Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549925

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549925

United Kingdom DC Motor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

PUBLISHED:

PAGES: 90 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

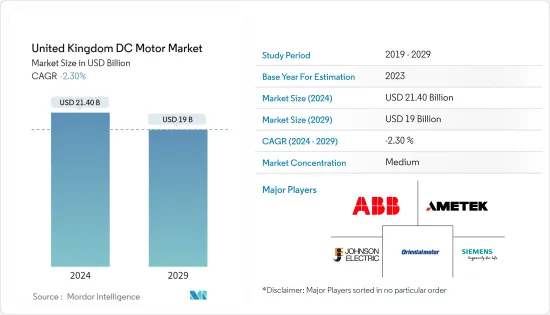

The United Kingdom DC Motor Market size is estimated at USD 21.40 billion in 2024, and is expected to decline to USD 19 billion by 2029.

Key Highlights

- The declining sales of DC motors are attributed to the increasing adoption of alternative motor technologies such as AC motors, which are highly durable, have a longer life span, and require little maintenance. However, DC motors favor industrial applications demanding consistent low-speed torque or precise speed adjustments. They originated from the early days of electricity experiments and have evolved into a cornerstone of industrial operations and contemporary robotics.

- DC motors are sought for efficiency, aligning with the UK's sustainability goals. Their ability to provide precise control over speed and torque makes them ideal for applications demanding accuracy, especially in automation. Energy scarcity and escalating costs pose significant challenges for the nation. DC motor controllers achieve this by dynamically regulating the speed and power consumption of DC motors, tailoring them to real-time needs. Such precision not only aids industries in curbing energy wastage but also bolsters their efforts to meet global sustainability targets and slash carbon footprints.

- Moreover, as the United Kingdom continues to emphasize renewable energy sources, DC motors are often used in renewable energy systems, contributing to the country's clean energy initiatives. According to the Green Industrial Revolution, the UK government invested around GBP 40 billion (USD 50.3 billion) in the last two years. By the end of 2023, they were expected to increase their capacities by 15%.

- Additionally, Industry 4.0 is a key driver propelling the market's growth. This push toward automation enhances productivity across manufacturing sectors across the country, with a particularly robust outlook for the forecast period. These motors power core industrial processes and play a vital role in auxiliary systems like compressed air generation, ventilation, and water pumping, making them indispensable across industries.

- However, the initial costs of DC motors and associated control systems, which could impact their adoption, especially in the case of budget-sensitive projects, may be higher than for other motor types. In addition, there is a risk of such motors becoming obsolete due to their limitations in terms of control and compatibility with modern systems. During the forecast period, integrating DC motor technology with current systems may pose problems hindering its uptake in specific industry sectors with already existing infrastructure.

United Kingdom DC Motor Market Trends

Permanent Magnet DC Motor (PMDC) is Expected to Hold A Significant Share

- A permanent magnet DC motor (PMDC) is a type of DC motor that uses permanent magnetic magnets on the rotor rather than field windings. Permanent magnets produce a magnetic field that interacts with the magnetic field produced by the motor windings, creating rotation in the rotor.

- The PMDC motors are known for their high energy efficiency, which matches the United Kingdom's focus on reducing energy consumption and greenhouse gas emissions. Companies are helping to achieve energy efficiency targets and reduce operating costs using efficient motors.

- Regulations and initiatives supporting sustainable practices and reducing carbon emissions were put in place by the UK government. The PMDC motors are compatible with these environmental regulations and contribute to achieving sustainability targets due to their high efficiency and reduced energy consumption.

- These motors are suited for applications with limited space due to their narrow size and muscular power density. In particular, this is important in the United Kingdom, where offshore platforms and modular equipment configurations are common in the oil and gas sector. In addition, the UK has been moving toward renewables for some time. It is easy to integrate PMDC motors, with their high efficiency, into renewable energy sources like wind turbines and photovoltaic panels. They can efficiently use renewable energy as mechanical power for different oil and gas sector uses.

- PMDC motors are known for their reliability and ability to withstand harsh operating conditions. Equipment capable of being resilient to extreme temperatures, humidity, and corrosive conditions is needed in the UK's offshore oil and gas drilling operations, which are often faced with challenging environments. The PMDC motor is preferred for such applications due to its robustness and durability.

- Moreover, according to a recent Baker Hughes report, the United Kingdom had 49 offshore oil rigs as of September 2023, an increase from 39 in August 2023. This trend is expected to propel the PMDC motor demand during the forecast period.

The Oil and Gas End-user Industry is Expected to Hold A Significant Share

- Due to their inherent advantages, DC motors have extensive applications in the oil and gas sector. Their ability to deliver high torque at lower speeds makes them ideal for critical operations like pumping, drilling, and extraction. This precise speed and position control, a hallmark of DC motors, is crucial in tasks ranging from regulating pump speeds to managing compressors and actuators.

- The DC motors enable the variable speed to be controlled smoothly and efficiently. This is especially useful for applications where the speed requirements are regularly changed to optimize energy efficiency and improve process control. The durability and reliability of DC motors, which can be adapted to the harsh operating conditions that commonly exist in the oil and gas sector, e.g., high temperatures, corrosive environments, or vibration, make them well suited for their applications.

- The United Kingdom's oil and gas industry uses permanently magnetized DC motors, which are small but have a high power density. They are used for pumps, valves, winches, and others that need large torques and compact packaging. The series wound DC motors are used for applications such as lifts, cranes, or drilling equipment because they generate a higher start torque and take on an even heavier load. Shunt wound DC motors offering reasonable speed control are used in various installations. They are used in the case of fans, blowers, centrifugal compressors, and other applications for which continuous speed under varying load conditions is required.

- Further, the UK government actively promotes energy efficiency and environmental sustainability in many applications in the oil and gas industry. Regulations and initiatives are in place to encourage the use of energy-efficient technologies and reduce carbon emissions. These regulations promote the production of energy-efficient motors, e.g., DC motors, using incentive payments, tax rebates, or requirements for compliance with specific energy efficiency standards.

- As of 2023, the Office for National Statistics (UK) reports that there are 40 oil and gas extraction companies in the United Kingdom with an annual turnover of more than GBP 5 million (>USD 6.4 million). Increasing turnover of oil and gas extraction companies will encourage them to work in this sector, which will concurrently drive the market growth of DC motors in the coming period.

United Kingdom DC Motor Industry Segmentation

The UK DC motor market is partially consolidated with major global and regional players. The players use advanced technologies to take strategic initiatives like partnerships, collaborations, mergers, acquisitions, and new product developments. These initiatives help the company to be competitive in the market. Some of the recent developments include,

- May 2024: Maxon announced broadening its flat motor offerings with the introduction of the EC frameless DT 38 S and EC frameless DT 38 M. These kits, featuring BLDC motors and internal rotor technology, boast a sleek design, robust torques, and ample room for cable penetrations, facilitating seamless integration across diverse applications.

- January 2024: Parvalux inaugurated its new headquarters in Poole, Dorset. This consolidated its operations, previously scattered across three locations. Parvalux proudly asserts its position as the UK's primary producer of fractional horsepower, geared electric motors. The offerings span from AC motors up to 250W to permanent magnet DC motors and brushless DC motors reaching 600W.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50002569

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand of Energy-efficient DC Motors

- 5.2 Market Restraints

- 5.2.1 High Initial Installation Cost

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Permanent Magnet

- 6.1.2 Separately Excited

- 6.1.3 Self Excited

- 6.1.3.1 Shunt

- 6.1.3.2 Series

- 6.1.3.3 Compound

- 6.2 By End-user Industry

- 6.2.1 Oil and Gas

- 6.2.2 Chemical and Petrochemical

- 6.2.3 Power Generation

- 6.2.4 Water and Wastewater

- 6.2.5 Metal and Mining

- 6.2.6 Food and Beverages

- 6.2.7 Discrete Industries

- 6.2.8 Other End-user Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Limited

- 7.1.2 AMETEK Inc.

- 7.1.3 Johnson Electric Holdings Limited

- 7.1.4 Nidec Corporation

- 7.1.5 Siemens AG

- 7.1.6 Oriental Motor (UK) Ltd

- 7.1.7 Buhler Motor GmbH

- 7.1.8 Maxon

- 7.1.9 Faulhaber Group

- 7.1.10 Regal Rexnord Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.