PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549871

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549871

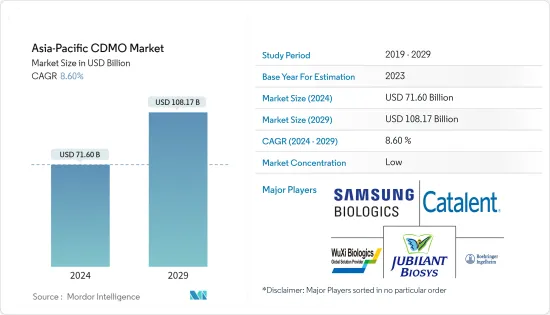

Asia-Pacific CDMO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Asia-Pacific CDMO Market size is estimated at USD 71.60 billion in 2024, and is expected to reach USD 108.17 billion by 2029, growing at a CAGR of 8.60% during the forecast period (2024-2029).

The Asia-Pacific CDMO (contract development and manufacturing organization) market is poised for substantial growth in 2024 and beyond. This growth can be attributed to escalating pharmaceutical demands, increasing emphasis on R&D, and the growing trend of outsourcing drug development and manufacturing.

Key Highlights

- The market is set for substantial growth, driven by the escalating trend of pharmaceutical companies outsourcing drug development and manufacturing. This is largely due to robust government backing and enticing incentives that lure foreign investments.

- Emerging markets, including China, India, and South Korea, are poised to maintain their dominance in the market. The rising incidence of chronic diseases and aging demographics in these nations are expected to drive up the need for pharmaceuticals, subsequently boosting the demand for CDMO services.

- China has over 180 million elderly citizens suffering from chronic diseases; of that, 75% has more than one, according to the National Health Commission (NHC). By 2030, cardiovascular diseases are expected to cost the Chinese government USD 1,044 billion. Similar trends for the high prevalence of diabetes are present in Asia-Pacific, including China, South Korea, and Australia.

- While the United States remains the central hub for pharmaceutical development outsourcing, the APAC region stands out as the favored CDMO growth market. This preference is largely attributed to the region's cost-effective manufacturing compared to North America and Europe. Significant funding allocations and the clustering of pharmaceutical research centers around universities contribute to this trend.

- However, the Asia-Pacific CDMO market is grappling with a severe labor shortage, leading to a significant surge in labor costs. This trend has prompted numerous Western CDMOs to relocate their operations back to the United States and Europe. Moreover, national policies, trade dynamics like Brexit and the US-China conflict, and the repercussions of the pandemic are poised to prompt the reshoring of supply chains in numerous nations.

Asia-Pacific CDMO Market Trends

The Demand For Injectable Dose Formulation is Rising in the Market

- The CDMO market is poised for growth, driven by increasing demand for injectable drugs, notably in cancer research. With a strong emphasis on oncology and other potent medications (including antibody conjugates, steroids, and fast-acting IV fluids), cytotoxics are anticipated to spearhead the growth in the injectable dose formulation segment.

- Injectable drugs are poised to outperform other drug formulations, offering superior returns. This is primarily attributed to their higher ROI, enhanced therapeutic efficacy, and quicker onset of action. The surge in demand for diabetes drugs has led to shortages for many patients reliant on these medications. The increased demand for injectable diabetes drugs in the region significantly boosted the segment's growth.

- According to Sina Med, the value of the human insulin market in China is expected to increase from USD 2.75 billion in 2018 to around USD 4.63 billion in 2030. The increasing prevalence of diabetes is a key driver expected to propel the growth of the injectable antidiabetic drugs market in the coming years.

- Further, the rising demand for cell and gene therapies is propelling the growth of the sterile injectable contract manufacturing sector. These therapies, tailored for genetic and chronic diseases, offer personalized and often curative treatments. Given their nature, manufacturing sterile injectables for these therapies necessitates specialized processes to meet stringent regulatory standards.

- In September 2023, India-based Strides introduced a separate branch of specialty pharma CDMO. The newly established company manufactures a wide array of products, spanning from biologicals to intricate injectables and oral soft-gelatin capsules. Such constants are expected to bolster the segmental growth in the region during the forecast period.

India is Expected to Witness Robust Growth in the Upcoming Years

- The Indian pharmaceutical sector predominantly focuses on producing bulk pharmaceuticals, the foundational ingredients for formulations. While bulk pharmaceuticals constitute roughly 20% of the sector's output, formulations make up the remaining 80%. India's prowess extends to active pharmaceutical ingredients (APIs), with the country manufacturing over 500 APIs and serving as the origin for 60,000 generic brands spanning 60 therapeutic categories.

- The global CDMO market is expanding, propelled by the cost-effective resources found in emerging markets. India is the top choice for CDMOs, boasting over 100 manufacturing facilities approved by the US FDA, with this number rising. The biologics CDMO market in India's pharmaceutical sector is gaining ground, bolstered by the robust presence of key players like Zydus Cadila and LUPIN.

- The pharmaceutical sector in India has become a prime target for foreign investors, ranking among the nation's top ten industries for foreign investment. The Indian government has implemented an investor-friendly Foreign Direct Investment (FDI) policy to further bolster investments in this sector. According to the Department for Promotion of Industry and Internal Trade (India), across the entire healthcare sector, the amount invested in drugs and pharmaceuticals witnessed the highest foreign investment of USD 21.46 billion between April 2020 and March 2023. Such consistent investment in the pharmaceutical sector may propel the market for pharmaceutical contract manufacturing during the forecast period.

- The Indian pharmaceutical sector experienced a surge in growth, propelled by the COVID-19 pandemic. Post-pandemic, there was a notable uptick in demand and production for anti-viral and anti-bacterial drugs within India. Consequently, companies in this sector notched up rising revenues. The increased trade tensions between the US and China underscored the global pharmaceutical supply chain's need for geo-diversification. China's cost structure shifted, making it a pricier outsourcing hub, while India's appeal grew.

Asia-Pacific CDMO Industry Overview

The Asia-Pacific CDMO Market is fragmented because of the presence of major players like Catalent Inc., Jubilant Biosys Ltd, Samsung Biologics, Boehringer Ingelheim Group, and WuXi Biologics. The other players are adopting acquisition and partnership strategies to enter the market and expand their offerings.

- February 2023: Catalent unveiled the completion of the expansion of a facility worth USD 2.2 million to its Clinical Supply in Singapore. The expansion increased the site footprint to 31,000 sq. ft, allowing the installation of 35 new UL freezers. The investment also enabled the facility to support bigger packaging campaigns with additional secondary packaging capacities for ULT products and increased capacity to process biopharmaceutical products and advanced modalities such as mRNA-based vaccines and cell and gene therapies.

- June 2023: FUJIFILM Diosynth Biotechnologies announced its intentions to enhance the commercial office in Tokyo to enhance sales support and customer service for contract development and manufacturing services catering to Biologics and Advanced Therapies, specifically targeting pharmaceutical and biotechnology firms based in Asia.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Porter's Five Forces Analysis for CMO

- 4.2.1.1 Bargaining Power of Suppliers

- 4.2.1.2 Bargaining Power of Buyers

- 4.2.1.3 Threat of New Entrants

- 4.2.1.4 Threat of Substitute Products

- 4.2.1.5 Intensity of Competitive Rivalry

- 4.2.2 Porter's Five Forces Analysis for CRO

- 4.2.2.1 Bargaining Power of Suppliers

- 4.2.2.2 Bargaining Power of Buyers

- 4.2.2.3 Threat of New Entrants

- 4.2.2.4 Threat of Substitute Products

- 4.2.2.5 Intensity of Competitive Rivalry

- 4.2.1 Porter's Five Forces Analysis for CMO

- 4.3 Industry Policies

- 4.4 Industry Value Chain Analysis

- 4.5 Market Dynamics

- 4.5.1 Market Drivers

- 4.5.1.1 Increasing Outsourcing Volume by Big Pharmaceutical Companies

- 4.5.1.2 Increasing Investment in Research and Development

- 4.5.2 Market Restraints

- 4.5.2.1 Increasing Lead Time Owing to Supply Chain Related Constraints in the Region

- 4.5.2.2 Skilled Labour Shortages Across the Region

- 4.5.1 Market Drivers

- 4.6 Qualitative Coverage on the 3D Printing Developments in the OSD Segment

- 4.6.1 Evolution of 3D Printing in Fabrication Processes and the Key Advantages Over Conventional Processes

- 4.6.2 Analysis of Major Drugs Manufactured Using 3D Printing-based Process

- 4.6.3 Analysis of Key Techniques Deployed (SLS & FDM), Along with their Relative Advantages

- 4.6.4 Key Developments on Stakeholders

- 4.7 Technology Snapshot

- 4.7.1 Dosage Formulation Technologies

- 4.7.2 Dosage Forms by Route of Administration

- 4.7.3 Key Considerations for Outsourcing of Pharmaceutical R&D

- 4.7.4 Major Segments in CRO Bio Analytical Testing, Central Laboratory Testing, and cGMP Testing

5 MARKET SEGMENTATION

- 5.1 By Service Type CMO Segment

- 5.1.1 Active Pharmaceutical Ingredient (API) Manufacturing

- 5.1.1.1 Small Molecule

- 5.1.1.2 Large Molecule

- 5.1.1.3 High Potency (HPAPI)

- 5.1.2 Finished Dosage Formulation (FDF) Development and Manufacturing

- 5.1.2.1 Solid Dose Formulation

- 5.1.2.1.1 Tablets

- 5.1.2.1.2 Others

- 5.1.2.2 Liquid Dose Formulation

- 5.1.2.3 Injectable Dose Formulation

- 5.1.3 Secondary Packaging

- 5.1.1 Active Pharmaceutical Ingredient (API) Manufacturing

- 5.2 By Research Phase CRO Segment

- 5.2.1 Pre-clinical

- 5.2.2 Phase I

- 5.2.3 Phase II

- 5.2.4 Phase III

- 5.2.5 Phase IV

- 5.3 By Country

- 5.3.1 China

- 5.3.2 Japan

- 5.3.3 India

- 5.3.4 Australia and New Zealand

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Catalent Inc.

- 6.1.2 Jubilant Biosys Ltd

- 6.1.3 Thermo Fisher Scientific Inc.

- 6.1.4 Samsung Biologics

- 6.1.5 Syngene International Limited

- 6.1.6 Lonza Group

- 6.1.7 WuXi Biologics

- 6.1.8 Boehringer Ingelheim Group

- 6.1.9 FUJIFILM Diosynth Biotechnologies

- 6.1.10 Pfizer CentreOne

- 6.1.11 Recipharm AB

- 6.1.12 Stella Lifecare

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS