PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1694038

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1694038

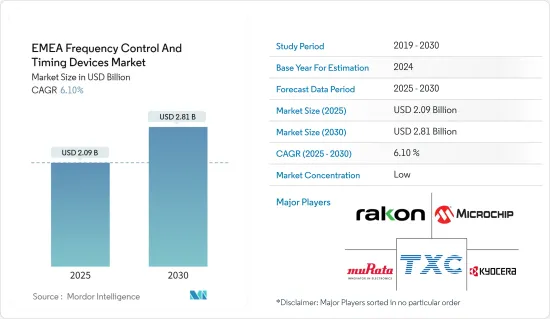

EMEA Frequency Control And Timing Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The EMEA Frequency Control And Timing Devices Market size is estimated at USD 2.09 billion in 2025, and is expected to reach USD 2.81 billion by 2030, at a CAGR of 6.1% during the forecast period (2025-2030).

The frequency control and timing device market faced significant disruptions due to the Russo-Ukraine conflict and an economic slowdown. Rising inflation and interest rates curtailed consumer spending, dampened semiconductor demand, and slowed the growth of FCTDs. In response to the conflict, Europe has shifted its focus toward the defense and aerospace sectors, leading to heightened demand for these components and opening up new growth avenues.

Key Highlights

- The rising adoption of smart home technologies creates a positive outlook for market growth. Smart homes consist of interconnected devices such as smart thermostats, lighting systems, security cameras, and appliances that need to communicate and operate seamlessly together. Frequency control and timing devices ensure the synchronization of these devices, providing accurate timing signals for data transmission, control signals, and event scheduling.

- According to the GSMA report, smartphone adoption in the MENA region is expected to increase from 54% in 2018 to 74% in 2025. By 2025, smartphones will make up 61% of all connections in Sub-Saharan Africa. Noticeably, the number of 5G connections is expected to reach 45 million and 41 million by 2025 in the MENA and Sub-Saharan African regions, respectively.

- Robots use oscillators for synchronized operation and time-sensitive tasks. The utilization of industrial robots in the region has been on the rise in numerous end-users and applications due to their ability to improve precision and adaptability, minimize product damage, enhance speed, and ultimately optimize operational efficiency.

- The rise of advanced automotive applications is a significant driver for the growth of EMEA frequency control and timing devices in the automotive industry. The increasing adoption of ADAS is a substantial contributor to the market growth. These systems rely on real-time sensor data processing for automatic emergency braking, lane departure warning, and adaptive cruise control. Frequency control devices provide the accurate timing for these systems to respond promptly and accurately.

- The frequency control and timing devices market is a critical segment within the electronics industry, providing essential components for various applications. However, the high costs of developing and producing these devices challenge the market's growth.

- Factors like GDP growth, government budget constraints, geopolitical factors, and fiscal policies significantly impact military spending in EMEA. According to NATO, in 2023, Spain's defense expenditure was estimated at USD 19.18 billion, the highest spending since 2014. The expenditure was estimated to be USD 14.90 billion in the previous year. Such figures gave Spain the eighth-highest defense expenditure among NATO members.

EMEA Frequency Control And Timing Devices Market Trends

Automotive Industry to be the Fastest Growing End User

- In the automotive industry, frequency control and timing devices are used in ADAS for adaptive cruise control, lane assistance, and collision avoidance, infotainment systems for smooth music playback and accurate GPS functionality, telematics for real-time tracking and connected vehicles, and others. They are also used in electric vehicles to coordinate the operations of electric motors.

- The automotive segment presents promising opportunities for vendors operating in the EMEA frequency control and timing devices market, as the importance of these devices has been increasing in modern automobiles.

- Autonomous driving, electrification, connectivity, and shared vehicles are the trends driving market growth in the automotive sector. Automobiles today contain several high-performance electronic systems that rely on precision timing technology for stable, accurate frequency control of digital components, ranging from application processors to microcontrollers to FPGAs. According to SiTime, a leading frequency control and timing device provider, a typical automobile uses up to 70 timing devices to keep the electrical and electronic systems operating smoothly.

- The market growth in the EMEA region may be attributed to changing consumer preferences, technological advancements, and the increasing popularity of electric vehicles. With the automotive sector shifting toward electric and connected vehicles, there will be a growing demand for oscillators. This will require manufacturers and suppliers to invest in innovative technologies to ensure vehicle safety, performance, and competitiveness.

- For instance, the car market in the European Union experienced a significant growth of 13.9% in 2023 compared to the previous year, resulting in a total sales volume of 10.5 million units for the entire year. This data was reported by the European Automobile Manufacturers' Association (ACEA).

- Battery-electric cars emerged as the third most popular choice among buyers in 2023. In December alone, their market share skyrocketed to 18.5%, contributing to an overall share of 14.6% for the entire year. This surpassed the steady market share of diesel cars, which remained at 13.6%. Petrol cars maintained their dominance with a market share of 35.3%, while hybrid-electric cars secured the second position with a commanding market share of 25.8%.

Germany to Hold Major Market Share

- Germany leads the way in Industry 4.0, where automation, data exchange, and IoT technologies converge in manufacturing. In these 'smart factories,' precise timing is crucial. It synchronizes machines, robotics, and sensors, optimizing production and resource efficiency. As Industry 4.0 takes hold, the need for advanced timing devices in industrial automation and smart manufacturing surges.

- Germany's consumer electronics and wearable devices market is driven by consumer demand for innovative gadgets and connected devices. Smartphones, wearables, and consumer electronics often incorporate timing devices for clock synchronization, data processing, and connectivity. As consumer preferences shift towards intelligent and connected devices, there's a continuous demand for compact, low-power timing solutions that may meet the requirements of modern consumer electronics products.

- According to data provided by GSMA Intelligence, Germany is projected to emerge as the leading smartphone market in Europe in terms of the number of connections, with a value of USD 105 million, by 2025. Germany's smartphone adoption rate is expected to rise from 80% in 2021 to 84% in 2025.

- In Germany, the defense and aerospace sectors increasingly demand high-performance timing solutions. These solutions find applications in radar systems, communication networks, and satellite payloads. With evolving defense needs to combat emerging threats, the demand is shifting toward advanced timing devices. These devices must deliver robust performance and boast enhanced reliability and security features. Suppliers specializing in timing solutions stand to benefit by tailoring their offerings to meet the stringent demands of these mission-critical applications.

- Adhering to the above synopsis, the government's excess investments towards advancing its defense industry will create new growth opportunities for the studied market. According to SIPRI, in 2023, the government invested around 3.08% in its defense budget.

- The country fosters collaborations between industry, academia, and research institutions to drive innovation and technology development. Collaborative research initiatives and partnerships create opportunities for suppliers of timing devices to participate in cutting-edge research projects, develop new technologies, and commercialize innovative solutions. By leveraging the expertise and resources available through collaborative networks, companies can gain a competitive edge and accelerate developing and adopting advanced timing solutions. Such trends and initiatives are expected to drive the market growth in the projected period.

EMEA Frequency Control And Timing Devices Industry Overview

The EMEA Frequency Control And Timing Devices Market is fragmented with the presence of key players like Murata Manufacturing Co. Ltd, Kyocera Corporation, Rakon Limited, Microchip Technology Inc., and TXC Corporation. Key players in the market are adopting strategies such as acquisitions and partnerships to enhance their product offerings and gain sustainable competitive advantage.

In April 2024, KYOCERA AVX, a manufacturer of advanced electronic components, unveiled a new manufacturing and design center for high-quality, low-noise quartz crystal frequency control products under the name KYOCERA AVX Components Corporation (Erie). The newly established production facility could manufacture over 1.2 million patented and unparalleled low-power OCXO (oven-controlled crystal oscillators). It would produce a range of TCXO (temperature-computed crystal oscillators) and VCXO (voltage-computed crystal oscillators).

In February 2024, the Error Exchange OCXO (MercuryXE2) is a version of Rakon's recently launched Mercury compact IC-OCXO. It improves the system's current synchronization abilities on a network synchronizer evaluation board by incorporating frequency error exchange processing and aging compensation, thereby increasing the holdover performance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 Aftereffects and Macro Economic Trends on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Number of Emerging Applications (such as IoT Devices, Robotics, etc.)

- 5.1.2 Rising Demand from Advanced Automotive Applications

- 5.2 Market Restraint

- 5.2.1 High Cost of Development

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Crystals

- 6.1.2 Oscillators

- 6.1.2.1 Temperature Compensated Crystal Oscillator (TCXO)

- 6.1.2.2 Voltage-controlled Crystal Oscillator (VCXO)

- 6.1.2.3 Oven-controlled Crystal Oscillator (OCXO)

- 6.1.2.4 MEMS Oscillator

- 6.1.2.5 Other Types of Oscillators

- 6.1.3 Resonators

- 6.1.4 Saw Filters

- 6.1.5 Real Time Clocks

- 6.2 By End-user Industry

- 6.2.1 Automotive

- 6.2.2 Computer and Peripherals

- 6.2.3 Communications/Server/Data Storage

- 6.2.4 Consumer Electronics

- 6.2.5 Industrial

- 6.2.6 Defense and Aerospace

- 6.2.7 IoT

- 6.2.8 Other End-user Industries

- 6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 GCC

- 6.3.6 South Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Murata Manufacturing Co. Ltd

- 7.1.2 Kyocera Corporation

- 7.1.3 Rakon Limited

- 7.1.4 Microchip Technology Inc.

- 7.1.5 TXC Corporation

- 7.1.6 Seiko Epson Corporation

- 7.1.7 Daishinku Corporation

- 7.1.8 Hosonic Technology (group) Co. Ltd

- 7.1.9 Nihon Dempa Kogyo Co. Ltd

- 7.1.10 Sitime Corporation

- 7.1.11 Stmicroelectronics NV

- 7.1.12 Texas Instruments Incorporated

- 7.1.13 NXP Semiconductors NV

- 7.1.14 Abracon Llc

- 7.1.15 Jauch Quartz

- 7.1.16 IQD Frequency Products Ltd

- 7.1.17 Euroquartz Ltd

- 7.1.18 Geyer Electronic GmbH

- 7.1.19 ACT

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS