PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1694043

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1694043

Europe Automotive Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

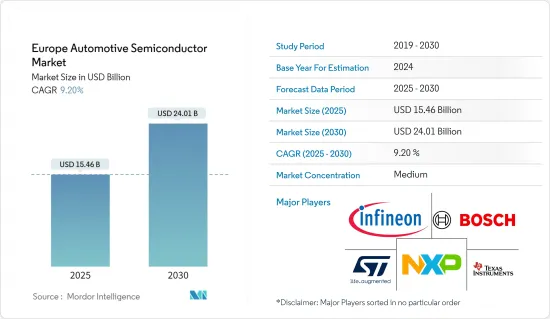

The Europe Automotive Semiconductor Market size is estimated at USD 15.46 billion in 2025, and is expected to reach USD 24.01 billion by 2030, at a CAGR of 9.2% during the forecast period (2025-2030).

Key Highlights

- An automotive semiconductor is a type of semiconductor chip specifically designed and used in the automotive industry. These chips play a crucial role in the functioning of various electronic components and systems in vehicles. They are responsible for powering and controlling many features and functions, including safety systems, infotainment systems, engine control units, sensors, etc.

- Automotive semiconductors have become increasingly important as vehicles have become more technologically advanced. They are essential for integrating advanced technologies such as autonomous driving, electric powertrains, and connected car systems. These semiconductors are designed to meet the specific requirements of the automotive industry, including durability, reliability, and the ability to operate in harsh environments.

- One of the primary applications of automotive semiconductors is in Advanced Driver Assistance Systems (ADAS). These systems use sensors, cameras, and processors to enhance vehicle safety and assist drivers in real-time. Semiconductors enable features like adaptive cruise control, lane-keeping assist, automatic emergency braking, blind-spot detection, and pedestrian detection, making driving safer and reducing the risk of accidents.

- Semiconductors play a crucial role in developing advanced infotainment systems in vehicles. These systems provide a seamless integration of entertainment, navigation, and communication features. Automotive semiconductors enable touchscreens, voice recognition, connectivity options, and multimedia playback, transforming the driving experience into a personalized and connected one.

- The increasing investments in the automotive semiconductor industry in Europe are likely to aid the development of the market studied. For instance, in August 2023, Robert Bosch GmbH, TSMC, NXP Semiconductors NV, and Infineon Technologies AG announced a plan to jointly invest in ESMC (European Semiconductor Manufacturing Company GmbH) in Dresden, Germany, to offer advanced semiconductor manufacturing services. ESMC is claimed to mark a substantial step toward constructing a 300 mm fab to support the future capacity requirements of the fast-growing automotive and industrial sectors.

- The project is designed under the framework of the European Chips Act. The planned fab is anticipated to have a monthly production capacity of 40,000 wafers (12-inch) on TSMC's 28/22 nanometer planar CMOS and 16/12 nanometer FinFET process technology, bolstering Europe's semiconductor manufacturing ecosystem with advanced FinFET transistor technology and creating approximately 2,000 direct high-tech professional jobs. ESMC seeks to begin construction of the fab in the second half of 2024, with production targeted to commence by the end of 2027.

- Semiconductors enable vehicle connectivity, forming the foundation for connected car technology. They power wireless communication systems, allowing vehicles to connect with other vehicles (V2V), infrastructure (V2I), and the internet (V2X). This connectivity facilitates real-time data exchange, enabling features like traffic updates, remote vehicle diagnostics, over-the-air updates, and even autonomous driving capabilities.

- With the increasing concern for environmental sustainability and the necessity to reduce carbon emissions, electric vehicles (EVs) have gained immense popularity in Europe. EVs rely heavily on semiconductor technology for power management, battery management, and motor control systems. As the demand for EVs continues to rise, so does the demand for automotive semiconductors.

- According to the European Automobile Manufacturers Association (ACEA), the sales volume of battery electric (BEV) and plug-in hybrid electric vehicles (PHEV) in Europe increased from 559.81 thousand in Q2 2022 to 757.83 thousand in Q3 2023. Such an increase in the demand for EVs would offer lucrative opportunities for the growth of the studied market.

- However, the high cost of development and production is a significant barrier to the growth of the market studied. The complex manufacturing processes and testing requirements make these semiconductors expensive, limiting their affordability for both manufacturers and consumers.

- Furthermore, the conflict between Russia and Ukraine is expected to significantly impact the semiconductor industry. The conflict has already exacerbated the electronics & semiconductor supply chain issues and the chip shortage that have affected the industry for some time. The disruption may result in volatile pricing for critical raw materials such as nickel, palladium, copper, titanium, and aluminum, resulting in material shortages. This, in turn, could impact the manufacturing of automotive semiconductors.

Europe Automotive Semiconductor Market Trends

The Passenger Vehicles Segment is Expected to Drive the Market's Growth

- Automotive semiconductors find applications in various safety systems within passenger vehicles. These semiconductors are used in power electronics modules that control the anti-lock braking system (ABS), electronic stability control (ESC), and advanced driver-assistance systems (ADAS). By accurately monitoring and adjusting power flow, these systems enhance vehicle stability, traction, and overall safety.

- Moreover, automotive semiconductors play a crucial role in power management within passenger vehicles. These semiconductors are used in DC-DC converters, voltage regulators, and other power control modules, ensuring efficient power distribution and optimal utilization of electrical energy.

- These tiny electronic components are integrated into different systems within the vehicle, enabling advanced safety features and ensuring a safer driving experience. One of the primary applications of automotive semiconductors in passenger vehicle safety is the anti-lock braking system (ABS). ABS relies on sensors and microcontrollers to monitor wheel speed and prevent wheel lock-up during sudden braking. By rapidly modulating brake pressure, automotive semiconductors help maintain vehicle stability, prevent skidding, and reduce the risk of accidents.

- They are also employed in electronic stability control (ESC) systems. ESC uses sensors, accelerometers, and microcontrollers to monitor vehicle dynamics and apply selective braking to individual wheels. Automotive semiconductors enable real-time data processing and precise control, enhancing vehicle stability and preventing loss of control in hazardous situations.

- The increasing automotive production in Europe is likely to increase the demand for automotive semiconductors. For instance, according to OICA, around 1.5 million motor vehicles were produced in France in 2023, 68.2% of which were passenger cars. In 2022, approximately 1.3 million cars were produced in France.

- Furthermore, the proliferation of connected car technologies has transformed the way users interact with vehicles. From infotainment systems to advanced driver assistance systems (ADAS), connected car technologies rely on semiconductor chips to enable seamless communication and data processing. With the increasing integration of internet connectivity, cloud services, and data analytics in vehicles, the demand for automotive semiconductors is expected to grow exponentially.

Germany is Expected to Witness High Market Growth Rate

- Germany, known for its strong automotive industry, has established itself as one of the leading players in the global automotive semiconductor market. With a robust ecosystem of automotive manufacturers, suppliers, and technology companies, Germany has become a hub for semiconductor development and production. Semiconductor companies like Infineon Technologies, Bosch, and Continental AG have a significant presence in Germany. These companies specialize in producing a diverse range of automotive semiconductors, including microcontrollers, sensors, power management ICs, and connectivity solutions.

- German semiconductor companies often collaborate with automotive manufacturers, research institutions, and start-ups to foster innovation, drive technological advancements, and enhance their market capitalization.

- For instance, in January 2024, Infineon Technologies AG and GlobalFoundries announced a new multi-year agreement on the supply of Infineon's AURIX TC3x 40 nanometer automotive microcontrollers and power management and connectivity solutions. The additional capacity is anticipated to contribute to secure Infineon's business growth from 2024 through 2030. At the center of this collaboration is claimed to be a highly reliable embedded non-volatile memory technology solution that is designed to enable mission-critical automotive applications while satisfying the stringent safety and security requirements for next-generation vehicle systems.

- The increasing automobile production in Europe is likely to augment the demand for the market studied. For instance, according to the International Organization of Motor Vehicle Manufacturers (OICA), in 2023, Germany was the largest automobile manufacturing country in Europe, with approximately 4.1 million vehicles produced.

- The increasing demand for electric vehicles (EVs) and autonomous driving systems has driven the development of specialized semiconductors to meet the unique requirements of these applications. For instance, according to the Kraftfahrt-Bundesamt (Federal Motor Transport Authority - KBA), the number of new electric cars registered in Germany has grown significantly in recent years, increasing from 470,559 in 2022 to 524,219 in 2023.

- Automotive manufacturers in Germany are constantly striving to improve the energy efficiency of vehicles. Semiconductor technology enables more efficient power management and control systems, resulting in decreased energy consumption and increased overall efficiency. With stricter regulations on fuel economy and emissions, the demand for automotive semiconductors that contribute to energy-efficient solutions will continue to rise.

- Autonomous driving is the future of transportation, and semiconductors are at the heart of this technological revolution. These components power the advanced sensors, cameras, LiDAR, radar, and AI processors that enable autonomous vehicles to perceive, interpret, and respond to their surroundings. Semiconductors facilitate complex decision-making algorithms, ensuring the safety and reliability of autonomous driving systems. German semiconductor companies are at the forefront of developing sensors, vision systems, and AI chips that enable vehicles to perceive their surroundings and make intelligent decisions in real time.

Europe Automotive Semiconductor Industry Overview

The European automotive semiconductor market is a semiconsolidated market with the presence of several prominent market players like NXP Semiconductors NV, Infineon Technologies AG, STMicroelectronics NV, Texas Instruments Inc., Robert Bosch GMBH, Micron Technology Inc., etc. The market players are striving to innovate new products by way of extensive investments in R&D, collaborations, and mergers to cater to the evolving demands of consumers.

- January 2024: Texas Instruments introduced new semiconductors designed to enhance automotive safety and intelligence. The AWR2544 77 GHz millimeter-wave radar sensor chip is designed for satellite radar architectures, enabling higher levels of autonomy by improving sensor fusion and decision-making in ADAS.

- August 2023: STMicroelectronics NV, one of the largest European semiconductor contract manufacturing and design companies, and BorgWarner, an American automotive supplier, joined forces to integrate SiC technology into BorgWarner's VIPER power modules. This integration strives to support Volvo Cars' transition to full vehicle electrification by 2030.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19, Aftereffects, and Other Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Vehicle Production and Adoption of EVS

- 5.1.2 Growing Demand For Advanced Safety and Comfort Systems Augmented by Government Regulations

- 5.2 Market Restraint

- 5.2.1 Increasing Costs Associated With Growing Advance Features

6 MARKET SEGMENTATION

- 6.1 Vehicle Type

- 6.1.1 Passenger Vehicle

- 6.1.1.1 Discrete

- 6.1.1.2 Optoelectronics

- 6.1.1.3 Sensors and Actuators

- 6.1.1.4 Logic

- 6.1.1.5 Memory

- 6.1.1.6 Analog IC

- 6.1.1.7 Micro

- 6.1.2 Light Commercial Vehicle

- 6.1.2.1 Discrete

- 6.1.2.2 Optoelectronics

- 6.1.2.3 Sensors and Actuators

- 6.1.2.4 Logic

- 6.1.2.5 Memory

- 6.1.2.6 Analog IC

- 6.1.2.7 Micro

- 6.1.3 Heavy Commercial Vehicle

- 6.1.3.1 Discrete

- 6.1.3.2 Optoelectronics

- 6.1.3.3 Sensors and Actuators

- 6.1.3.4 Logic

- 6.1.3.5 Memory

- 6.1.3.6 Analog IC

- 6.1.3.7 Micro

- 6.1.1 Passenger Vehicle

- 6.2 Application

- 6.2.1 Chassis

- 6.2.2 Power Electronics

- 6.2.3 Safety

- 6.2.4 Body Electronics

- 6.2.5 Comfort/Entertainment Unit

- 6.2.6 Other Applications

- 6.3 Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Italy

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 NXP Semiconductor NV

- 7.1.2 Infineon Technologies AG

- 7.1.3 Renesas Electronics Corporation

- 7.1.4 STMicroelectronics NV

- 7.1.5 Toshiba Electronic Devices & Storage Corporation (Toshiba Corporation)

- 7.1.6 Texas Instrument Inc.

- 7.1.7 Robert Bosch GmbH

- 7.1.8 Micron Technology Inc.

- 7.1.9 Onsemi (Semiconductor Components Industries LLC)

- 7.1.10 Analog Devices Inc.

- 7.1.11 ROHM Co. Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET