Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550011

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550011

Semiconductor Consumables - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

PUBLISHED:

PAGES: 120 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

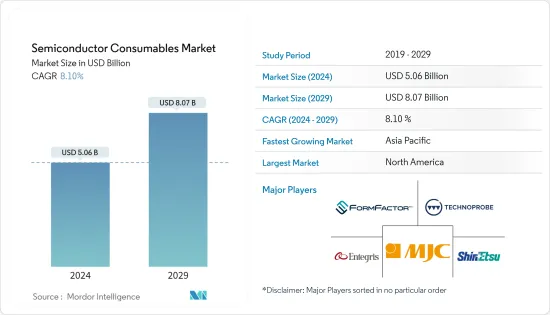

The Semiconductor Consumables Market size is estimated at USD 5.06 billion in 2024, and is expected to reach USD 8.07 billion by 2029, growing at a CAGR of 8.10% during the forecast period (2024-2029).

Key Highlights

- Semiconductor consumables are materials or components used in semiconductors' manufacturing and testing processes. These consumables are essential for producing semiconductors and are often disposable or replaceable parts used in fabrication. They play a crucial role in ensuring the quality and efficiency of semiconductor production. Semiconductors are widely used in various industries, including computers, mobile phones, automotive technologies, and consumer electronics. The semiconductor industry is an essential part of the global economy and serves as an indicator of the economy's overall health. As the demand for semiconductors increases, the need for reliable and high-quality consumables becomes increasingly essential.

- Semiconductor consumables can include various materials and components employed in the manufacturing process. Some examples of semiconductor consumables are electrodes, focus rings, blades, gaskets, and other parts that need frequent replacement. These consumables are used with machinery and equipment to ensure efficient production of semiconductors.

- Technological advancements serve as a key driver for the semiconductor consumables industry. As the demand for faster, compact, and more efficient electronic devices increases, semiconductor manufacturers require advanced consumables to meet these evolving requirements. The development of new materials, novel fabrication techniques, and the integration of artificial intelligence and machine learning in semiconductor manufacturing processes are likely to offer lucrative opportunities for the growth of the market studied.

- Wet chemicals, including acids, hydroxides, and peroxides, are used for cleaning and etching substrate surfaces in the semiconductor industry. These processes are essential for the fabrication and wet stripping of semiconductors. The manufacturing process of semiconductors requires a clean environment, and wet chemicals play a crucial role in maintaining this cleanliness. Chemicals like hydrogen peroxide are used for long-term applications such as etching and cleaning integrated circuits (ICs).

- The establishment of new semiconductor manufacturing facilities also drives the demand for semiconductor consumables. As these facilities increase their production capacity, the demand for the studied market is expected to increase rapidly. For instance, in March 2024, the Union Cabinet of India approved INR 1.26 trillion (USD 15.07 billion) worth of investments in three semiconductor plants, including a Tata Group proposal to build the country's first major chip fabrication facility at Dholera in Gujarat. The semiconductor fabrication unit in Dholera by Tata Electronics, in partnership with Powerchip Semiconductor Manufacturing Corp (PSMC), Taiwan, would manufacture high-performance computing chips with 28 nm technology.

- The semiconductor consumables industry faces several market restraints that impact its growth and profitability. One major restraint is the high cost of raw materials used in the manufacturing of semiconductor consumables. This increases the overall production cost, making it difficult for companies to maintain competitive pricing. Additionally, the industry is highly dependent on the semiconductor market, which is subject to cyclical demand patterns and economic fluctuations. This volatility can lead to unpredictable demand for consumables, affecting revenue streams.

- Further, the conflict between Russia and Ukraine will significantly impact the semiconductor industry. The conflict has already exacerbated the semiconductor supply chain issues and the chip shortage that have affected the industry for some time. The disruption may result in volatile pricing for critical raw materials such as nickel, palladium, copper, titanium, and aluminum, resulting in material shortages. This, in turn, could impact the manufacturing of semiconductors.

Semiconductor Consumables Market Trends

The Wet Chemicals Segment is Expected to Drive the Market's Growth

- Semiconductor technology relies heavily on the precise manipulation and fabrication of semiconductor materials. One critical aspect of semiconductor manufacturing is the use of wet chemicals in various consumables. These chemicals are important in cleaning, etching, and passivating semiconductor surfaces, ensuring high-quality, defect-free devices.

- Wet chemicals are extensively used in the cleaning processes of semiconductor manufacturing. Semiconductor wafers, the primary substrates for chip production, often have impurities, contaminants, and residue from previous processing steps. Wet chemical cleaning removes these impurities and ensures a pristine starting point for subsequent fabrication steps. Different chemicals, such as sulfuric acid, hydrogen peroxide, and deionized water, are used to remove specific types of contaminants.

- Etching is an essential step in semiconductor manufacturing, used to remove layers of material from the wafer surface selectively. Wet etching involves using chemicals that can selectively dissolve specific materials without affecting others. For instance, hydrofluoric acid is commonly used to etch silicon dioxide, while other chemicals like potassium hydroxide or nitric acid are used for different materials. Precise control of the etching process is essential to achieve desired device structures and dimensions.

- Proper chemical waste management becomes critical with the increasing use of wet chemicals in semiconductor manufacturing. The disposal of spent chemicals requires adherence to strict environmental regulations to minimize ecological impact. Recycling and treatment processes are employed to recover valuable components from the waste, reducing environmental harm and overall production costs.

- The demand for semiconductors has been on the rise, driven by various factors such as robust growth in consumer electronics, computing, 5G, and automotive semiconductors. This increased demand for semiconductors directly translates into a higher demand for wet chemicals used in their manufacturing processes.

- According to Ericsson Mobility Report 2023, between the end of 2023 and 2029, global 5G subscriptions are forecasted to increase by over 330%, from 1.6 billion to 5.3 billion. 5G coverage was forecasted to be available to more than 45% of the global population by the end of 2023 and 85% by the end of 2029. North America and the Gulf Cooperation Council are anticipated to have the highest regional 5G penetration rates by the end of 2029 at 92%. Western Europe is forecasted to follow at 85% penetration.

- Moreover, according to Ericsson, the global number of smartphone mobile network subscriptions reached nearly 6.6 billion in 2022, and it is expected to exceed 7.8 billion by 2028. This is expected to drive the market studied further.

Asia-Pacific is Expected to Witness a High Market Growth Rate

- Taiwan plays a crucial role in semiconductor manufacturing in Asia-Pacific. Taiwan's semiconductor industry owes much of its success to the proactive role played by the government. The Taiwanese government has implemented a diverse range of policies and initiatives to foster the growth of the industry.

- One such initiative is the Industrial Upgrading and Transformation Plan, which aims to enhance the competitiveness of Taiwan's semiconductor industry through investments in research and development, talent acquisition, and infrastructure development. The government has also provided tax incentives, subsidies, and funding support to domestic semiconductor companies, encouraging them to invest in innovation and expand their global reach.

- Taiwanese semiconductor companies have continuously innovated advanced products and processes in the semiconductor consumables market, driving technological advancements in the industry. Advanced chip manufacturing technologies, such as 7 nm and 5 nm processes, have been successfully developed and deployed by Taiwanese firms, facilitating the production of smaller, faster, and more energy-efficient chips. The ability to manufacture these advanced semiconductors has given Taiwan a competitive edge in the global market.

- Additionally, the industry has witnessed substantial progress in the development of specialized chips for emerging technologies like artificial intelligence, the Internet of Things (IoT), and autonomous vehicles, which are further driving the growth of Taiwanese semiconductor consumables vendors.

- Taiwanese companies, such as TSMC (Taiwan Semiconductor Manufacturing Company), MediaTek, and UMC (United Microelectronics Corporation), have become critical players in the global semiconductor supply chain. TSMC, in particular, has emerged as one of the world's largest contract chipmakers, catering to prominent global technology companies.

- The presence of major semiconductor companies is likely to aid the expansion of the market studied in the country. Moreover, Taiwan's semiconductor industry has leveraged its robust supply chain to gain a competitive advantage. The country has developed a vertically integrated ecosystem, encompassing everything from design and manufacturing to testing and packaging. This integration allows for greater flexibility and cost-effectiveness, making Taiwan an attractive destination for semiconductor companies worldwide.

- The increasing electronics production and demand in Asia-Pacific are likely to drive the growth of the market studied. For instance, China is one of the prominent consumer electronics producers worldwide. The manufacturing industry is growing quickly in the country and is witnessing the deployment of several manufacturing and telecommunications technologies, which is likely to aid in the market's growth.

Semiconductor Consumables Industry Overview

The semiconductor consumables market is a competitive market with the presence of several major players like FormFactor Inc., Technoprobe SpA, Micronics Japan Co. Ltd, Entegris Inc., and Shin-Etsu Polymer Co. Ltd. The market players are striving to innovate new products by way of extensive investments in R&D, collaborations, and mergers to cater to the evolving demands of consumers.

- November 2023: Teradyne Inc., a prominent supplier of automated test solutions, and Technoprobe SpA, a significant company in the design and production of probe cards, announced a series of agreements establishing a strategic partnership that is anticipated to accelerate growth for both companies and allow them to deliver higher performance semiconductor test interfaces to their global customers. As part of the partnership, Teradyne will make nearly USD 516 million in equity investment in Technoprobe, and Technoprobe will acquire Teradyne's Device Interface Solutions business for USD 85 million. The companies also claimed to engage in joint development projects.

- August 2023: Technoprobe finalized its acquisition of Harbor Electronics Inc. Harbor Electronics, a company founded in the '80s in Santa Clara, California, is a prominent manufacturer of advanced printed circuit boards for testing systems for prominent semiconductor manufacturers. As per Technoprobe, the acquisition is claimed to allow it further to strengthen its technological skills in the testing field and vertically integrate the probe card production process, bringing PCB production expertise in-house.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50002654

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Advancements

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.3.6 Threat of New Entrants

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

- 4.5 Industry Supply Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand for Certain Class of ICs

- 5.2 Market Restraints

- 5.2.1 Uncertainties in Demand for Certain Segments and Supply Chain Uncertainties

6 MARKET SEGMENTATION

- 6.1 By Product Category

- 6.1.1 Wet Chemicals (includes acids, basis, associated mixtures, and organics)

- 6.1.2 Wafer Shipping Containers

- 6.1.3 Wafer Processing (Cassettes, FOUP, FOSB Boxes etc.)

- 6.1.4 Test Consumables

- 6.1.4.1 Probe Card (Vertical, MEMS, Cantilever, and Other Speciality)

- 6.1.4.2 Sockets (Burn-in, and Test)

- 6.1.5 End Effectors

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Taiwan

- 6.2.3 China

- 6.2.4 South Korea

- 6.2.5 Japan

- 6.2.6 Europe

- 6.2.7 South East Asia

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 FormFactor, Inc.

- 7.1.2 Technoprobe S.p.A.

- 7.1.3 Micronics Japan Co., Ltd.

- 7.1.4 Japan Electronic Materials (JEM)

- 7.1.5 MPI Corporation

- 7.1.6 Entegris, Inc.

- 7.1.7 Shin-Etsu Polymer Co., Ltd.

- 7.1.8 Miraial Co Ltd

- 7.1.9 3s Korea Co.,Ltd.

- 7.1.10 Dainichi Shoji K.K.

8 VENDOR RANKING ANALYSIS

9 FUTURE OF THE MARKET

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.