PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549806

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549806

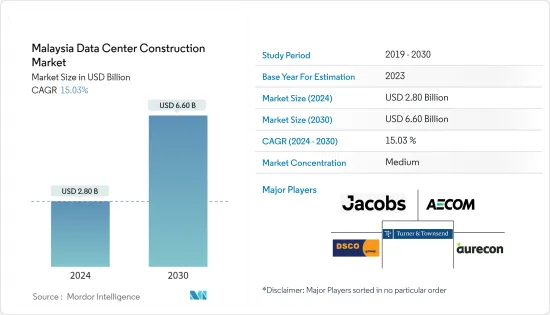

Malaysia Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2030)

The Malaysia Data Center Construction Market size is estimated at USD 2.80 billion in 2024, and is expected to reach USD 6.60 billion by 2030, growing at a CAGR of 15.03% during the forecast period (2024-2030).

Factors such as the rising demand for cloud computing among SMEs, bolstered by government regulations emphasizing local data security and amplified investments by domestic players, are pivotal in propelling the demand for data centers in the Malaysian market.

Key Highlights

- Under Construction IT Load Capacity: The upcoming IT load capacity of the Malaysian data center construction market is expected to reach 1,460 MW by 2030.

- Under Construction Raised Floor Space: The country's construction of raised floor area is expected to increase to 5.2 million sq. ft by 2030.

- Planned Racks: The country's total number of racks to be installed is expected to reach 263,359 units by 2030. Cyberjaya-Kuala Lumpur is expected to house the maximum number of racks by 2030.

- Planned Submarine Cables: There are close to 23 submarine cable systems connecting Malaysia, and many are under construction. One such submarine cable that is estimated to start service in 2025 is SeaMeWe-6, which stretches over 19,200 km with landing points from Morib, Malaysia.

Malaysia Data Center Construction Market Trends

IT and Telecom Segment Expected to Gain a Significant Market Share

- Malaysia's telecom industry is currently navigating an extended negotiation phase between the government and key local operators. In a recent agreement, major carriers, including CelcomDigi, Maxis, U Mobile, Telekom Malaysia, and YTL Power International, committed to purchasing a 14% stake in DNB, each investing approximately USD 50 million.

- The development of digital infrastructure, such as data centers, is central to enabling 5G applications. Owing to this, various investors are signing an agreement for the 5G launch. For instance, in June 2024, Malaysian operators implementing the dual-network 5G model announced that they were poised to finalize an agreement to acquire stakes in the state-operated 5G network, Digital Nasional Berhad (DNB).

- Further, the government announced its plans for a second 5G network, emphasizing its focus on implementing 5G technology across various verticals.

- Moreover, by April 2024, DNB's 5G network covered 81.5% of populated areas, with an adoption rate of 39.2%. The nation boasted a cumulative 13.2 million 5G subscriptions. These subscriptions were divided into 12.7 million for individual users and 422,609 for enterprises. The growing subscriptions are expected to increase dependency on data centers.

- In terms of IT, Malaysia secured the eighth spot in the Asia-Pacific market, boasting a CRI score of 68.5. Specifically, in cloud regulation, Malaysia notched a score of 24.9, ranking it 8th in the regional market. Leading provider Amazon Web Services (AWS) recently inked a fresh Cloud Framework Agreement (CFA) with the Malaysian government. This collaboration, alongside local IT provider Radmik Solutions Sdn Bhd, aims to expedite cloud adoption within the public sector. The initiative targets cost savings, enhanced digital skills, and a push for innovation across government agencies. Such instances in the market are expected to create more opportunities for data center construction players in the coming years.

Tier-III Segment Expected to Hold a Major Share in the Malaysian Market

- Tier-III data centers are majorly popular in Malaysia, with their capacity projected to reach 575 MW in 2024. The segment is estimated to reach an IT load capacity of 1,186 MW by 2029 while recording a CAGR of 12.8%.

- In 2023, there were around 45 data centers in Malaysia with tier-III certification and a cumulative IT load capacity of around 432 MW. Reliability and affordability are the major factors driving the country's demand for tier-III data centers.

- Cyberjaya hosts the maximum number of tier-III data centers in the country, with a share of 70.6%, followed by Kuala Lumpur, Johor Bahru, and George Town. In 2023, VADS BERHAD (TM One) had 10 data centers with tier-III certification in Malaysia, followed by Open DC Sdn Bhd and NTT Ltd, with four data center facilities each.

- More than 10 data center facilities are currently under construction in Malaysia and are being built in accordance with tier-III standards. Major players involved in tier-III DC construction include Bridge Data Center (Chindata Group), Basis Bay, YTL Data Center Holdings Pte Ltd (YTL Power International Berhad), Regal Orion Sdn Bhd, and NTT Ltd. The constructions are projected to be more concentrated in Cyberjaya-Kuala Lumpur, Johor Bahru, and George Town.

- In July 2024, Princeton Digital Group (PDG), an APAC data center company, completed the initial phase of its Johor campus in Malaysia, boasting an IT load capacity of 52 MW. Such developments are poised to fuel market growth through the forecast period.

Malaysia Data Center Construction Industry Overview

The Malaysian data center construction market is semi-consolidated, with a few major players, such as Aurecon Group Pty Ltd, AECOM, DSCO Group Pte Ltd, Turner & Townsend, and Jacobs Engineering Group.

- In April 2024, Asia-Pacific Strategic Investments Limited (APS), a Singaporean real estate firm, acquired a data center company with intentions to expand its operations into Malaysia. APS, known for its expertise in constructing hospitality establishments and retirement communities, marked its inaugural foray into the data center industry with this acquisition.

- In July 2023, Singtel announced plans to develop a data center in Johor, Malaysia, during discussions with the company on a state visit by the head of the Singaporean government. This is expected to create opportunities for the vendors in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 The Rapid Adoption of Cloud Computing by Enterprise and Government Drives Demand in the Market

- 4.2.1.2 Government Initiatives to Modernize in the Digital Era Fueling Heightened Demand for Data Centers Nationwide

- 4.2.2 Market Restraints

- 4.2.2.1 High Power Consumption can Deter Investments

- 4.2.1 Market Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Key Malaysia Data Center Construction Statistics

- 4.4.1 Number of Data Centers In Malaysia, 2022 and 2023

- 4.4.2 Data Centers Under Construction in Malaysia, in MW, 2024 - 2029

- 4.4.3 Average Capex and Opex for the Malaysian Data Center Construction Market

- 4.4.4 Data Center Power Capacity Absorption in MW, Selected Cities, Malaysia, 2022 and 2023

- 4.4.5 Top Capex Spenders on Data Center Infrastructure in Malaysia

5 MARKET SEGMENTATION

- 5.1 Market Segmentation - By Infrastructure

- 5.1.1 Market Segmentation - By Electrical Infrastructure

- 5.1.1.1 Power Distribution Solution

- 5.1.1.1.1 PDU - Basic & Smart - Metered & Switched Solutions

- 5.1.1.1.2 Transfer Switches

- 5.1.1.1.2.1 Static

- 5.1.1.1.2.2 Automatic (ATS)

- 5.1.1.1.3 Switchgear

- 5.1.1.1.3.1 Low-voltage

- 5.1.1.1.3.2 Medium-voltage

- 5.1.1.1.4 Power Panels and Components

- 5.1.1.1.5 Other Power Distribution Solutions

- 5.1.1.2 Power Back Up Solutions

- 5.1.1.2.1 UPS

- 5.1.1.2.2 Generators

- 5.1.1.3 Service - Design & Consulting, Integration, Support & Maintenance

- 5.1.2 Market Segmentation - By Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.2.1.1 Immersion Cooling

- 5.1.2.1.2 Direct-to-Chip Cooling

- 5.1.2.1.3 Rear Door Heat Exchanger

- 5.1.2.1.4 In-row and In-rack Cooling

- 5.1.2.2 Racks

- 5.1.2.3 Other Mechanical Infrastructure

- 5.1.3 General Construction

- 5.1.1 Market Segmentation - By Electrical Infrastructure

- 5.2 Market Segmentation - By Tier Type

- 5.2.1 Tier-I and-II

- 5.2.2 Tier-III

- 5.2.3 Tier-IV

- 5.3 Market Segmentation - By End User

- 5.3.1 Banking, Financial Services, and Insurance

- 5.3.2 IT and Telecommunications

- 5.3.3 Government and Defense

- 5.3.4 Healthcare

- 5.3.5 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Aurecon Group Pty Ltd

- 6.1.2 AECOM

- 6.1.3 DSCO Group Pte Ltd

- 6.1.4 Turner & Townsend

- 6.1.5 Jacobs Engineering Group

- 6.1.6 Gaw Capital Partners

- 6.1.7 JLand Group (JLG)

- 6.1.8 Cyclect Group

- 6.1.9 Basis Bay

- 6.1.10 Mah Sing Group Bhd

7 INVESTMENTS ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 ABOUT US

- 9.1 Industries Covered

- 9.2 Illustrative List of Clients in the Industry

- 9.3 Our Customized Research Capabilities