PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549843

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549843

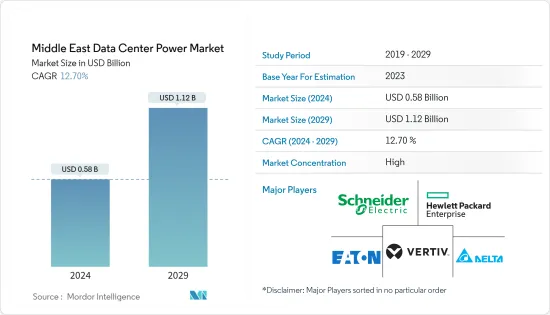

Middle East Data Center Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Middle East Data Center Power Market size is estimated at USD 0.58 billion in 2024, and is expected to reach USD 1.12 billion by 2029, growing at a CAGR of 12.70% during the forecast period (2024-2029).

The exponential growth of data has led to a massive increase in electrical power usage within data centers. In 2022, as per the Energy Institute, the consumption of primary energy in the Middle East amounted to approximately 39.13 exajoules, an increase of around 4.3% in comparison to the previous year. Operators are seeking more energy-efficient technological equipment to ensure optimum operation while minimizing energy consumption. In countries such as the United Arab Emirates, the government has pledged to cut emissions as part of its global commitment to tackle climate change. Overall, the demand for renewable power solutions is expected to increase.

Key Highlights

- The upcoming IT load capacity of the Middle Eastern data center construction market is expected to reach 2,059.5 MW by 2029.

- The region's construction of raised floor area is expected to increase by 9.7 million sq. ft by 2029.

- The region's total number of racks to be installed is expected to reach 496 K units by 2029. Saudi Arabia is expected to house the maximum number of racks by 2029.

- There are close to 26 submarine cable systems connecting the Middle East, and many are under construction. One such submarine cable that is estimated to start service in 2024 is Blue, which stretches over 4,696 km with a landing point in Tel Aviv.

Middle East Data Center Power Market Trends

IT and Telecom to Hold Significant Share

- Telecom providers are primarily responsible for driving content delivery and facilitating mobile and cloud services, which is why telecom data centers require high connectivity. This specific type of data center is connected to other data centers, cloud providers, and telecom operators through outside plant (OSP) cables, with cross-connects extensively deployed to ensure efficient operations.

- While most traditional data centers use alternating current (AC) power distribution systems, telecom data centers run on direct current (DC) power. Adding more battery strings allows DC power systems to easily be built and expanded over time as the load increases. Since telecom data centers manage network resources, such as vRAN and 5G packet core, the increasing load is expected to increase with major 5G deployment.

- Telecom suppliers are encouraged to invest in data center businesses due to the increasing adoption of 4G and the impending 5G wave. According to the Telecommunications Regulatory Authority, in the United Arab Emirates, there were about 18.7 million active mobile phone subscribers as of March 2022. This figure reflected a slight rise from December 2020.

- Saudi Arabia's 5G users achieved the fastest 5G peak download speed globally, outpacing South Korea's performance by 11%, at 862.6 Mbps. Once 5,358 new towers are built, there will be 12,302 5G towers nationwide by the end of the year. This number is anticipated to increase as more spectrum is available for commercial use and more people desire quicker internet services.

- The data center power industry is gaining traction due to investments from cloud service providers such as Google and Oracle. For Saudi Vision 2030, Oracle, in partnership with NEOM Tech & Digital Hold Co., will be the first tenant in the hyperscale data center at NEOM. Oracle Cloud Infrastructure (OCI) would be housed in the data center, providing a high-performing, resilient platform for cloud services. Such factors are expected to lead to major demand for power solutions during the forecast period.

UAE to Register Significant Growth

- The major growth drivers for the UAE data center power market include increasing demand for cloud storage and an increasing amount of data around the United Arab Emirates. At the start of 2022, the internet penetration rate in the United Arab Emirates was 99.0% of the total population. The country ranks sixth in terms of digital banking adoption.

- Australian financial comparison website Finder states that the number of UAE residents using digital banking will increase by 22% by the end of 2027. Digital bank account adoption reached 34% in 2023. The increase in data center construction is expected to augment digital banking.

- The use of DCIM/BMS software reduces power consumption and decreases carbon emissions, resulting in significant savings in data center OPEX and reducing human intrusions to handle critical tasks. Therefore, the usage of DCIM/BMS software is rising in the country.

- Increasing IT load capacity is a major factor affecting the demand for power solutions. Khazna Data Centre announced plans in January 2021 to increase its IT load capacity from 40 MW to 200 MW by 2023. The plan calls for expanding the company's three existing data centers in Abu Dhabi and Dubai. Etisalat and du, two national telcos, are also expanding their data storage and transmission capabilities. du opened two data centers recently, one in Dubai Silicon Oasis and one in Abu Dhabi's Khalifa Industrial Zone.

- The United Arab Emirates is also looking into cleaner energy sources to power data centers to reduce environmental impact and carbon emissions. Moro Hub in the United Arab Emirates signed an agreement with Chinese tech giant Huawei in May 2021 to build a 100 MW, uptime tier 3-certified solar-powered data center in the Mohammed bin Rashid Al Maktoum Solar Park.

- In terms of partnerships, Equinix partnered with various organizations to develop and demonstrate low-environmental-impact fuel cells that provide economic and resilient prime power solutions for data centers. The project will integrate solid-oxide fuel cells (SOFC) with uninterruptible power supply (UPS) technology and lithium-ion batteries to provide resilient and clean primary power for data center deployments and other critical infrastructure.

Middle East Data Center Power Industry Overview

The Middle Eastern data center power market is slightly consolidated among the players and has gained a competitive edge in recent years. A few major players in the market include Delta Power Solutions, Vertiv Group Corp., and Eaton Corporation. These major players with a prominent market share focus on expanding their customer base across the region. These companies leverage strategic collaborative initiatives to increase their market share and profitability.

In March 2023, Vertiv Group Corp. announced that its Vertiv Geist Upgradeable Rack PDUs come with a combination outlet C13/19, simplifying purchasing, inventory management, and deployment. The universal C13/C19 outlet on Vertiv Geist Upgradeable Rack PDUs can easily accommodate new rack configurations, eliminating the need to modify or replace rPDUs as rack densities increase.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Mega Data Centers and Cloud Computing

- 4.2.2 Increasing Demand to Reduce Operational Costs

- 4.3 Market Restraints

- 4.3.1 High Cost of Installation and Maintenance

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 Power Infrastructure

- 5.1.1 Electrical Solution

- 5.1.1.1 UPS Systems

- 5.1.1.2 Generators

- 5.1.1.3 Power Distribution Solutions

- 5.1.1.3.1 PDU

- 5.1.1.3.2 Switchgear

- 5.1.1.3.3 Critical Power Distribution

- 5.1.1.3.4 Transfer Switches

- 5.1.1.3.5 Remote Power Panels

- 5.1.1.3.6 Others

- 5.1.2 Service

- 5.1.1 Electrical Solution

- 5.2 End User

- 5.2.1 IT and Telecommunication

- 5.2.2 BFSI

- 5.2.3 Government

- 5.2.4 Media and Entertainment

- 5.2.5 Other End Users

- 5.3 Country

- 5.3.1 Saudi Arabia

- 5.3.2 United Arab Emirates

- 5.3.3 Israel

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 ABB Ltd

- 6.1.2 Caterpillar Inc.

- 6.1.3 Cummins Inc.

- 6.1.4 Eaton Corporation

- 6.1.5 Legrand Group

- 6.1.6 Rolls-Royce PLC

- 6.1.7 Vertiv Group Corp.

- 6.1.8 Schneider Electric SE

- 6.1.9 Rittal GmbH & Co. KG

- 6.1.10 Fujitsu Limited

- 6.1.11 Cisco Systems Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS