PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549850

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549850

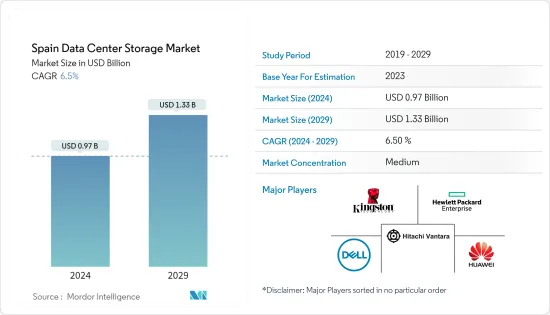

Spain Data Center Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Spain Data Center Storage Market size is estimated at USD 0.97 billion in 2024, and is expected to reach USD 1.33 billion by 2029, growing at a CAGR of 6.5% during the forecast period (2024-2029).

The increasing demand for cloud computing among SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data centers in the country.

Key Highlights

- Under Construction IT Load Capacity: The upcoming IT load capacity of the Spain data center rack market is expected to reach 1400 MW by 2029.

- Under Construction Raised Floor Space: The country's construction of raised floor area is expected to increase to 6 million sq. ft by 2029.

- Planned Racks: The country's total number of racks to be installed is expected to reach 330,000 units by 2029. Madrid will likely house the maximum number of racks by 2029.

- Planned Submarine Cables: There are close to 32 submarine cable systems connecting Spain, and many are under construction.

- An increasing need for data storage has resulted in an upsurge in the number of data centers nationwide. Several factors contribute to the demand for data centers and their growth within the spain, which is reflected by the country's evolving IT landscape, business activities, and technological initiatives. Key drivers that propel the development of data centers in the nation include Digital Transformation, Cloud Computing Adoption, E-commerce & Digital Services, Renewable Energy & Sustainability, and Smart Cities & IoT Initiatives. Hence, such factors are expected to drive market growth during the forecast period.

Spain Data Center Storage Market Trends

IT & Telecommunication Segment holds the major share.

- The increasing use of the cloud by large companies, driven by technologies such as big data and artificial intelligence, is the main driver of the Spanish market. The number of companies in the IT solutions and services industry has grown significantly from 16,648 in 2020 to 18,264 in 2023.

- Increased adoption of cloud-based services has fueled the expansion of retail and wholesale colocation services in Spain, leading to increased demand. This will require more racks in the data center.

- The cloud service market, which is indispensable for digitalization, is growing rapidly. With the rise of the digital economy and increased internet usage in Spain, the need for data storage and processing is increasing.

- The government has allocated EUR 84 million (USD 90.81 million )for the expansion and improvement of the Central Government Private Cloud (SARA Cloud) initiative. The use of the cloud facilitates the development of new business models, enabling companies of all sizes and industries to innovate and gain a competitive edge.

- Additionally, the data center industry heavily depends on the telecommunications sector. The 5G and broadband industries are rapidly building and deploying links across the nation. The nation has developed the Plan for Connectivity and Digital Infrastructures and the Strategy to Promote 5G Technology, which would be endowed with EUR 4,320 million (USD 4,551.1 million) through 2025 to push the adoption of 5G further. Such instances in the market are expected to create more demand for data center Storage in the coming years.

Hybrid Storage is Expected to Hold a Significant Market Share

- The combination of on-premises and cloud storage solutions is called hybrid storage in data centers. This approach leverages the strengths of both environments, offering the flexibility to store and manage data on-site and in the cloud.

- Digital transformation is being applied by Spanish businesses and around the world. In support of a phased and strategic approach towards Digitalisation, the integration of old systems with new cloud-based technologies is facilitated by hybrid data centers.

- Specific data storage and processing requirements may exist in certain sectors of the Spanish economy. The flexibility of the hybrid architecture allows for a wide variety of solutions based on specific sector requirements like finance, healthcare, or manufacturing.

- Furthermore, factors such as internet users, online shopping, would contribute to the increasing generation of data and processing facilities. As users grow more inclined to online shopping with attractive deals offered, this would lead to a rise in digital payment services and traffic on websites, thus increasing data consumption. The number of digital payment users in the country is projected to reach 40.6 million by 2027, up from 32.35 million users in 2022. All these factors would contribute to a significant increase in consumption, boosting the demand for DC cooling infrastructre in the region.

- The key players in the market focus on collabrations and improving the data center storage solutions to meet the market demand. In June 2023, Hitachi Vantara, a prominent infrastructure, data management, and digital solutions subsidiary of Hitachi, Ltd., announced its two new global partnership agreements with Cisco. These agreements will enable Hitachi Vantara to seamlessly integrate Cisco technologies into its storage products and position it as a leading provider of data center infrastructure and hybrid cloud-managed services by bringing it into the Vantara Service Provider and Technology Integrator (STI) Partner programs.

Spain Data Center Storage Industry Overview

The upcoming DC construction projects in the country would increase the demand for Spain data center storage Market in the coming years. The Spain Data Center Storage Market is moderately consolidated with some players in the market, including Dell Inc., Hewlett Packard Enterprise, Huawei Technologies Co. Ltd., Hitachi Vantara LLC, and Kingston Technology Company Inc. These major players, with a prominent market share, focus on expanding their regional customer base.

- May 2023: Nutanix, a prominent provider in cloud computing and hybrid multi-clouds, announced the launch of Nutanix Central, a cloud-based solution that provides a single console for visibility, monitoring, or management across on-premises, hosted, or edge infrastructure. This will extend the universal cloud operating model of the Nutanix Cloud Platform to break down silos and simplify consistently managing apps and data anywhere.

- March 2023: At the World Mobile Congress Barcelona in 2023, it released the industry's prominent entry-level primary and secondary storage portfolio based on a Huawei A-A architecture. This portfolio solution is developed to assist SMEs in building cost-effective data storage systems using the new Huawei OceanStor Dorado 2000 and OceanProtect X3000.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand of Clolud Computing Capabilities Drives the Market Growth

- 4.2.2 Increase in the Demand for Energy-Efficient and Cost-Effective Data Centers

- 4.3 Market Restraints

- 4.3.1 Skilled Workforce Availability and Security Concerns

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 Storage Technology

- 5.1.1 Network Attached Storage (NAS)

- 5.1.2 Storage Area Network (SAN)

- 5.1.3 Direct Attached Storage (DAS)

- 5.1.4 Other Technologies

- 5.2 Storage Type

- 5.2.1 Traditional Storage

- 5.2.2 All-Flash Storage

- 5.2.3 Hybrid Storage

- 5.3 End-User

- 5.3.1 IT & Telecommunication

- 5.3.2 BFSI

- 5.3.3 Government

- 5.3.4 Media & Entertainment

- 5.3.5 Other End-User

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dell Inc.

- 6.1.2 Hewlett Packard Enterprise

- 6.1.3 Huawei Technologies Co. Ltd.

- 6.1.4 Hitachi Vantara LLC

- 6.1.5 Kingston Technology Company Inc.

- 6.1.6 Pure Storage Inc.

- 6.1.7 Infinidat Ltd.

- 6.1.8 Lenovo Group Limited

- 6.1.9 Fujitsu Limited

- 6.1.10 Oracle Corporation

- 6.1.11 KIOXIA Singapore Pte. Ltd.

- 6.1.12 Commvault Systems Inc.

- 6.1.13 NetApp Inc.

- 6.1.14 Nutanix Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS