PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549581

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1549581

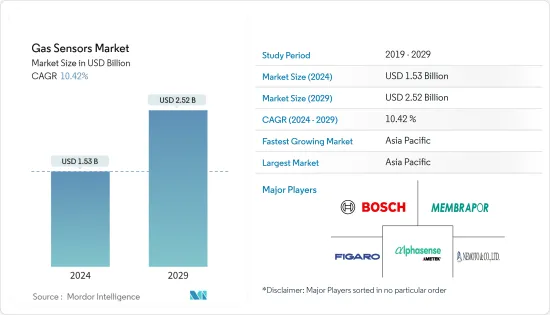

Gas Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Gas Sensors Market size is estimated at USD 1.53 billion in 2024, and is expected to reach USD 2.52 billion by 2029, growing at a CAGR of 10.42% during the forecast period (2024-2029).

Key Highlights

- In smart cities, gas sensors find applications in environmental monitoring, including air quality checks at weather stations, public areas, and within building automation systems. This widespread adoption is expected to drive the market's growth through the forecast period.

- Additionally, heating, ventilation, and air conditioning (HVAC) systems are integral to buildings, monitoring environments and regulating gas concentrations. This dual functionality has spurred significant demand, further fueling market growth.

- Gas detection is paramount in the global oil and gas sector. This industry's offshore drilling and exploration activities produce a spectrum of hazardous, flammable, and toxic gases. While some gases are benign in small quantities, they can deplete oxygen in high concentrations, leading to severe risks like suffocation. As oil production is projected to rise, so is the demand for gas sensors. These sensors are crucial for swiftly identifying gas leaks from equipment, pipelines, and storage tanks.

- Increasing awareness of workplace hazards related to toxic and hazardous gases is propelling the adoption of gas sensors, especially in sectors like oil and gas, chemicals, petrochemicals, metals, and mining. Given the potential risks, chemical industries often rely on gas sensors to trigger emergency systems when gas concentrations exceed safe limits.

- Production costs for gas sensors have increased, primarily due to technological advancements. Many sensors now incorporate cutting-edge technologies like microelectromechanical systems (MEMS) or nanotech, which, while enhancing performance, also complicate the fabrication process, thereby increasing costs. Developing these advanced sensor technologies necessitates substantial investments in research and development, further adding to the cost structure. While established players have adapted to these changes, newcomers and mid-tier manufacturers face significant hurdles.

- The gas sensors market faced notable disruptions due to the Russia-Ukraine conflict and subsequent economic slowdown. Rising inflation and interest rates curtailed consumer spending, dampening the demand for gas sensors. The trade tensions between the United States and China exacerbated global supply chain disruptions. Notably, the United States' stringent controls on semiconductor manufacturing equipment exports to China have hampered production in China's consumer electronics and automotive sectors.

Gas Sensors Market Trends

Carbon Monoxide (CO) Segment to Hold Significant Market Share

- Carbon monoxide (CO) poses a significant threat as it can cause intoxication, a leading factor in unpredictable morbidity and mortality, which is often linked to inhalation injuries from combustion. This underscores the critical need to identify optimal materials and technologies for detecting this hazardous gas. Metal oxide semiconductor (MOS) sensors have garnered attention, especially for their application in micro- or nano-thin film formats.

- While carbon monoxide is inherently toxic, it serves as a crucial, combustible, and eco-friendly energy source in industrial and metallurgical operations. It plays a pivotal role in redox reactions, aiding in metal purification. Notably, carbon monoxide is both highly flammable and prone to explosions. Given the potential dangers, the adoption of carbon monoxide sensors is on the rise. This trend is further propelled by increasingly stringent government regulations, particularly those emphasizing worker safety.

- Carbon monoxide detectors are indispensable in various industries, primarily for their ability to detect this colorless, odorless, and tasteless gas, which is otherwise imperceptible to human senses. Such sensors are pivotal in averting carbon monoxide poisoning, a condition that, when left unchecked, can lead to severe consequences, including loss of consciousness, seizures, or even death. In the United States alone, this silent killer prompts over 20,000 emergency room visits annually and stands as the most common fatal poisoning in many nations.

- Carbon monoxide (CO) can harm health by impeding oxygen delivery to the body's organs and tissues. Individuals with heart disease face heightened risks even at lower CO levels, experiencing symptoms like chest pain, reduced exercise capacity, and potentially additional cardiovascular complications with repeated exposure. The growing number of vehicles on the road generates a huge amount of CO, which creates a significant demand for gas sensors to analyze and detect gases in the environment. CO (Carbon Monoxide) gas sensors are crucial components in gas detection equipment, designed to identify carbon monoxide in various settings, from homes and automotive to industrial environments.

- According to the Environmental Protection Agency, the United States saw emissions of around 42.3 million tons of carbon monoxide (CO) in 2023, excluding those from wildfires. Such increased CO emissions create new market opportunities for segment growth.

Asia-Pacific Expected to Witness Major Growth

- After CO2, methane is the second most impactful greenhouse gas, significantly contributing to global warming. China is one of the top methane emitters from fossil fuel activities, and the nation is under pressure to rein in its methane output.

- Despite efforts outlined in China's recent methane plan issued by the Ministry of Ecology and Environment. These include inadequate data collection, tax regulatory standards, and ongoing technical and managerial hurdles in controlling methane emissions.

- The increase in energy prices due to geopolitical conflicts has caused a growing interest in alternative energy sources like Hydrogen. Hydrogen can potentially be a primary energy source for industrial and residential uses. The medical industry is projected to stay steady, with gas sensors in devices like capnography and breath analyzers.

- Gas sensors are crucial for detecting hydrogen leaks and ensuring Hydrogen's safe production, storage, and utilization. Japan invests heavily in Hydrogen as a clean energy source, with initiatives to develop hydrogen fuel cells for vehicles and power generation. Gas sensors are crucial for detecting hydrogen leaks, ensuring the safe production, storage, and utilization

- For instance, Japan's most prominent power generation company, JERA, intends to invest over USD 6 billion in ammonia and hydrogen fuel supplies by 2035. The company's primary focus will be on blue and green Hydrogen. Blue Hydrogen is generated from natural gas, which produces carbon emissions that are then captured and stored to minimize its greenhouse gas impact. In contrast, green Hydrogen is produced through water electrolysis-powered solar and wind energy renewable resources.

Gas Sensors Industry Overview

The gas sensors market is fragmented because of the presence of many players. The companies offering various types of gas sensors have technological product differentiation. Hence, they are adopting competitive pricing strategies to gain market share. Some of the key players include Membrapor AG, AlphaSense Inc., Nemoto & Co. Ltd, Figaro Engineering Inc., and Robert Bosch GmbH

October 2023-Figaro Engineering announced the opening of the Figaro Europe Office in Neuss, Germany. This strategic move aimed to bolster Figaro's presence in Europe by offering dedicated technical support to customers and local distributors. The office was expected to spearhead targeted marketing initiatives, underscoring Figaro's commitment to expanding its foothold in the European market.

October 2023 - MEMBRAPOR AG enhanced its NO2/CA-2 sensor, boosting its sensitivity to nearly double its capability. This advancement enabled the sensor to detect lower concentrations in the ppb range. The sensor features its established catalytic O3 filter, effectively mitigating the common O3 cross-sensitivity in electrochemical NO2 sensors. It introduced the NO2/CA-20 sensor, extending its measurement capabilities to ranges of up to 20 ppm.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand for Gas Sensors in Automobiles for Compliance with Governmental Regulations

- 5.1.2 Growing Awareness on Occupational Hazards across Major Industries

- 5.2 Market Challenges

- 5.2.1 Rising Costs and Lack of Product Differentiation

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Oxygen

- 6.1.2 Carbon Monoxide (CO)

- 6.1.3 Carbon Dioxide (CO2)

- 6.1.4 Nitrogen Oxide

- 6.1.5 Hydrocarbon

- 6.1.6 Other Types

- 6.2 By Technology

- 6.2.1 Electrochemical

- 6.2.2 Photoionization Detectors (PID)

- 6.2.3 Solid State/Metal Oxide Semiconductor

- 6.2.4 Catalytic

- 6.2.5 Infrared

- 6.2.6 Semiconductor

- 6.3 By Application

- 6.3.1 Medical

- 6.3.2 Building Automation

- 6.3.3 Industrial

- 6.3.4 Food and Beverages

- 6.3.5 Automotive

- 6.3.6 Transportation and Logistics

- 6.3.7 Other Applications

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.5.1 Brazil

- 6.4.5.2 Argentina

- 6.4.5.3 Mexico

- 6.4.6 Middle East and Africa

- 6.4.6.1 United Arab Emirates

- 6.4.6.2 Saudi Arabia

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Figaro Engineering Inc.

- 7.1.2 Membrapor AG

- 7.1.3 AlphaSense Inc.

- 7.1.4 Nemoto & Co. Ltd

- 7.1.5 Robert Bosch GmbH

- 7.1.6 Delphi Technologies

- 7.1.7 SGX Sensortech Ltd (Amphenol Corporation)

- 7.1.8 Zhengzhou Winsen Electronics Technology Co., Ltd.

- 7.1.9 Niterra Co. Ltd. (NGK-NTK)

- 7.1.10 Senseair (Asahi Kesai)

- 7.1.11 Drgerwerk AG & Co. KGaA

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE GROWTH