Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549922

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549922

Europe Wire And Cable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

PUBLISHED:

PAGES: 120 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

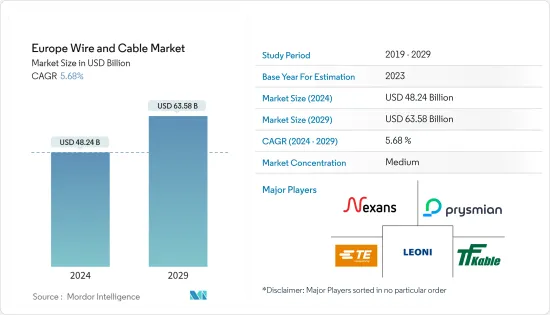

The Europe Wire And Cable Market size is estimated at USD 48.24 billion in 2024, and is expected to reach USD 63.58 billion by 2029, growing at a CAGR of 5.68% during the forecast period (2024-2029).

Key Highlights

- The European wire and cable market is consistently growing, fueled by increasing demand across diverse sectors. Escalating infrastructure projects and technological innovation are streamlining energy transmission and data communication. There has been growing investment in European cities toward intelligent city initiatives, focusing on adopting innovative, sustainable solutions to enhance efficiency and environmental footprint over the last 10 years. Thus, developing a good communication infrastructure requires deploying fiber optic cables, which drive the market's growth.

- Wire and cables play a significant role in efficient and safe electricity transmission, especially from renewable sources. Europe's ambitious goals to diversify its energy mix have led to a surge in projects focusing on cleaner and more sustainable energy production. These projects leverage various sources, such as wind, hydroelectric, photovoltaic solar, biomass, and geothermal energy. By 2022, renewable energy accounted for 22.2% of Europe's energy consumption. The EU aimed at a 32% renewable energy target for its gross final consumption by 2030.

- The rise of Industry 4.0 and automation adoption in manufacturing sectors led to the increased use of control and instrumentation cables. Industry 4.0's rise signifies a pivotal transition, with businesses now seamlessly using the Internet of Things (IoT), machine learning, and extended reality (XR) in their operations. These combined capabilities are reshaping industries' efficiency, productivity, and innovation.

- Several European nations lack domestic refined copper production, constraining market expansion. With a growing appetite for new establishments, the demand for copper rods is surging. However, intensive reliance on raw material imports is a challenge for the region. Moreover, the industry grapples with the dual challenge of managing both raw material costs and navigating volatile prices.

- After the COVID-19 pandemic, there has been an increasing demand for building 5G infrastructure, which allows for faster internet speeds and higher bandwidths to facilitate managing the large workloads of organizations on cloud platforms. Additionally, rising government funding and investments by numerous companies for 5G deployment across Europe are also driving the telecom market growth in Europe, thus facilitating wire and cable growth.

Europe Wire And Cable Market Trends

The Power Cables Segment is Expected to Witness a Major Growth

- The surge in power cable growth is experiencing increasing demand for power infrastructure, renewable energy initiatives, and transportation electrification. With a global shift toward sustainable energy and the expansion of electrical grids, the need for high-capacity power cables is increasing, propelling their rapid growth.

- There are growing government initiatives in European countries promoting energy efficiency and environmental sustainability. The installation of solar power plants and wind farms is increasing, driving the market for specialized power cables that can handle high voltage and withstand harsh environmental conditions. As per data by EurObserv'ER, the solar annual electricity generation is constantly increasing from 60,304 GW hours in 2022 to 61,216 GW hours in 2023, which signifies the growth of the sector.

- The Spanish robust solar sector has several large projects in various development phases. One of the crucial projects is the Zaragoza Solar Park, an 11.8MW solar PV power project situated in Aragon, Spain. Currently in the development stage, the Zaragoza and Teruel greenfield project is on track for commissioning in 2024. This project is under the ownership of Bruc Iberia Energy Investment Partners. Boasting a single-phase development plan and aiming for 2580 MWp/dc capacity, this solar farm is planned to rank among Europe's largest. These large-scale projects are propelling the market's growth in Europe.

- Moreover, the development of smart grids in Europe requires new and upgraded power cables and enables communication and digital communication efficiently. A smart grid is an electricity network that efficiently coordinates the actions of all its users, including both generators and consumers. Its goal is to create an economically efficient, sustainable power system, ensuring high-quality, secure, and safe power supply. With smart grids, businesses and households can generate electricity through photovoltaic panels or wind turbines and distribute it directly to other consumers via the grid.

- The ongoing urban development and construction of new residential, commercial, and industrial projects increase the demand for power cables. The UK construction industry, as per the Office for National Statistics, saw its GVA (Gross Value Added) rise from GBP 33.36 billion in Q1 2022 to GBP 37.41 billion in Q1 2023. Notably, private housing emerged as the dominant segment in the UK's construction landscape, driving a significant portion of the industry's output.

Germany is Expected to Hold a Major Share in the Market

- Germany is known for its investments in wind, solar, and hydroelectric power projects, which involve extensive cabling networks for transmission and distribution. For instance, in 2023, Germany saw its renewable energy sources account for 22% of its total energy consumption. This uptick was primarily driven by the consistent growth of solar and wind power installations in electricity generation, coupled with a rising adoption of renewable heating systems, as the Federal Environment Agency (UBA) reported. As per data by BMWK (German Ministry), the investment in renewable energy plants reached USD 40.39 billion in 2023, compared to USD 23.77 billion in 2022.

- German companies invest in research and development, which helps develop innovations in cable technology, including higher efficiency, improved durability, and environmental sustainability. Moreover, adopting Industry 4.0 practices helps integrate smart technologies into manufacturing processes, which helps grow the sector.

- In June 2024, Amprion, the German transmission system operator (TSO), announced that it received two high-voltage direct current (HVDC) cable projects, valued at over USD 3.3 billion (EUR 3 billion), from Sumitomo Electric, a Japanese firm. Sumitomo Electric plans to manufacture these cables in Germany, a move facilitated by its acquisition of a 90% stake offering from Suedkabel, a prominent German high-voltage cable manufacturer. As part of the agreement, Sumitomo Electric is bolstering Suedkabel's capital by USD 32.39 million (EUR 30 million) and further injecting USD 97.17 million (EUR 90 million) to bolster the manufacturer's cable production capabilities.

- Germany Trade and Invest supports small and medium-sized companies, with a particular focus on aiding their digitalization efforts. The Mittelstand 4.0 Competence Centers play a pivotal role in this by raising awareness about digitalization and offering comprehensive support. This support encompasses information dissemination, training sessions, and hands-on opportunities to explore and test advanced solutions nationwide. Furthermore, universities and research institutes contribute by offering dedicated test and demonstration labs tailored for Industries 4.0 applications.

- Additionally, investment in infrastructure development, which includes smart grids, transportation networks, and telecommunication systems, is expected to drive the market for different types of cables. The government support for infrastructure development also ensures a steady demand for wires and cables.

Europe Wire And Cable Industry Overview

The European wire and cable market is competitive and fragmented, as it currently consists of various significant players. Some key players are Nexans SA, Prysmian SpA, Leoni AG, TE Connectivity, and TELE-FONIKA Kable SA. Several key players in the market are constantly striving to bring advancements.

- April 2024: NKT AS, a Danish power cable manufacturer, announced a strategic investment of approximately USD 108.5 million (EUR 100 million). This initiative is designed to accelerate its medium-voltage cable production capacity, a move prompted by the surge of demand fueled by grid modernizations and the rise of European renewable energy projects. The company anticipates enhanced production capabilities, with full operational capacity projected for 2026.

- February 2024: Nexans, a player in the global energy transition, announced a significant deal to purchase the renowned La Triveneta Cavi. La Triveneta Cavi, known for its excellence in the European medium- and low-voltage sectors, is headquartered in Italy. The company specializes in producing low-voltage cables for various applications, including building, infrastructure, fire-retardant systems, and renewable energy, distributing its products across 30 countries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50002566

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 An Assessment of the Impact of Key Macroeconomic Trends

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand From the Construction Sector

- 5.1.2 Increasing Demand from the Renewable Power Generation Sector

- 5.1.3 Increasing Adoption in the Telecommunications Industry

- 5.2 Market Restraints

- 5.2.1 High Cost of Installation and Associated Complexities

- 5.2.2 Fluctuating Raw Material Prices

6 MARKET SEGMENTATION

- 6.1 By Cable Type

- 6.1.1 Low Voltage Energy

- 6.1.2 Power Cable

- 6.1.3 Fiber Optic Cable

- 6.1.4 Signal and Control Cable

- 6.1.5 Other Cable Types

- 6.2 By End-user Vertical

- 6.2.1 Construction (Residential and Commercial)

- 6.2.2 Telecommunication (IT and Telecom)

- 6.2.3 Power Infrastructure (Energy and Power and Automotive)

- 6.2.4 Other End-user Verticals

- 6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Austria

- 6.3.6 Switzerland

- 6.3.7 Czech Republic

- 6.3.8 Poland

- 6.3.9 Denmark

- 6.3.10 Belgium

- 6.3.11 Netherlands

- 6.3.12 Luxembourg

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Nexans SA

- 7.1.2 Prysmian SpA

- 7.1.3 Leoni AG

- 7.1.4 TE Connectivity

- 7.1.5 TELE-FONIKA Kable SA

- 7.1.6 NKT AS

- 7.1.7 British Cables Company (Wilms Group)

- 7.1.8 Waskonig + Walter Kabel-Werk GmbH u. Co. KG

- 7.1.9 Habia Cable

- 7.1.10 Folan

8 LIST OF CABLE PRODUCERS AND DISTRIBUTORS (United Kingdom, Germany, France, Rest of Europe)

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITES AND FUTURE TRENDS

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.