Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1686666

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1686666

Automated Material Handling (AMH) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 249 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

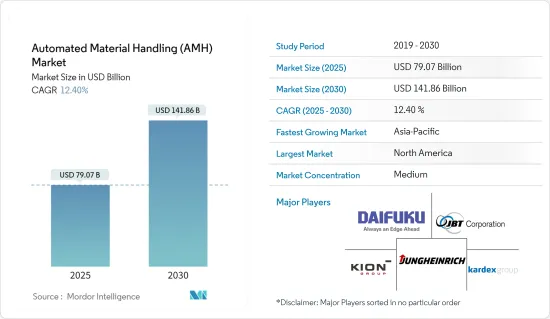

The Automated Material Handling Market size is estimated at USD 79.07 billion in 2025, and is expected to reach USD 141.86 billion by 2030, at a CAGR of 12.4% during the forecast period (2025-2030).

Key Highlights

- Technological advancements, rising labor costs and safety concerns, improved efficiency in manufacturing and warehouse operations, a significant recovery in global manufacturing, increasing demand for automation in industries, growing need for robots in manufacturing units and warehousing facilities, and the growth of emerging markets are key factors driving the automated material handling market. Additionally, the market will benefit from the expanding digitization of supply chain operations, further supported by increasing order customization and personalization during the forecast period.

- Automated Material Handling (AMH) systems streamline the movement of materials across various settings, including manufacturing facilities, warehouses, retail outlets, airports, and logistics centers. These systems facilitate the seamless transfer of materials, whether within the same area, across departments, or even between distinct buildings. AMH systems rely on routes designated by the manufacturing execution system (MES). These systems employ various technologies, including optical character recognition (OCR), barcodes, RFID, ultra-wideband indoor tracking, and near-field communication.

- Over the past seven decades, material handling has undergone significant transformations, reshaping the industry's landscape. Machines and robots have largely supplanted manual labor, catalyzing growth across sectors. Notably, the automotive industry stands out, boasting a remarkable tenfold expansion. Canada's advancements in Industry 4.0 and cutting-edge manufacturing are revolutionizing product design, delivery, and maintenance, even in diverse climates. From robotics and automation to additive manufacturing (3D printing), these technologies find broad utility in sectors spanning e-commerce, automotive, agriculture, and pharmaceuticals. Canadian innovators are spearheading the creation of sophisticated, high-value products, not only for domestic markets but also for a fiercely competitive global arena. Their initiatives not only elevate local practices but also set the stage for collaborative ventures that will define the trajectory of advanced automation technologies.

- While the first AGV debuted in 1953, widespread adoption across production and warehousing firms has been hindered by various factors, with cost being a primary concern. A typical guided vehicle is priced between USD 60,000 and 100,000, but systems with advanced features like navigation aids and sensors can be considerably pricier. These high upfront costs, coupled with maintenance challenges, are dampening the market's growth. Leading firms are striving to control costs without compromising on innovation or R&D investments.

- The COVID-19 pandemic has significantly impacted the adoption of automation across sectors, reshaping operational norms and introducing challenges such as social distancing and contactless operations. Organizations faced surging demands and reduced workforces, prompting the implementation of enhanced safety protocols. Since 2020, the outbreak affected the US workers, compelling companies to adopt new safety measures swiftly. While some industries, like food production, experienced shutdowns due to the virus's severity, many others adapted by incorporating stringent health measures to sustain operations.

Automated Material Handling (AMH) Market Trends

Industry 4.0 Investments Significantly Drive the Market's Growth

- The market is driven by the developments occurring due to countries adopting Industry 4.0 and IOT technologies. Through the use of robotics, industry 4.0 is revolutionizing how material handling is done. In warehouses and distribution facilities, robotics is becoming more and more prevalent. For instance, the International Federation of Robotics reported that US manufacturers heavily invested in automation, leading to a 12% increase in industrial robot installations, totaling 44,303 units in 2023. In addition to picking and packaging orders, loading and unloading trucks, and even cleaning the warehouse floor, they can also be employed for these activities. Workplace accuracy and productivity can both be enhanced by robotics. Robots can also enable company save money by lowering the quantity of necessary manual work.

- For instance, as warehouses are huge, associates must walk considerable distances to locate SKUs and deliver orders to the packing and shipping regions. Every year, an average warehouse wastes 6.9 weeks on unnecessary walking and other movements, equating to 265 million hours of work at the cost of USD 4.3 billion. During each stage of the selection process, collaborative robots also minimize the need for extended walks between functional areas. The rise in material handling equipment orders will significantly drive the studied market.

- Moreover, robotics, automation, and technologies like additive manufacturing (3D printing) have a wide range of applications in Canadian industries such as e-commerce, automotive, agriculture, and pharmaceuticals. Canadian innovators are producing a comprehensive range of technologically complex, increased-value products for domestic and competitive global markets, sharing enhanced practices and laying the groundwork for collaborations that shape the future of advanced automation technologies.

- Germany is also focused on the 2030 vision for Industry 4.0 in three strategic fields of action: autonomy, interoperability, and sustainability. In this 2030 vision, the stakeholders of the platform Industry 4.0 present a holistic approach to shaping the digital ecosystem. The goal is to create a framework for a future data economy that is by the demands of a social market economy, emphasizing open ecosystems, diversity, and supporting competition between all market stakeholders based on the specific situation and established strengths of the German industry base for the automation market.

- Furthermore, the government's strong support in the acquisition program has enabled China to move toward Industry 4.0. For instance, Siasun, a China-based industrial robot maker, is affiliated with the Chinese Academy of Sciences, which is further linked to the government. The country's adoption of industrial control systems by various companies is a notable trend. The advanced systems allow ease of production in factories. This also points to the gradual shift of companies from depending on manual labor to advanced technology-based systems that will enable the facility's automation.

- A significant trend impacting the market studied is the focus on smart manufacturing practices. According to the data from IBEF, the Government of India set an ambitious target of increasing manufacturing output contribution to 25% of the gross domestic product (GDP) by 2025 from 16%. The Smart Advanced Manufacturing and Rapid Transformation Hub (SAMARTH) Udyog Bharat 4.0 initiative aims to enhance awareness about Industry 4.0 within the Indian manufacturing industry and enable stakeholders to address challenges related to automation material handling.

Asia-Pacific is Expected to be the Fastest Growing Market

- China has been a prominent contributor to the growth of the Asia-Pacific AMH market. The increasing demand for AMH products across industries, such as manufacturing, automotive, and e-commerce, boosts the market's growth. China has a vast population and pursues an industrial policy. Measured on the PPP basis, the country became the largest global economy and the largest global exporter and trader during the current decade. The country is currently transitioning from a manufacturing and construction-led economy to a consumer-led economy.

- According to China's National Bureau of Statistics, total retail sales in China's consumer products market were around CNY 41,860.5 billion (USD 5786.31 billion) in 2023. The number of Chinese online buyers has risen rapidly from under 34 million in 2006 to over 915 million in 2023, enabling China's e-commerce business to proliferate. Hence, with growing e-commerce, the demand for material-handling equipment will likely rise in the forecasted years.

- Japan is predominantly a manufacturing nation. Its manufacturing industry contributes close to 20% to the nominal GDP, whereas it is close to 10% for other developed countries. According to the IMF, the country's manufacturing sector has achieved significant industrial productivity gains over the services sector, owing to the increased adoption of ICT. The automotive and electronics sectors are the most productive manufacturing sectors in the country.

- The government's heightened infrastructure investments, bolstered by industry contributions and the 'Make in India' campaign, are set to propel the demand for automated material handling (AMH) systems. Given that the manufacturing sector accounts for 17% of India's GDP and employs over 27.3 million individuals, its significance in the nation's economic landscape is undeniable. With a vision to derive 25% of the economy's output from manufacturing by 2025, the Indian government is rolling out various initiatives and policies. Consequently, manufacturers are gearing up to embrace Industry 4.0 and other digital innovations to meet this ambitious goal.

- South Korea adopted the 4th Industrial Revolution. In Korea, smart factories will be one of the most important fields. Both the private and public sectors in Korea have committed to ramping up the number of domestic smart factories. Their target is ambitious: they aim to have 30,000 such cutting-edge factories equipped with the latest digital and analytical technologies up and running across the nation by 2023. Furthermore, in a bid to counteract Korea's shrinking working-age population, there are plans to establish 20 smart industrial zones by 2030. As part of this initiative, the goal is to set up 2,000 new AI-powered smart factories by 2030, aligning with the rapid pace of digitalization and automation characteristic of the fourth industrial revolution.

Automated Material Handling (AMH) Industry Overview

The automated material handling (AMH) market is characterized by semi-consolidation and high competitiveness. Key players in the market primarily rely on strategies like product launches, significant investments in R&D, and forming partnerships or making acquisitions to navigate the fierce competition.

- In May 2024, KION North America (KION NA), a prominent manufacturer of Linde Material Handling equipment, and Fox Robotics entered into a strategic non-exclusive partnership. As part of this collaboration, KION NA is expected to manufacture and assemble FoxBot autonomous trailer loader/unloaders (ATLs) at its state-of-the-art facilities in Summerville, South Carolina.

- In November 2023, Toyota Material Handling (TMH), a pioneer in material handling, unveiled three cutting-edge electric forklift models. These additions bolster TMH's already extensive range of material handling solutions. The trio includes a Side-Entry End Rider, a Center Rider Stacker, and an Industrial Tow Tractor. These models promise heightened efficiency, versatility, and top-tier performance, all while emphasizing operator comfort.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 53959

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitute Products

- 4.4 Impact of the COVID-19 Pandemic on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Incremental Technological Advancements aiding the Market's Growth

- 5.1.2 Industry 4.0 Investments driving the Demand for Automation and Material Handling

- 5.1.3 Rapid Growth of the E-commerce Sector

- 5.2 Market Challenges

- 5.2.1 High Initial Equipment Costs

- 5.2.2 Unavailability for Skilled Workforce

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Hardware

- 6.1.2 Software

- 6.1.3 Services

- 6.2 By Equipment Type

- 6.2.1 Mobile Robots

- 6.2.1.1 Automated Guided Vehicle (AGV)

- 6.2.1.2 Autonomous Mobile Robot (AMR)

- 6.2.2 Automated Storage and Retrieval System

- 6.2.2.1 Fixed Aisle

- 6.2.2.2 Carousel

- 6.2.2.3 Vertical Lift Module

- 6.2.3 Automated Conveyor

- 6.2.3.1 Belt

- 6.2.3.2 Roller

- 6.2.3.3 Pallet

- 6.2.3.4 Overhead

- 6.2.4 Palletizer

- 6.2.4.1 Conventional

- 6.2.4.2 Robotic

- 6.2.5 Sortation System

- 6.2.1 Mobile Robots

- 6.3 By End User

- 6.3.1 Airport

- 6.3.2 Automotive

- 6.3.3 Food And Beverages

- 6.3.4 Retail/Warehousing/Distribution Centers/Logistic Centers

- 6.3.5 General Manufacturing

- 6.3.6 Pharmaceuticals

- 6.3.7 Post and Parcel

- 6.3.8 Other End Users

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 France

- 6.4.2.3 Italy

- 6.4.2.4 Spain

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.5.1 Brazil

- 6.4.5.2 Mexico

- 6.4.6 Middle East and Africa

- 6.4.6.1 United Arab Emirates

- 6.4.6.2 Saudi Arabia

- 6.4.6.3 South Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Daifuku Co. Ltd

- 7.1.2 Kardex Group

- 7.1.3 KION Group AG

- 7.1.4 JBT Corporation

- 7.1.5 Jungheinrich AG

- 7.1.6 TGW Logistics Group GmbH

- 7.1.7 SSI Schaefer AG

- 7.1.8 KNAPP AG

- 7.1.9 Mecalux SA

- 7.1.10 System Logistics SpA

- 7.1.11 Viastore Systems GmbH

- 7.1.12 BEUMER Group GmbH & Co. KG

- 7.1.13 Interroll Holding AG

- 7.1.14 WITRON Logistik

- 7.1.15 Siemens AG

- 7.1.16 KUKA AG

- 7.1.17 Honeywell Intelligrated Inc. (Honeywell International Inc.)

- 7.1.18 Murata Machinery Ltd

- 7.1.19 Toyota Industries Corporation

- 7.1.20 Visionnav Robotics

- 7.1.21 Dearborn Mid-West Company

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.