PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549841

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549841

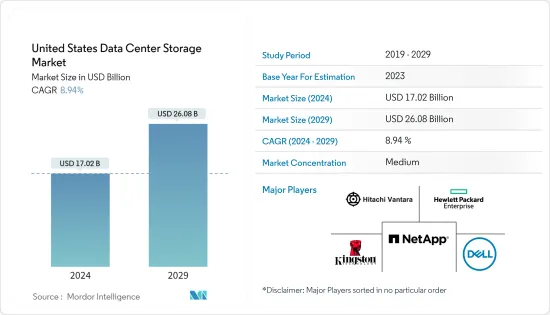

United States Data Center Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The United States Data Center Storage Market size is estimated at USD 17.02 billion in 2024, and is expected to reach USD 26.08 billion by 2029, growing at a CAGR of 8.94% during the forecast period (2024-2029).

The increasing demand for cloud computing among SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data centers in the country.

Key Highlights

- Under Construction IT Load Capacity: The upcoming IT load capacity of the US data center rack market is expected to reach 24,000 MW by 2029.

- Under Construction Raised Floor Space: The country's construction of raised floor area is expected to increase to 80 million sq. ft by 2029.

- Planned Racks: The country's total number of racks to be installed is expected to reach 4,035,000 units by 2029. Northern Virginia is expected to house the maximum number of racks by 2029.

- Planned Submarine Cables: There are more than 90 submarine cable systems connecting the United States, and many are under construction. One such submarine cable that is estimated to start service in 2025 is Gold Data-1, which stretches over 2,333 km with landing points from Naples, United States.

- An increasing need for data storage has resulted in an upsurge in the number of data centers nationwide. Several factors contribute to the demand for data centers and their growth within the United States, which is reflected by the country's evolving IT landscape, business activities, and technological initiatives. Key drivers that propel the development of data centers in the nation include digital transformation, cloud computing adoption, e-commerce and digital services, renewable energy and sustainability, and smart cities and IoT initiatives. Hence, such factors are expected to drive market growth during the forecast period.

United States Data Center Storage Market Trends

IT and Telecommunication Segment Holds the Major Share

- The COVID-19 pandemic impacted the economic effects of early entrants on digital transformation as they began offering digital products and services and using digital processes more than their competitors engaged in digital transformation.

- Among US corporate infrastructure decision-makers, 94% have at least one cloud deployment, with hybrid or multi-cloud solutions more common. Nearly 74% of US infrastructure decision-makers say their organizations are adopting containers as a platform as a service (PaaS) in on-premises or public cloud environments. Clouds are expected to increase significantly.

- US cloud providers include AWS, Microsoft, and Google. Among enterprise infrastructure decision-makers who use at least one type of cloud deployment, 94% use at least one type of cloud deployment, with the majority being hybrid or multi-cloud.

- In the United States, cloud storage is growing due to the growing demand for cost-effective data backup, storage, and backup in every business and the need to manage the data generated by the increasing use of mobile phones.

- With the rise of the digital economy and increased internet usage in the United States, the need for data storage and processing has increased. The proliferation of hybrid cloud service providers has increased demand for colocation services and increased rack utilization.

- The number of IoT devices utilizing network connections from telecommunication providers is likely to generate huge amounts of data. For instance, connected consumer device unit shipments in the United States were projected to reach more than 800 million units by 2023. By 2025, IoT connections in the United States are projected to grow to more than 4 billion. In the United States, the average monthly mobile data speed is projected to reach 534 Mbps in 2029 through 5G service. Such instances in the market are expected to create more need for data centers, resulting in rising demand for data center storage solutions in the coming years.

Hybrid Storage is Expected to Hold a Significant Market Share

- The combination of on-premises and cloud storage solutions is called hybrid storage in data centers. This approach leverages the strengths of both environments, offering the flexibility to store and manage data on-site and in the cloud.

- The United States is a hub of technological innovation, and there is widespread adoption of advanced technologies, such as AI, machine learning, and analytics. Hybrid storage infrastructure is needed for these technologies to be integrated and supported smoothly.

- The ability to adapt and innovate is vital in a competitive business environment. By providing a robust, cost-efficient, and technically advanced storage solution, hybrid storage-type DC facilities improve the competitiveness of businesses in the United States.

- Furthermore, with the advent of 5G and the increasing use of smartphones, we need to ensure adequate speed availability. As a result, the country has adopted cloud computing, increased the number of Internet users, and adopted fiber optic technology. With the introduction of such technologies and the increase in data usage, the use of hybrid storage data centers is increasing in the country.

- In 2023, around 92% of the US population was an internet user, up from approximately 75% in 2012. The United States is one of the world's largest online markets, with approximately 299 million internet users in the country in 2022. Such market improvements propel data centers' growth and contribute to segmental growth.

- The key players in the market focus on improving the data center storage solutions to meet the market demand. In July 2023, Hitachi Vantara, a prominent infrastructure, data management, and digital solutions subsidiary of Hitachi Ltd, announced its collaboration with Microsoft to launch the Hitachi Unified Compute Platform (UCP) for Azure Stack HCI. The streamlined and powerful hybrid cloud solution increases business flexibility and delivers enhanced cloud management across various environments, including data centers, branch offices, and edge computing, to give businesses greater visibility and control over how their data is stored, managed, and used.

United States Data Center Storage Industry Overview

The upcoming DC construction projects in the country are expected to increase the demand in the US data center storage market in the coming years. The US data center storage market is moderately consolidated with some major players, including Dell Inc., Hewlett Packard Enterprise, NetApp Inc., Hitachi Vantara LLC, and Kingston Technology Company Inc. These major players, with a prominent market share, focus on expanding their regional customer base.

- April 2023: Hewlett Packard Enterprise (HPE) announced new file, disaster, block, and backup recovery data services designed to assist customers in eliminating data silos, reduce cost and complexity, and improve performance. The new file storage data services deliver scale-out, enterprise-intensive performance for data workloads, and the expanded block services provide mission-critical, midrange storage economics.

- February 2023: NetApp, a significant, cloud-led, data-centric software company, announced the expansion of NetApp AFF C-Series, a new product line of capacity flash storage that delivers lower-cost all-flash storage, and NetApp AFF A150, a new entry-level storage system in the AFF A-Series line of all-flash systems.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Cloud Computing Capabilities Drives Market Growth

- 4.2.2 Adoption of Green Practices in Data Centers Drives Market Growth

- 4.3 Market Restraints

- 4.3.1 High Maintenance and Replacement Cost

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Storage Technology

- 5.1.1 Network Attached Storage (NAS)

- 5.1.2 Storage Area Network (SAN)

- 5.1.3 Direct Attached Storage (DAS)

- 5.1.4 Other Technologies

- 5.2 By Storage Type

- 5.2.1 Traditional Storage

- 5.2.2 All-Flash Storage

- 5.2.3 Hybrid Storage

- 5.3 By End User

- 5.3.1 IT and Telecommunication

- 5.3.2 BFSI

- 5.3.3 Government

- 5.3.4 Media and Entertainment

- 5.3.5 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dell Inc.

- 6.1.2 Hewlett Packard Enterprise

- 6.1.3 NetApp Inc.

- 6.1.4 Hitachi Vantara LLC

- 6.1.5 Kingston Technology Company Inc.

- 6.1.6 Pure Storage Inc.

- 6.1.7 Infinidat Ltd

- 6.1.8 Lenovo Group Limited

- 6.1.9 Fujitsu Limited

- 6.1.10 Nutanix Inc.

- 6.1.11 KIOXIA Singapore Pte. Ltd

- 6.1.12 Commvault Systems Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS