PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549808

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549808

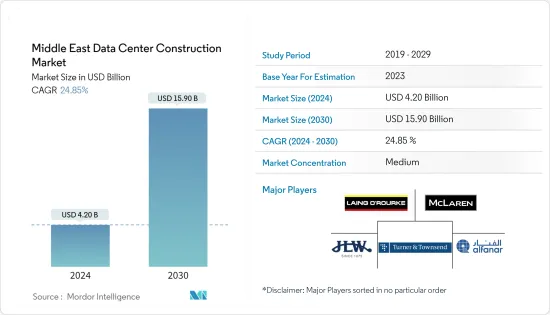

Middle East Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Middle East Data Center Construction Market size is estimated at USD 4.20 billion in 2024, and is expected to reach USD 15.90 billion by 2030, growing at a CAGR of 24.85% during the forecast period (2024-2030).

In the coming years, the Middle East region is expected to increase its investment in the data center market. Several factors are facilitating the expansion of data centers in the area. The smart city ambitions of the governments in the region are driving a shift in how modern communities are built. Cities of the future, supported by digital technologies, are expected to generate massive amounts of data. It is critical to optimize data capture, storage, and processing.

Key Highlights

- The upcoming IT load capacity in the region is expected to reach 3,530 MW by 2030, which is projected to positively impact the demand for data center racks during the forecast period.

- The region's construction of raised floor area is expected to increase by 12.6 million sq. ft by 2030.

- The region's total number of racks to be installed is expected to reach 380k units by 2029. Saudi Arabia is expected to house the maximum number of racks.

- There are close to 29 submarine cable systems connecting the Middle East, and many are under construction. One such submarine cable that is estimated to start service in 2025 is India Europe Xpress (IEX), which stretches over 9,775 kilometers with a landing point in NEOM, Saudi Arabia, Yanbu, Saudi Arabia, and Salalah, Oman.

Middle East Data Center Construction Market Trends

Tier 3 Expected to Hold the Major Share in the Region

- The tier 3 segment of the data center market in the Middle East is expected to record a CAGR of 21.48% during the forecast period (2024-2030) due to the growing user base of streaming services, online gaming, smart home automation services, and other factors.

- There are around 90 tier 3 data center facilities in the Middle East. These facilities are mainly located in Dubai, Abu Dhabi, Jeddah, Fursan, Riyadh, Herzliya, Rosh HaAyin, Tel Aviv, Bnei Zion, Doha, Tehran, Amman, Aqaba, Al-Askar, Hamala, Muscat, and Bawshar.

- In 2023, the tier 3 segment dominated the market, claiming a substantial 75% share, boasting an IT load capacity exceeding 600 MW. Geographically, the United Arab Emirates led the pack with a 36% share, trailed by Saudi Arabia at 28.6% and Israel at 25.4%, with other countries following suit.

- In terms of the number of facilities, medium data centers in the tier 3 segment in the Middle East currently have a market share of 44.7%, followed by market shares of 34%, 16%, and 3.2% for large, small, and mega data centers, respectively.

- Such instances in the Middle East are expected to drive the demand for tier 3-certified facilities. This surge in demand, specifically from the tier 3 segment, is anticipated to bolster the need for data center construction services in the years ahead.

Saudi Arabia Expected to Hold Major Share in the Region

- The Saudi Arabian data center market held the major share in 2023, with an IT load capacity of 258 MW. Saudi Arabia's data center infrastructure development has surged, propelled by the government's 'Vision 2030' initiative, designed to broaden the nation's economic base.

- Positioned at the crossroads of Asia, Africa, and Europe, Saudi Arabia leveraged its strategic location to bolster its data center market. The Red Sea and Arabian Gulf witness a significant influx of subsea cables, further enhancing the region's connectivity. The data center industry, emerging in the early 2000s, primarily catered to the telecoms and banking & finance sectors. Over the years, a surge in both local and international investments has catalyzed the sector's growth, prompting the development of tier-3 and tier-4 certified data centers.

- The rising adoption of the Internet of Things (IoT) for higher production efficiency, better customer experience, improved communication services, and Industry 4.0, in line with the country's Vision 2030, is driving the ICT market's growth. The joint venture specializing in IoT by the vendors in the country is further creating demand for IoT solutions and infrastructure. In March 2022, Saudi Telecom Company (STC) formed a USD 131 million partnership with the Public Investment Fund (PIF) to establish a new joint venture (JV) specializing in IoT to expand its 5G and NarrowBand-IoT connection infrastructure.

- The ongoing smart city projects, including NEOM, Red Sea, Qiddiya, Waad Alshamal, and SPARK, and initiatives to develop the most connected and digitized nation by 2030 are the factors further fueling the adoption of IoT technology. This growing adoption of IoT is expected to provide opportunities for the ICT vendors to develop and cater IoT solutions for applications such as predictive maintenance, asset tracking, fleet management, and warehouse optimization.

- In August 2023, Saudi Arabia announced that it would host the Seamless Saudi Arabia 2023 Conference, steered by the Saudi Central Bank. The conference's theme was "The Future of Payments, Fintech and Banking across Saudi Arabia," and the meeting cemented the apex bank's efforts to achieve the Saudi Vision 2030 objective of digital transformation within the financial sector. The surge in data storage demand is poised to elevate the need for data centers in the region, thereby bolstering the prospects of data center construction firms in the coming years.

Middle East Data Center Construction Industry Overview

The Middle East data center construction market is fairly fragmented with the presence of significant players, such as Laing O'Rourke, McLaren Construction Group PLC, Turner & Townsend, James L Williams Middle East, and Alfanar Group.

In October 2023, CtrlS Datacenters, an Indian data center company, announced its ambitious investment plan of USD 2 billion. This investment, set to unfold over the next six years, is aimed at bolstering its presence across Asia and the Middle East. The company's strategy includes a significant expansion, with a target of adding 350 MW of AI and cloud-ready hyperscale data center capacity. This expansion will be implemented both in new facilities and as augmentations to its existing ones, which currently boast a capacity of 234 MW.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 The Growth of Internet of Things (IoT) Devices, Cloud adoption, and Artificial Intelligence (AI) Drives the Demand for Data Center Construction

- 4.2.1.2 The Government Push to Implement Digital Programs Driving the Demand for Data Centers

- 4.2.2 Market Restraints

- 4.2.2.1 High Power Consumption and Emission Contribution of Data Centers

- 4.2.1 Market Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Key Middle East Data Center Construction Statistics

- 4.4.1 Number of Data Centers in the Middle East, 2022 and 2023

- 4.4.2 Data Center Under Construction in the Middle East, in MW, 2024 - 2029

- 4.4.3 Average CAPEX and OPEX for the Middle East Data Center Construction

- 4.4.4 Data Center Power Capacity Absorption in MW, Selected Cities, Middle East, 2022 and 2023

- 4.4.5 The Top CAPEX Spenders on Data Center Infrastructure in the Middle East

5 MARKET SEGMENTATION

- 5.1 Market Segmentation - By Infrastructure

- 5.1.1 Market Segmentation - By Electrical Infrastructure

- 5.1.1.1 Power Distribution Solution

- 5.1.1.1.1 PDU - Basic & Smart - Metered & Switched Solutions

- 5.1.1.1.2 Transfer Switches

- 5.1.1.1.2.1 Static

- 5.1.1.1.2.2 Automatic (ATS)

- 5.1.1.1.3 Switchgear

- 5.1.1.1.3.1 Low-Voltage

- 5.1.1.1.3.2 Medium-Voltage

- 5.1.1.1.4 Power Panels and Components

- 5.1.1.1.5 Other Power Distribution Solutions

- 5.1.1.2 Power Backup Solutions

- 5.1.1.2.1 UPS

- 5.1.1.2.2 Generators

- 5.1.1.3 Service - Design & Consulting, Integration, Support & Maintenance

- 5.1.2 Market Segmentation - By Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.2.1.1 Immersion Cooling

- 5.1.2.1.2 Direct-To-Chip Cooling

- 5.1.2.1.3 Rear Door Heat Exchanger

- 5.1.2.1.4 In-Row and In-Rack Cooling

- 5.1.2.2 Racks

- 5.1.2.3 Other Mechanical Infrastructure

- 5.1.3 General Construction

- 5.1.1 Market Segmentation - By Electrical Infrastructure

- 5.2 Market Segmentation - By Tier Type

- 5.2.1 Tier 1 and 2

- 5.2.2 Tier 3

- 5.2.3 Tier 4

- 5.3 Market Segmentation - By End User

- 5.3.1 Banking, Financial Services, and Insurance

- 5.3.2 IT and Telecommunications

- 5.3.3 Government and Defense

- 5.3.4 Healthcare

- 5.3.5 Other End Users

- 5.4 Market Segmentation - By Country

- 5.4.1 United Arab Emirates

- 5.4.2 Saudi Arabia

- 5.4.3 Israel

- 5.4.4 Qatar

- 5.4.5 Oman

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Laing O Rourke

- 6.1.2 McLaren Construction Group PLC

- 6.1.3 Turner & Townsend

- 6.1.4 James L Williams Middle East

- 6.1.5 Alfanar Group

- 6.1.6 Saudi Technical Contracting Co. (Saudi Technical Limited)

- 6.1.7 SALFO SA

- 6.1.8 ICS ARABIA

- 6.1.9 OCS Infortech LLC

- 6.1.10 Absal Paul Contracting

7 INVESTMENTS ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 ABOUT US

- 9.1 Industries Covered

- 9.2 Illustrative List of Clients in the Industry

- 9.3 Our Customized Research Capabilities