PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644886

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644886

North America Secure Access Service Edge - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

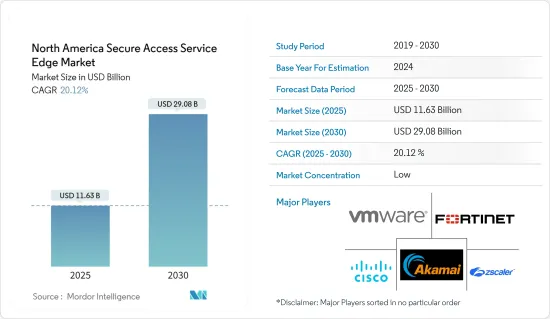

The North America Secure Access Service Edge Market size is estimated at USD 11.63 billion in 2025, and is expected to reach USD 29.08 billion by 2030, at a CAGR of 20.12% during the forecast period (2025-2030).

Demand for qualified individuals to implement, manage, and support SASE solutions increases as SASE adoption spreads. As a result, the number of training and certification programs provided by vendors and independent groups has increased. To enable the efficient deployment and use of these technologies, IT teams are concentrating on gaining competence in SASE.

Key Highlights

- SASE helps enterprises achieve strict compliance requirements by enforcing uniform security standards and encryption across the network. It minimizes the chances of regulatory infractions and related fines by safeguarding data during transmission and when kept in cloud applications. For instance, a healthcare institution is expected to abide by stringent regulatory standards for protecting patient data, including safeguarding data during information and idle state.

- The use of SASE is strongly encouraged by the shortage of sufficient security protocols and technologies. An all-encompassing and adaptable security solution like SASE is becoming increasingly necessary for organizations dealing with an expanding threat landscape, remote work issues, cloud migrations, and compliance obligations. In addition to addressing these urgent security issues, it closes the cybersecurity talent gap and guarantees scalability, business continuity, and resilience in the face of contemporary threats and difficulties.

- The mandatory observance of data privacy and regulatory legislation is a strong force behind expanding the SASE business. Businesses are realizing the necessity of a complete security solution like SASE to assist them in complying with strict data protection rules, avoiding penalties, and safeguarding their brand. The demand for SASE as a tool for assuring compliance is anticipated to grow as privacy legislation continues to change and spread internationally, making it an essential part of contemporary cybersecurity and data protection initiatives.

- The demand for cloud-based solutions surges due to the growing technological advances and consumer propensity toward the cloud. Technology allows the user to access data from remote locations. The increasing realization among companies about the cost and resource efficiency of shifting data to the cloud rather than maintaining on-premise infrastructure is driving the demand for cloud-based solutions among enterprises.

- The COVID-19 pandemic accelerated the enterprise's SASE adoption as digital transformation initiatives advanced rapidly. As cloud adoption continues to accelerate through the convergence of networking, security is critical to better support an increasingly remote and mobile workforce.

- In March 2023, Fortinet, the global cybersecurity firm driving the convergence of networking and security, announced several enhancements to FortiSASE, Fortinet's single-vendor SASE solution, enabling additional deployment flexibility and new secure access capabilities for digital resources across SaaS, private applications, and the internet.

North America Secure Access Service Edge Market Trends

IT and Telecom End-user Industry is Expected to Hold Significant Market Share

- North America, particularly the United States, is often a major player in the IT and telecom sectors. The region boasts a robust telecommunications industry, numerous technology companies, and significant investment in IT infrastructure. For instance, in May 2023, Kyndryl, a US-based supplier of IT infrastructure services, introduced a managed secure access service edge (SASE) solution powered by Fortinet that intends to assist clients in implementing advanced network security measures. The solution combines Kyndryl's network and security services with Fortinet's cloud-delivered security and secure networking solutions to design, construct, maintain, and upgrade mission-critical networking for clients across sectors. Such initiatives led to substantial adoption of SASE solutions in the IT and telecom end-user vertical.

- Moreover, network-as-a-service (NaaS) is essential for IT and telecom organizations because it provides the network infrastructure necessary for seamless communication, data transfer, and cloud connectivity. These organizations rely heavily on robust and scalable networking solutions. For instance, in July 2023, Lumen Technologies, a US-based telecom company, introduced its flagship feature on its network-as-a-service (NaaS) platform as a part of its plan to transform the telecom sector. Lumen is transforming traditional telecom into the cloud by giving consumers flexibility in purchasing, utilizing, and managing networking services.

- Overall, the IT and telecom end-user vertical growth in the SASE market is driven by the sector's specific cybersecurity needs, the imperative for secure remote access, the protection of telecommunications services, and the broader trends of digital transformation and cloud adoption.

- 5G's revolutionary latency, throughput, and reliability capabilities will support new industrial, business, and consumer services. It will encourage the global SASE vendors to embrace a more holistic view of the network and develop best practices to combat new security threats. Network as a service solution provider will get more lucrative opportunities to improve the network's cost efficiency with the advent of 5G. The rising integration of network automation and other technologies in the telecom industry is increasing the demand for 5G.

- According to GSMA, the forecasts revised for the impact of the COVID-19 pandemic expect a short-term slowdown in using 5G in North America. However, from 2023 to 2025, the 5G take-up is expected to account for 13 million more connections compared to the pre-COVID-19 forecast.

United States is Expected to Hold Significant Market Share

- The United States is a developed economy with a significant inclination toward implementing and accepting advanced technology, development in network automation, and surge in cloud-based services, thereby contributing to the secure access service edge market. Moreover, the growing digitization among end-user industries, coupled with the presence of prominent market vendors like Cisco Systems Inc., Vmware Inc., Palo Alto Networks, Versa Networks Inc., and Akamai Technologies, contribute to the market's growth.

- Further, security is moving to the cloud with the rapid acceleration of the digital transformation of businesses. Additionally, the significant adoption of cloud services in the end-user industries necessitates securing the network infrastructure and reducing complexity to improve speed and agility. This is analyzed to create substantial growth opportunities for market vendors in the coming years.

- By offering type, the network-as-a-service segment is analyzed to witness substantial growth in the United States over the coming years. The market is expected to grow significantly, owing to the greater penetration of cloud solutions across various industry verticals, the advent of IoT and Industry 4.0, and the growing number of DDoS and data breaches. All these factors are expected to drive the demand for network-as-a-service offerings in the United States. According to GSMA, in North America, by 2025, the number of industrial Internet of Things (IoT) and consumer connections is expected to increase to about 5.4 billion.

- Further, the country has three major cloud service providers: Amazon Web Services, Microsoft's Azure, and Google Cloud. It is also considered the hub for major technological innovations such as 5G, autonomous driving, IoT, blockchain, artificial intelligence, and gaming. Integrating SASE capabilities converges zero trust security capabilities into enterprise architectures, which is paramount in achieving a trusted network security posture. Thus, SASE solutions are analyzed to transform the end-user's network and security architecture to reduce cyber risk, costs, and complexity.

- Market vendors are capitalizing on the opportunity and launching innovative SASE solutions to enhance cyber resiliency through SASE solutions. For instance, in April 2023, Accenture and Palo Alto Networks collaborated to deliver joint secure access service edge (SASE) solutions powered by the Palo Alto Networks AI-powered Prisma SASE. The solution will enable organizations to improve cyber resilience and accelerate business transformation efforts.

North America Secure Access Service Edge Industry Overview

The North American secure access service edge market is fragmented with the presence of major players like Cisco Systems Inc., VMware Inc., Fortinet Inc., Akamai Technologies Inc., and Zscaler Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- April 2024: CloudCover formed a partnership with SHI International to extend the global reach of its advanced threat-prevention cybersecurity platform. SHI, a global leader in end-to-end IT solutions with an unparalleled supply chain, offers CloudCover's unique XDR/SASE security-as-a-service platform as part of its security portfolio. CloudCover delivers advanced cyber risk management, providing microsecond risk awareness and control. Additionally, it has established an in-network cybersecurity insurance system with methods that embed liability protection.

- January 2024: Kyndryl, a technology infrastructure services provider, introduced two advanced security services in partnership with Cisco. These services aim to enhance customers' security controls and enable proactive responses to cyber incidents. The new offerings, Kyndryl Consult Security Services Edge (SSE) with Cisco Secure Access and Kyndryl Managed SSE with Cisco Secure Access, represent a significant advancement in cybersecurity solutions.

- August 2023 - Versa Networks, the global provider in AI/ML powered Unified Secure Access Service Edge (SASE), announced a set of enhancements to VersaAI that includes new embedded generative AI capabilities to identify malicious behaviors in real-time, secure generative AI tools, and enhance network and security operational excellence.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Need For a Single Network Architecture that combines SD-WAN, FWaaS, SWG, CASB, and ZTNA Capabilities

- 5.1.2 Lack of Security Procedures and Tools

- 5.1.3 Mandatory Compliance with Data Protection and Regulatory Legislation

- 5.2 Market Restraints

- 5.2.1 Lack of Knowledge on Cloud Resources, Cloud Security Architecture, and SD-WAN strategy

- 5.2.2 Difficult in Accessing Such Dispersed Data While Managing And Safeguarding These Networks

6 MARKET SEGMENTATION

- 6.1 By Offering Type

- 6.1.1 Network-as-a-Service

- 6.1.2 Security-as-a-Service

- 6.2 By Organization Size

- 6.2.1 Large Enterprises

- 6.2.2 Small and Medium Enterprises

- 6.3 By EndUser Vertical

- 6.3.1 BFSI

- 6.3.2 IT and Telecom

- 6.3.3 Retail

- 6.3.4 Healthcare

- 6.3.5 Government

- 6.3.6 Manufacturing

- 6.3.7 Other End-user Industries

- 6.4 By Country

- 6.4.1 United States

- 6.4.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 VMware Inc.

- 7.1.3 Fortinet Inc.

- 7.1.4 Akamai Technologies Inc.

- 7.1.5 Zscaler Inc.

- 7.1.6 Cloudflare Inc.

- 7.1.7 Versa Networks Inc.

- 7.1.8 Broadcom Corporation

- 7.1.9 Forcepoint

- 7.1.10 Aryaka Networks Inc.

- 7.1.11 McAfee Corp.

- 7.1.12 Citrix Systems Inc.

- 7.1.13 Barracuda Networks Inc

- 7.1.14 Verizon Communications Inc.

- 7.1.15 Juniper Networks Inc.

- 7.1.16 Aruba Networks

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET