primary adopters of industrial robots; each year, a significant number of industrial robots are installed in the country, which drives the demand for electronic devices/components.

- The United States is also among the major automotive markets. Millions of automobiles are produced annually in the country to fulfill local demand and export. The automotive manufacturing facilities of various car manufacturers in the country are highly automated to maintain accuracy and efficiency. This supports the demand for electronic products, creating a favorable ecosystem for the market's growth in the country.

- The adoption of advanced electronic devices is also increasing in the consumer segment. According to the Consumer Technology Association estimates, sales revenue from smart home devices in the United States was expected to reach USD 23.5 billion in 2023, up from USD 19.7 billion in 2018. Such trends will also promote the electronic manufacturing services industry in the country.

- Moreover, in the aftermath of the pandemic, the United States government has taken several initiatives to support the growth of the electronics and chip manufacturing industry, which was highly dependent on outsourcing. The launch of initiatives such as the Chips and Science Law and Bipartisan Infrastructure Law has several provisions to restore semiconductor chip production. Hence, such trends are also anticipated to support the country's market growth during the forecast period.

North America Electronic Manufacturing Services Industry Overview

The North American electronic manufacturing services market is highly competitive and has several players. Companies continuously try to increase their market presence by introducing new products, expanding their operations, or entering into strategic mergers and acquisitions, partnerships, and collaborations. Some of the major players include Vinatronic Inc., Benchmark Electronics Inc., Flex Ltd, and Sanmina Corporation.

April 2024 - International Business Machines Corp. (IBM) unveiled its intentions to bolster its Canadian semiconductor packaging and testing facility with over CAD 1 billion (~USD 730 million) investments over the next five years. In the initial phase, IBM, in collaboration with its partner, the MiQro Innovation Collaborative Centre, is injecting CAD 227 million (~USD 165 million) into the project. This investment will expand the current Quebec plant and establish a dedicated research and development lab.

January 2024 - Creation Technologies, an end-to-end electronic manufacturing service provider, opened a new state-of-the-art manufacturing facility in New York, United States. The company, with 13 locations in the United States and China, has opened a new facility to strengthen its presence in the United States further and meet the evolving requirements of its customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 and Other Macroeconomic Factors on the Electronic Manufacturing Services Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Trends of Miniaturization

- 5.1.2 Adoption of Emerging Technologies in IIoT (Industrial Internet of Things), Blockchain, and Enhanced Communication

- 5.2 Market Challenges

- 5.2.1 Intensifying Competition and Rigorous Government and Environmental Regulations

- 5.2.2 Intellectual Property Rights Infringements

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Electronics Design and Engineering

- 6.1.2 Electronics Assembly

- 6.1.3 Electronics Manufacturing

- 6.1.4 Other Service Types

- 6.2 By Application

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive

- 6.2.3 Industrial

- 6.2.4 Aerospace and Defense

- 6.2.5 Healthcare

- 6.2.6 IT and Telecom

- 6.2.7 Other Applications

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

7 COMPETITIVE LANDSCAPE*

- 7.1 Company Profiles

- 7.1.1 Vinatronic Inc.

- 7.1.2 Benchmark Electronics Inc.

- 7.1.3 Hon Hai Precision Industry Co. Ltd (Foxconn)

- 7.1.4 Flex Ltd

- 7.1.5 Sanmina Corporation

- 7.1.6 Jabil Inc.

- 7.1.7 SIIX Corporation

- 7.1.8 Nortech Systems Incorporated

- 7.1.9 Celestica Inc.

- 7.1.10 Integrated Micro-electronics Inc.

- 7.1.11 Creation Technologies LP

- 7.1.12 Wistron Corporation

- 7.1.13 Plexus Corporation

- 7.1.14 TRICOR Systems Inc.

- 7.1.15 Sumitronics Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET