PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549964

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549964

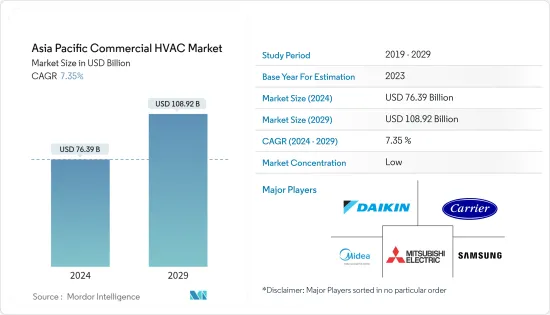

Asia Pacific Commercial HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Asia Pacific Commercial HVAC Market size is estimated at USD 76.39 billion in 2024, and is expected to reach USD 108.92 billion by 2029, growing at a CAGR of 7.35% during the forecast period (2024-2029).

Key Highlights

- The APAC commercial HVAC market is predicted to rise steadily due to increasing investments in commercial construction activity in developing economies in the region. In addition, the region's strong economic growth, urbanization, and expanding consumer market drive demand for commercial spaces, which is expected to increase the demand for innovative and high-quality HVAC equipment and services.

- Significant drivers of the regional HVAC equipment market's growth in the commercial industry over the forecast period include the surging demand for energy-efficient and sustainable technologies. According to the IEA, electricity consumption in Southeast Asia is expected to double by 2040, with air conditioning systems becoming a significant contributor to overall and peak electricity requirements. The study by the IEA highlights the urgent need to find sustainable solutions for meeting growing energy demand in the region.

- Several regional governments have established rules and regulations in the market that adhere to sustainability and energy efficiency, which expedites technological developments in the market. For instance, in February 2024, Panasonic unveiled its 2024 air conditioner lineup, prominently featuring its range of Matter-enabled room ACs. Matter, a cutting-edge connectivity standard for smart home appliances, facilitates seamless interoperability via brand-agnostic mobile apps. This move positions Panasonic as the pioneer in India, being the first to introduce ACs adhering to this protocol. The brand's launch encompasses a diverse portfolio, with 60 models spanning 1.0-ton, 1.5-ton, and 2.0-ton variants, all equipped with Matter technology.

- The commercial space's heating, ventilation, and air conditioning sectors are changing. The cooling and heating units are smaller, more compact, and more efficient than ever. However, manufacturers and service providers must keep pace with these technological developments. The need for more skilled workers is a significant problem for several regional companies. The HVAC services are often time-consuming and entertaining and need a supervisor to supervise the entire process and closing phase, apart from those installing the necessary equipment. Team management is a real challenge when handling several projects simultaneously.

- The region is home to several HVAC manufacturers and service providers in the commercial segment. They focus on enhancing their market presence by establishing domestic manufacturing facilities to remain competitive. For instance, Japan's Daikin Industries aims to make India a central export hub to nearly triple the Made in India products sold abroad by 2025. Daikin has built a new plant in India, making room air conditioners and compressors a key component. The company will also pursue exports of Made in India aircon products to 100 markets in 2025.

- The conflict between Russia and Ukraine has caused significant problems with regional supply chains. After the COVID-19 pandemic, the region was recovering logistics and supply chains, and this conflict created new market problems. It has contributed to exacerbating existing supply chain problems like commodity exports. On the other hand, Japanese factories are directly affected by the lack of raw materials and components from Ukraine.

Asia Pacific Commercial HVAC Market Trends

Commercial Buildings Segment is Expected to Hold Significant Share

- HVAC systems are essential to any commercial building, such as restaurants, hospitals, schools, hotels, office buildings, etc., to provide occupants with a comfortable environment. For instance, HVAC systems are commonly used in many offices to provide appropriate temperature and ventilation conditions, which helps improve employee productivity and working conditions and prevent health issues caused by improper humidity levels.

- The regional commercial sector's HVAC market is predicted to increase throughout the forecast period owing to several trends, from automated systems to green and smart technology, which are anticipated to be crucial in determining the direction of the commercial HVAC market. The increasing demand for environmentally friendly and energy-efficient HVAC systems drives the segment's expansion. The development of the commercial construction sector plays a significant role in the rise of heat pumps, ACs, air handlers, and other HVAC equipment.

- For instance, several rules have altered the engineering of commercial rooftop air conditioners, heat pumps, and warm-air systems for low-rise buildings like retail outlets, educational facilities, and mid-level hospitals to increase RTU efficiency and reduce energy use and waste. The phasing out of CFC (chlorofluorocarbon) and HCFC (hydrochlorofluorocarbon) by several manufacturers has increased the demand for solutions to replace outdated models, which has increased the use of heat pumps.

- Energy consumption in the commercial sectors is gradually increasing in several regional countries, fueling the market's growth to innovate energy-efficient HVAC products. For instance, in China, the secondary sector, which includes commercial and industrial sectors, accounted for 6,070 terawatt hours of electricity consumption.

China is Expected to Witness Significant Growth in the Market

- The demand for commercial HVAC equipment in the region has witnessed significant growth opportunities over the past few years. China is one of the essential markets for data center cooling due to the exponential growth in the number of data centers and the government's policies to support more energy-efficient infrastructure in the country. According to Cloudscene, China has the most significant number of data centers in Asia, with 448.

- In March 2024, an official from China's Ministry of Industry and Information Technology (MIIT) announced that China is gearing up to pilot the opening-up of internet data centers. As China pushes for new industrialization, it is imperative to deepen reforms and broaden its scope of opening-up. Notably, China has made headlines by declaring a complete removal of restrictions on foreign investments in manufacturing. In tandem, the MIIT is gearing up to test the waters by opening up value-added telecommunications services, with a specific focus on internet data centers. This expansion offers a massive opportunity for the vendors in the market studied.

- The construction industry in China has witnessed massive growth due to sustainable construction policies and a shift toward a service-led economy over the past few years. Investing in large-scale infrastructure projects has been a vital part of the Chinese government's strategy to boost growth. According to EPRA, as of December 2023, China's commercial real estate market was worth nearly as much as all Asia-Pacific combined, which was USD 5.6 trillion.

- The increase in commercial buildings is estimated to affect national energy consumption directly, which is why the Chinese government has taken energy management seriously. Two laws, the Energy Saving Law and Renewable Energy Law, provide the main guidelines for building energy systems and HVAC industries.

Asia Pacific Commercial HVAC Industry Overview

The Asia-Pacific commercial HVAC market is highly competitive, with several global and regional players. The players are emphasizing strategic initiatives like innovations, partnerships, mergers, and acquisitions to fulfill the surging demand of the HVAC market in the commercial sectors. Besides global players, the regional players offer HVAC equipment and services with highly advanced technologies at competitive prices. The key market players include Daikin Industries Ltd, Carrier Corporation, Midea Group Co. Ltd, Mitsubishi Electric, and Samsung HVAC LLC.

- January 2024: Carrier expanded its HVAC products made in India with a range of air handling units (AHUs) and fan coil units (FCUs) that meet the diverse needs of commercial buildings by providing custom solutions for healthy indoor environments and high-efficiency air filtration requirements. The expansion to FCUs and AHUs affirms more than a five-decade manufacturing presence in India.

- August 2023: Daikin Industries Ltd decided to acquire land in Tsukubamirai City, Ibaraki Prefecture, Japan, to establish a new production base for air conditioners. The company intends to optimize the domestic supply of air conditioning products in Japan to expand further when it locates its new factory in the Kanto region. It will be Daikin's first air conditioning plant in the Kanto region.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Energy Efficiency and Sustainable Technology

- 5.1.2 Increasing Investment Toward Commercial Real-Estate in the Region

- 5.2 Market Restraints

- 5.2.1 Lack of Skilled Workforce and Training to Perform Routine Tasks like Installations and Repair

6 MARKET SEGMENTATION

- 6.1 By Type of Component

- 6.1.1 HVAC Equipment

- 6.1.1.1 Heating Equipment

- 6.1.1.2 Air Conditioning/Ventilation Equipment

- 6.1.2 HVAC Services

- 6.1.1 HVAC Equipment

- 6.2 By End-user Industry

- 6.2.1 Hospitality

- 6.2.2 Commercial Buildings

- 6.2.3 Public Buildings

- 6.2.4 Other End-user Industries

- 6.3 By Country

- 6.3.1 China

- 6.3.2 India

- 6.3.3 Japan

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Daikin Industries Ltd

- 7.1.2 Carrier Corporation

- 7.1.3 Johnson Controls International PLC

- 7.1.4 Mitsubishi Electric

- 7.1.5 Trane Technologies

- 7.1.6 Samsung HVAC LLC

- 7.1.7 LG Electronics

- 7.1.8 Panasonic Corporation

- 7.1.9 Lennox International Inc.

- 7.1.10 Midea Group Co. Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET