PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550006

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550006

Data Center Processor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

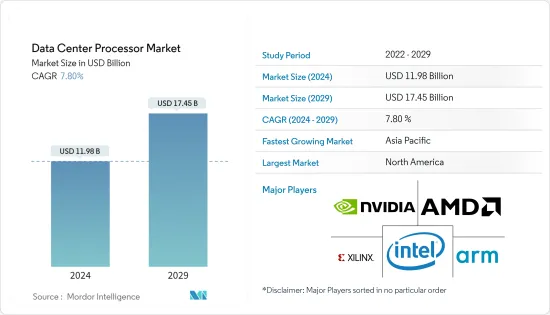

The Data Center Processor Market size is estimated at USD 11.98 billion in 2024, and is expected to reach USD 17.45 billion by 2029, growing at a CAGR of 7.80% during the forecast period (2024-2029).

Key Highlights

- A data center processor is a critical component of a data center's computing infrastructure. It is a high-performance chip that performs various tasks, including arithmetic, logic, and input/output operations. Data centers rely on servers, which are high-performance computers with large storage space, memory, processing power, and input/output capabilities. These servers use data center processors to handle the computational workload and run applications. The choice of processors in a data center depends on the specific tasks and requirements. General-purpose CPUs may be suitable for many applications, but processors optimized for these workloads may be preferred for specialized tasks like artificial intelligence (AI) and machine learning (ML).

- CPU processors are the most common type of processors found in data centers. They provide the capability to handle various tasks and applications, making them versatile and adaptable. Initially designed for graphics-intensive applications, GPU processors have become indispensable in data centers due to their parallel processing capabilities. GPUs perform highly parallel computations, making them suitable for machine learning, artificial intelligence, and big data analytics. Their massive number of cores enables them to process vast amounts of data simultaneously, significantly reducing processing time and improving overall performance.

- FPGA processors offer the advantage of programmable hardware, allowing customization to specific applications. They provide the flexibility to reconfigure their circuitry, making them suitable for tasks that require low latency and high throughput. FPGA processors are often used for functions such as encryption, video processing, and network packet processing, where real-time processing is crucial.

- With the proliferation of connected devices, cloud computing, and the Internet of Things, the amount of data being generated is increasing at an unprecedented rate. This surge in data necessitates powerful processors that can handle data centers' processing and analysis requirements. Further, data centers are responsible for processing and analyzing vast real-time data. As industries increasingly rely on data-driven insights and complex computations, processors must deliver high performance and efficiently handle demanding workloads.

- Moreover, energy efficiency is a significant market driver for data center processors. Data centers consume enormous amounts of energy, and optimizing power consumption is crucial for reducing operational costs and environmental impact. Processors that offer higher performance per watt are in high demand as they allow for more efficient data center operations. Moreover, the increasing adoption of artificial intelligence (AI) and machine learning (ML) technologies is driving the demand for processors with enhanced capabilities in handling AI workloads. AI and ML algorithms require powerful processors to process and analyze complex data patterns and make accurate predictions, driving the need for specialized processors optimized for AI workloads.

- One of the key macroeconomic trends that can affect the data center processors market is GDP growth. As the economy expands, companies are inclined to increase their investments in IT infrastructure, such as data centers. This increased investment leads to a higher demand for data center processors, as businesses require more computing power to handle the growing volume of data. For instance, the United States is a prominent data center market. According to the Bureau of Economic Analysis (BEA), the US GDP increased from USD 25.7 trillion in 2022 to about USD 27.36 trillion in 2023.

- However, the data center processor market faces several market restraints that can hinder its growth and potential. The high cost of data center processors is a significant barrier for small and medium-sized businesses, limiting their adoption. Additionally, the rapid technological advancements in the industry lead to a shorter lifecycle of processors, making it challenging for businesses to keep up with the latest innovations.

Data Center Processor Market Trends

The Central Processing Unit (CPU) Segment is Expected to Drive the Growth of the Market

- CPU data center processors, also known as server processors, are a crucial component in the functioning of data centers. These processors are specifically devised to handle the demanding workload and high-performance requirements of data center environments. One of the primary features of CPU data center processors is their high core count. These processors often have multiple cores, ranging from 8 to 64 or more. This allows for parallel processing of tasks, enabling data centers to handle various workloads simultaneously. The high core count also ensures efficient resource utilization, maximizing the data center's overall performance.

- Another essential feature is the high clock speed of CPU data center processors. Clock speed refers to how fast a processor can execute instructions. Higher clock speeds result in faster data processing, which is crucial for data centers that need to handle large amounts of data in real time. Additionally, CPU data center processors often have turbo boost technology, temporarily increasing the clock speed when additional performance is required.

- Also, CPU data center processors are designed to support virtualization. Virtualization facilitates multiple virtual machines to run on a single physical server, maximizing resource utilization and reducing hardware costs. CPU data center processors include features like hardware-assisted virtualization, improving virtualized environments' performance and security.

- One of the primary market drivers is the exponential growth of data generated by various sources like mobile devices, social media, and the Internet of Things. This vast amount of data must be processed and analyzed in real time, requiring powerful, high-performance processors. As the market for data processing continues to grow, data center operators are compelled to invest in advanced CPU processors to meet the increasing computational requirements.

- The rapid expansion of cloud computing services is also anticipated to drive market growth significantly. Cloud platforms have become essential to many businesses, offering scalability, flexibility, and cost-efficiency. To support the growing demand for cloud services, data centers must deploy processors that can handle the heavy workloads and provide optimal performance. As a result, there is a constant need for more robust and energy-efficient CPU processors to cater to the evolving requirements of cloud computing.

- According to Cloudscene, as of March 2024, there were a reported 5,381 data centers in the United States, the most of any country worldwide. A further 521 were in Germany, while 514 were in the United Kingdom. The increasing investments in data centers in several regions are likely to aid the growth of the market. For instance, in October 2023, Vantage Data Centers closed an investment deal for several European data center assets. The company announced it had completed an investment partnership with DigitalBridge and a consortium of investors led by Infranity and MEAG. The investment partnership initially comprises six stabilized European data centers and is valued at approximately USD 2.7 billion, including Vantage's stake.

North America Holds the Largest Market Share

- The American data center processor market has experienced substantial growth due to technological advancements, the proliferation of data-intensive applications, and the need for high-performance computing. The migration of businesses to cloud-based solutions has fueled the demand for robust data centers in North America. This has driven the need for powerful processors that can handle the increasing volume of data and provide seamless performance.

- The high adoption of the Internet and advanced technologies like AI, 5G, IoT, and high-performance computing in the United States is driving the need for a high data transmission rate, which drives the market's growth. According to Meltwater, a software-as-a-service solution company and an online media monitoring company, as of October 2023, the internet penetration rate in the United States was 91.8%.

- Data centers consume large amounts of energy, resulting in heightened operational costs and environmental concerns. As a result, there is a rising emphasis on energy-efficient processors that can optimize power consumption without compromising performance.

- Data centers are embracing heterogeneous computing architectures to meet the region's requirements of emerging technologies like AI and machine learning. This trend has led to the integration of CPUs, GPUs, and specialized accelerators, offering superior performance and flexibility.

- The upsurge in data traffic has created elevated demand for developing several data centers that support data generated by businesses and consumers. The use of cloud-computing services and applications will continue to grow in the US, leading to the development of large hyperscale cloud-based data centers.

- Several companies are investing in data center capacity expansions in the region, thereby driving the expansion of the optical transceiver market. For instance, in September 2023, Amazon announced it would invest USD 3.5 billion in five new data centers in New Albany, Ohio, United States. It is reported that they will be finished by 2030. The construction is set to commence in 2025 on the five data centers and supporting buildings. The investment is claimed to be an initial part of Amazon's USD 7.8 billion commitment to expand data centers in the state. The agreement follows Google's recent announcement of a planned USD 1.7 billion expansion of its three data centers in New Albany.

Data Center Processor Industry Overview

The data center processor market is semi-consolidated with significant players like Intel Corporation, NVIDIA Corporation, Advanced Micro Devices Inc., Xilinx Inc., and Arm Holdings PLC. The players in the studied market are striving to constantly innovate advanced products to cater to the evolving needs of consumers.

February 2024: Nvidia announced that it ramped up GPU production to fuel the AI data center revolution. The company launched optimizations for Google's newly released Gemma family of lightweight models. The two companies developed architecture to accelerate the model's performance running in Nvidia data centers, in the cloud, and on GPU-enhanced PCs. The initial stock of Nvidia's H200 processors is set to ship in the second half of 2024.

December 2023: Intel launched its 5th-generation Xeon Scalable processors at the AI Everywhere event in New York. Intel released the fourth generation of its Intel Xeon processors in January 2023, but to keep pace with its competitors, it has unveiled the fifth generation of the chips, also known by its code name Emerald Rapids. These new processors offer a 21% average compute performance gain and 16% better memory speeds than the previous generation of Xeon processors, Sapphire Rapids, enabling 36% higher average performance per watt across a diverse range of customer workloads - Intel claims. This would facilitate users' undertaking processor-intensive tasks while utilizing less overall power, with Intel describing them as their most sustainable data center processors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technology Snapshot

- 4.2.1 Impact of Deep Learning, Public Cloud Interface, and Enterprise Interface on Data Center Accelerators

- 4.2.2 Technological Updates/Developments by Various Vendors

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

- 4.6 Market Scenario Based on the Setup - On-premise vs Cloud

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Deployment of AI in HPC Data Centers

- 5.1.2 Increasing Deployment of Data Center Facilities and Cloud-based Services

- 5.2 Market Restraints

- 5.2.1 Limited AI Hardware Experts and Infrastructural Concerns

6 MARKET SEGMENTATION

- 6.1 By Processor

- 6.1.1 CPU (Central Processing Unit)

- 6.1.2 GPU (Graphics Processing Unit)

- 6.1.3 FPGA (Field-programmable Gate Array)

- 6.1.4 ASIC (Application-specific Integrated Circuit) - Only AI-dedicated Accelerators

- 6.1.5 Networking Accelerators (SmartNIC and DPUs)

- 6.2 By Application

- 6.2.1 Artificial Intelligence (Deep Learning and Machine Learning)

- 6.2.2 Data Analytics/Graphics

- 6.2.3 High-performance Computing (HPC)/Scientific Computing

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Intel Corporation

- 7.1.2 NVIDIA Corporation

- 7.1.3 Advanced Micro Devices Inc.

- 7.1.4 Xilinx Inc.

- 7.1.5 Arm Holdings PLC

- 7.1.6 Super Micro Computer Inc.

- 7.1.7 Samsung Electronics Co. Ltd

- 7.1.8 Qualcomm Technologies Inc.

- 7.1.9 Imagination Technologies Limited

- 7.1.10 Advantech Co. Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET