PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549859

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549859

Europe Data Center Physical Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

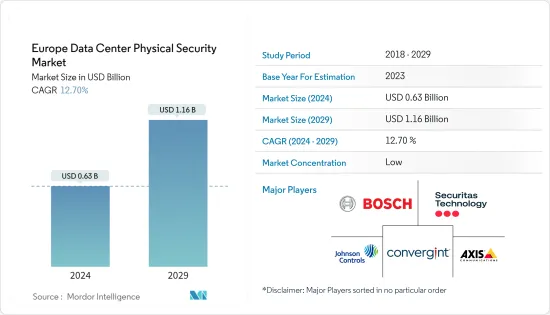

The Europe Data Center Physical Security Market size is estimated at USD 0.63 billion in 2024, and is expected to reach USD 1.16 billion by 2029, growing at a CAGR of 12.70% during the forecast period (2024-2029).

Security measures can be categorized into four, namely perimeter security, computer room controls, facility controls, and cabinet controls. The first layer of data center security discourages, detects, and delays any unauthorized entry of personnel at the perimeter. In case of any infringement in the perimeter monitoring, the second layer of defense denies access. It is an access control system utilizing card swipes or biometrics.

The third layer of physical security further restricts access through various verification methods, including monitoring all restricted areas, deploying entry restrictions such as turnstiles, providing biometric access control devices to verify finger and thumbprints, irises, or vascular patterns, providing VCA, and using radio frequency identification. The first three layers ensure the entry of only authorized people. Further security to restrict admission includes cabinet locking mechanisms. This layer addresses the fear of an 'insider threat,' such as a malicious employee.

The upcoming IT load capacity of the European data center market is expected to reach 18,000 MW by 2029.

The region's construction of raised floor area is expected to increase to 87.6 million sq. ft by 2029.

The region's total number of racks to be installed is expected to reach 4.3 million units by 2029. The United Kingdom is expected to house the maximum number of racks by 2029.

There are close to 210 submarine cable systems connecting Europe, and many are under construction. One such submarine cable that is estimated to start service in 2025 is SeaMeWe-6, which stretches over 19,200 km with a landing point in Marseille, France.

Europe Data Center Physical Security Market Trends

IT and Telecom to Hold Significant Share

- In Europe, players in the telecommunications industry are affected by shrinking revenues and profitability, as well as the effects of regulatory pricing intervention and consolidation. The rapidly increasing 4G penetration and the upcoming 5G wave are adhering telecom vendors to invest in the data center market. Swedish network provider Net4Mobility, a joint venture between local carriers Tele2 and Telenor, announced plans to connect 90% of the nation's population to its 5G network by the end of 2023.

- The impending expansion of hyperscalers for AI-related data centers in the IT and telecom space may create challenges for enterprises, especially in the case of security. Increasing AI-related data centers in countries such as Germany is expected to create a major demand for physical security solutions.

- In the Netherlands, in the telecom industry, the implementation of 5G is projected to impact data traffic positively. By 2026, the country's 3.5G Hz (5G) rollout is anticipated to be complete. By 2030, 60% of the Dutch population will be covered by the 3.5 GHz 5G network, up from 33% in 2023. This trend may greatly encourage the usage of VOD (video on demand). Such instances in the market are expected to create more need for data centers, resulting in rising demand for data center physical security solutions in the coming years.

- The Spanish government allocated EUR 84 million (USD 90.81 million) for the expansion and improvement of the Central Government Private Cloud (SARA Cloud) initiative. The use of the cloud facilitates the development of new business models, enabling companies of all sizes and industries to innovate and gain a competitive edge. The above-mentioned factors indicate a major market demand for physical security solutions.

United Kingdom to Register Significant Growth

- According to the Federation of Small Businesses (FSB), as of 2023, there were 5.51 million small businesses in the United Kingdom, accounting for 99.2% of the total business in the region. SMEs accounted for three-fifths of the employment and around half of the Kingdom's private sector turnover. A growing shift toward hyperscale data centers to efficiently support robust, scalable applications is anticipated to propel the data center security market in the United Kingdom.

- With data center providers increasing their digital infrastructure, the demand for physical security is expected to increase. In October 2021, Equinix Inc., a digital infrastructure company, announced its plans to build a new international business exchange (IBX) data center in Salford, Manchester. Equinix also announced a total investment of USD 165 million and an additional USD 1 billion in digital infrastructure in the United Kingdom.

- Brexit brought uncertainties among cloud providers in terms of storage and retrieval of customer data. European companies that are associated with the UK data center market are migrating workloads to the United Kingdom and other EU countries. In 2020, the increase in demand for cloud services led to the launch of 10 new services by Microsoft, AWS, and others. Such factors are expected to increase the cloud infrastructure, leading to the demand for physical security solutions.

- In December 2023, the UK government launched a new consultation, i.e., 'Protecting and enhancing the security and resilience of UK data infrastructure,' to source views on proposed regulations to improve the security and resilience of data infrastructure, including data centers. This is expected to increase the number of new players in the market regarding DC physical security solutions.

Europe Data Center Physical Security Industry Overview

The European data center physical security market is highly fragmented due to players like Axis Communications AB, ABB Ltd, and Bosch Sicherheitssysteme GmbH, which play a vital role in upscaling the capabilities of enterprises. Market orientation leads to a highly competitive environment. These major players with a prominent market share are focused on expanding their customer base across the region. These companies leverage strategic collaborative initiatives to increase their market share and profitability.

In April 2023, Schneider Electric launched EcoCare for Modular Data Centers services membership. Members of this innovative service plan benefit from specialized expertise to maximize modular data centers' uptime with 24/7 proactive remote monitoring and condition-based maintenance.

In March 2023, Motorola Solutions announced the new Avigilon physical security suite, providing organizations worldwide with scalable, secure, and flexible video security and access control solutions. The Avigilon security suite includes the on-premise Avigilon Unity solutions and cloud-native Avigilon Alta, each with advanced analytics designed to provide an effortless user experience.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased Data Center Activities and Investment by the Hyperscale and Colocation Operators

- 4.2.2 Advancements in Video Surveillance Systems Connected to Cloud Systems

- 4.3 Market Restraints

- 4.3.1 Operational and Return On Investment Concerns

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Solution Type

- 5.1.1 Video Surveillance

- 5.1.2 Access Control Solutions

- 5.1.3 Others (Mantraps, Fences, and Monitoring Solutions)

- 5.2 By Service Type

- 5.2.1 Consulting Services

- 5.2.2 Professional Services

- 5.2.3 Others (System Integration Services)

- 5.3 End User

- 5.3.1 IT and Telecommunication

- 5.3.2 BFSI

- 5.3.3 Government

- 5.3.4 Healthcare

- 5.3.5 Other End Users

- 5.4 Country

- 5.4.1 France

- 5.4.2 United Kingdom

- 5.4.3 Sweden

- 5.4.4 Austria

- 5.4.5 Belgium

- 5.4.6 Germany

- 5.4.7 Ireland

- 5.4.8 Italy

- 5.4.9 Norway

- 5.4.10 Poland

- 5.4.11 Spain

- 5.4.12 Switzerland

- 5.4.13 Netherlands

- 5.4.14 Denmark

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Axis Communications AB

- 6.1.2 Convergint Technologies LLC

- 6.1.3 Securitas Technology

- 6.1.4 Bosch Sicherheitssysteme GmbH

- 6.1.5 Johnson Controls International

- 6.1.6 Honeywell International Inc.

- 6.1.7 Schneider Electric

- 6.1.8 Pelco (Motorola Solutions Inc.)

- 6.1.9 Milestone Systems A/S

- 6.1.10 Cisco Systems Inc.

- 6.1.11 ABB Ltd

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS