PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550148

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550148

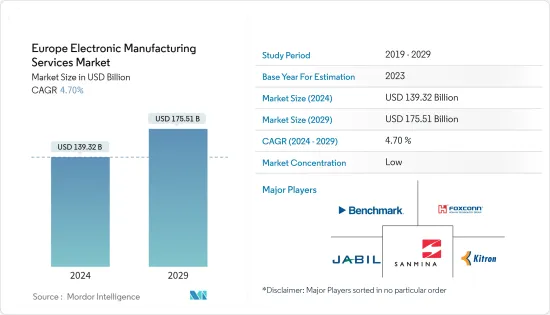

Europe Electronic Manufacturing Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Europe Electronic Manufacturing Services Market size is estimated at USD 139.32 billion in 2024, and is expected to reach USD 175.51 billion by 2029, growing at a CAGR of 4.70% during the forecast period (2024-2029).

Europe's numerous innovation hubs maintain its reputation for innovation and robust R&D capabilities. With consumer electronics advancing swiftly, European EMS providers leverage their proximity to these innovation centers, ensuring access to the latest technologies.

The surge in digitalization across industries, fueled by the adoption of technologies like the Internet of Things (IoT) and artificial intelligence (AI), strengthens the need for electronic components and manufacturing services. According to the European Commission, IoT spending in Europe has grown significantly. By pivoting toward digitalization and providing comprehensive solutions, regional EMS providers stand to capitalize on such trends.

In addition, the rising consumer preference for personalized electronics is fueling the demand for EMS providers adept at agile manufacturing. EMS firms are embracing cutting-edge technologies like 3D printing, flexible electronics, and modular designs to meet this demand. These innovations empower EMS providers to deliver bespoke solutions, catering to various customer needs and setting themselves apart in a competitive landscape.

Further, rising government initiatives in several regional countries drive the market's growth. For instance, in April 2023, the European Commission introduced stringent regulations to curb energy consumption in electrical appliances. These rules extend to devices with external power supplies, notably targeting small network equipment (like Wi-Fi routers and modems) and wireless speakers, especially when in 'standby' mode. The commission projects a substantial energy-saving potential by mandating lower power consumption during idle states, estimating a cumulative 4 TWh reduction by 2030. These standards are designed to boost energy efficiency and curb greenhouse gas emissions.

Similarly, the United Kingdom made significant strides in embracing Industry 4.0, with widespread participation from businesses, consumers, and the workforce. The Department of Industrial Strategy projects that by accelerating innovations and embracing Industry 4.0 solutions, the UK's manufacturing sector could see significant growth in the coming decade, creating demand for industrial electronic devices and driving opportunities in the market.

However, surging demand for technologies such as IoT, 5G, and EVs is fueling an unprecedented need for electronic components, often surpassing available supply. Shortages of crucial raw materials and components like chips and capacitors are causing production delays. Compounding the issue, backlogs at component suppliers have stretched lead times from weeks to months. These disruptions hamper EMS manufacturers' assembly processes and complicate timely product deliveries.

The electronics manufacturing industry is rapidly evolving, posing challenges for producers to keep pace. Key hurdles include upskilling the workforce and modernizing production facilities, frequently leading to increased production costs and delays.

Europe Electronic Manufacturing Services Market Trends

Electronics Design and Engineering Service Type is Expected to Hold Significant Market Share

- Electronic design tools, including computer-aided engineering, IC physical design, and verification, have ushered in a smarter design era. By reducing design time and errors, these tools have garnered significant popularity. The adoption of electronic design automation (EDA) tools has steadily risen, especially in sectors like automotive and aerospace. However, a notable drawback of EDA tools is their limited ability to draw insights from past designs.

- Given the rising demand for large volumes of complex chips, particularly for consumer electronics, electronics design firms increasingly turn to machine learning in their EDA toolsets. Machine learning offers profound insights into the semiconductor industry through modeling and simulation and promises heightened accuracy and efficiency, nudging engineers toward greater automation. As electronic device manufacturers witness the benefits of EDA tools enhanced by machine learning, they swiftly embrace these advanced solutions. This shift fosters innovation in designs and chips and fuels the widespread adoption of EDA tools.

- Further, AI-driven design automation tools autonomously create circuit designs, PCB layouts, and system architectures, adhering to set requirements and constraints. They outpace manual methods, swiftly navigating a broader design spectrum, leading to the discovery of novel topologies and architectures. Cutting-edge techniques, including generative adversarial networks (GANs) and reinforcement learning, are harnessed to birth fresh design concepts. In addition, Europe is widely adopting AI technologies for several industries, which can be a boon for market growth. According to Eurostat, in 2023, Denmark, in Europe, had 15.2% of AI adoption, the highest across the region.

- Initiatives taken by European governments to strengthen semiconductor manufacturing are also favoring the market's growth in the region. For instance, in 2023, the European Union (EU) approved a EUR 43 billion (~USD 47.5 billion) plan called the Chips Act to develop semiconductor fabs and support Europe's overall semiconductor production ecosystem.

Germany is Expected To Hold Significant Market Share

- The manufacturing sector is integral to Germany's economic growth, owing to critical industries like automotive, chemicals, engineering, consumer durables, and pharmaceuticals. In Q4 2023, Germany's manufacturing sector reported a GDP of EUR 193,736 billion, reflecting a significant increase from EUR 183,697 billion in Q4 2022, according to the Federal Statistical Office. This reflects that the country is steadily moving toward automation and process-driven manufacturing, which are projected to improve efficiency and enhance productivity.

- The country has one of the prominent sectors with many automation manufacturing facilities: the automobile industry. To maintain accuracy and efficiency, it was observed that the manufacturing facilities of various car manufacturers were automated. In addition, the demand in the automobile industry is expected to grow due to an increasing trend toward replacing traditional vehicles with EVs. For instance, according to KBA, Germany has witnessed a substantial surge in registering new electric cars. In 2023, the country registered a notable 524,219 new electric vehicles. As modern EVs contain more electronic units, such trends create a favorable ecosystem for the market's growth in the region.

- The shift in the automotive industry's electrification trend extends beyond the engines, permeating the vehicles with features like automated electric windows, power steering, and ADAS. These advancements have propelled the automotive industry to the forefront, making it a key driver of demand in the electronics manufacturing services market.

- Germany also boasts a substantial reservoir of skilled engineers, technicians, and manufacturing personnel, providing EMS providers with a rich talent pool. Ongoing training and upskilling initiatives help employees stay abreast of evolving technologies and cultivate an innovative ethos. This technical prowess is instrumental in offering cutting-edge design, prototyping, and manufacturing services.

Europe Electronic Manufacturing Services Industry Overview

The European electronic manufacturing services market is competitive and has several regional and global players. Significant players continuously try to increase their market presence by introducing new products, expanding their operations, or entering into strategic mergers and acquisitions, partnerships, and collaborations.

- In May 2024, Foresight Group, a prominent regional private equity and infrastructure investment manager, disclosed a GBP 4.5 million (~USD 5.70 million) investment in Assembly Contracts Limited. ACL, a key player in manufacturing printed circuit board assemblies (PCBAs) for electronic devices, is set to expand its operations and generate additional skilled employment opportunities courtesy of Foresight's backing.

- In May 2024, the President of TSMC Europe confirmed the company's plans to build its inaugural chip plant in Dresden, eastern Germany. Construction is set to kick off in the fourth quarter of 2024, with production slated to commence in 2027.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 An Assessment of Macroeconomic Factors on The Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Digitalization and Industry 4.0 Integration

- 5.1.2 Increasing Inclination Towards Sustainability and Green Manufacturing Owing to Several Regional Government Regulations

- 5.2 Market Restraints

- 5.2.1 Rising Cost of Raw Materials

- 5.2.2 Increasing Regional Regulatory and Compliance Issues

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Electronics Design and Engineering

- 6.1.2 Electronics Assembly

- 6.1.3 Electronics Manufacturing

- 6.1.4 Other Service Types

- 6.2 By Application

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive

- 6.2.3 Industrial

- 6.2.4 Aerospace and Defense

- 6.2.5 Healthcare

- 6.2.6 IT and Telecom

- 6.2.7 Other Applications

- 6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Spain

- 6.3.6 Netherlands

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Benchmark Electronics Inc.

- 7.1.2 Hon Hai Precision Industry Co. Ltd (Foxconn)

- 7.1.3 Kitron ASA

- 7.1.4 Sanmina Corporation

- 7.1.5 Jabil Inc.

- 7.1.6 SIIX Corporation

- 7.1.7 Celestica Inc.

- 7.1.8 Integrated Micro-electronics Inc.

- 7.1.9 Wistron Corporation

- 7.1.10 Plexus Corporation

- 7.1.11 BMK Group

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET