PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644616

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644616

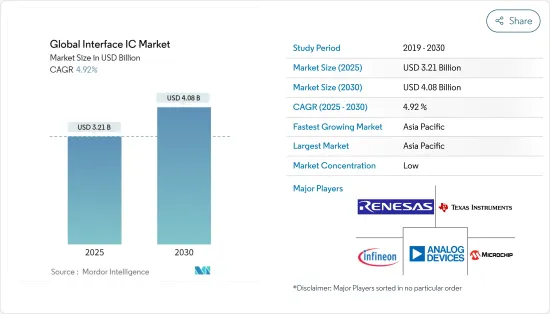

Global Interface IC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Global Interface IC Market size is estimated at USD 3.21 billion in 2025, and is expected to reach USD 4.08 billion by 2030, at a CAGR of 4.92% during the forecast period (2025-2030).

Interface ICs consolidate entire electronic interface circuit functions onto a single chip, ensuring cost-effective and reliable information sharing between devices. Their capability to manage and control communications across diverse electronic systems makes them integral to biometrics, electric vehicles, and telecommunications, fueling the demand for interface ICs in electronic circuit boards.

Key Highlights

- Integrated circuit (IC) interfaces are semiconductor chips that regulate and facilitate the transfer of information between devices. Performance parameters such as supply voltage, data rate, operational current, power dissipation, and temperature junction are all important considerations for IC interfaces. These interface-integrated circuits (ICs) play a crucial role in managing signal communications between different electronic systems.

- Interface ICs facilitate seamless communication and efficient collaboration among diverse electronic components and systems. By enabling the smooth exchange of data, control signals, and power within electronic devices, these ICs ensure optimal performance. They are specially designed to support a wide range of communication protocols and standards, including USB, HDMI, Ethernet, SPI, I2C, and CAN.

- The increasing demand for interface ICs is primarily driven by the proliferation of connected devices. As the IoT ecosystem rapidly expands, more devices require seamless communication and data transfer, where interface ICs are essential for facilitating this data exchange among various components and systems. Consequently, as sectors ranging from consumer electronics to industrial automation experience a rise in connected devices, the demand for these critical chips intensifies. According to Ericsson, the total number of connected devices across the globe is expected to reach 45.72 billion by 2029.

- The consumer electronics market is advancing with innovative products and features. Smartphones, tablets, wearables, and smart home devices are now being incorporated with multiple sensors, cameras, and connectivity options, requiring interface ICs as they enable the seamless integration of these components, providing advanced functionalities and enhancing user experiences.

- The increasing complexities of electronic devices have led to sophisticated system-on-chip (SoC) designs, presenting significant challenges for interface IC integration. Balancing performance, power consumption, and space constraints within the SoC requires careful consideration of interface IC selection and placement, complicating design cycles and raising development costs.

Interface IC Market Trends

Automotive Industry to be the Fastest Growing End User

- The market for electric and hybrid vehicles in the automotive sector is experiencing significant growth. The advancements in automotive technology and manufacturing are also increasing the demand for compact, power-efficient devices.

- The increasing usage of advanced driver-assistance systems (ADAS) and the implementation of government regulations worldwide that require ADAS are also broadening the potential of this sector. The rising adoption of vehicle infotainment will offer growth opportunities. The ongoing advancements in automotive digital applications necessitate the continual development of interface IC and technologies.

- The automotive sector is one of the significant end users of interface IC. The advancements in automotive technology and manufacturing are increasing the need for compact, energy-efficient electronics. The swift expansion of 5G networks and the rising popularity of Internet of Things (IoT) applications like assisted driving and vehicle-to-everything communication for intelligent transportation are expected to increase demand for interface ICs.

- Synaptics Incorporated introduced the SmartBridge SB7900 local dimming IC in January 2023, enabling larger, higher-contrast, higher-resolution car LCDs at a reduced cost and power consumption. The SB7900 SmartBridge offers improved image quality, increased system flexibility, decreased device footprint, power usage, and complexity for displays up to 30 inches and resolutions up to 6K. This is achieved by integrating the capability to drive multiple touch and display driver-integrated (TDDI) controllers with local dimming technology for the backlight array.

- With the increasing production of passenger cars across the region, the adoption of Advanced Driver Assistance Systems (ADAS) has risen significantly. This trend is expected to drive the demand for interface integrated circuits (ICs), as these components ensure seamless communication and data transfer among various sensors, processors, and actuators.

- These ICs handle high-speed data from cameras, radars, and LiDAR sensors, ensuring accurate and timely information processing. According to the International Organization of Motor Vehicle Manufacturers (OICA), China was the largest producer of passenger cars with 26,123.76 units, followed by Japan with 7,765.43 units.

Asia-Pacific to Register Major Growth

- The Asia-Pacific region is home to a considerable number of global semiconductor manufacturing facilities, prominently featuring industry leaders such as TSMC and Samsung Electronics. Key nations within this region, including Taiwan, South Korea, Japan, and China, possess substantial market shares.

- The region is anticipated to capture a significant portion of the market due to a high volume of semiconductor manufacturing activities. According to WSTS, a remarkable increase in semiconductor sales is projected, with a year-on-year growth of 17.5% in 2024 and 12.3% in 2025, driven by the rising demand for integrated circuits.

- The growing investments in the consumer electronics industry across various countries like India, China, Japan, and others are significantly driving the growth of the demand for interface integrated circuits. For instance, the market is expected to witness a significant demand across India's consumer electronics industry. Initiatives such as "Make in India" and "Digital India" have catalyzed expansion within the consumer electronics industry. These strategies are designed to enhance domestic manufacturing and digital infrastructure, thereby decreasing reliance on imports and increasing the accessibility and affordability of electronics for the Indian population. Such initiatives are expected to boost the market opportunities.

- As reported by IBEF, India has established itself as a prominent manufacturing center, with its domestic electronics production increasing from USD 29 billion in 2014-15 to USD 101 billion in 2022-23. Recently, the Ministry of Electronics & Information Technology published the second volume of the Vision document on Electronics Manufacturing in India, which projects that the electronics manufacturing sector will expand from USD 75 billion in 2020-21 to USD 300 billion by 2025-26. These substantial factors are anticipated to enhance the growth of the market.

- According to IBEF, the primary products anticipated to propel growth in India's electronics manufacturing sector include mobile phones, IT hardware such as laptops and tablets, consumer electronics like televisions and audio devices, industrial electronics, as well as wearables and wearables, among others.

- The electronics industry in India has experienced a remarkable 154% increase in overall hiring in March 2024 compared to the same period last year, as reported by research from Quess Corp. Limited. These notable advancements in the region are projected to enhance the demand for interface ICs throughout the electronics industry.

- The region's significant developments in the smartphone segment are also expected to drive market opportunities. IBEF stated that India has emerged as the second-largest mobile phone manufacturing nation, following China. Over the past decade, mobile phone production in India has increased twenty-onefold, achieving a value of USD 49.3 billion (INR 4.1 lakh crore). This remarkable growth can be attributed primarily to government initiatives, including the Production Linked Incentive (PLI) scheme. As a result, India is now capable of fulfilling 97% of its domestic mobile phone demand, which will create enormous market opportunities.

Interface IC Industry Overview

The interface IC market is highly fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are Infineon Technologies AG, Renesas Electronics Corporation, Texas Instruments Incorporated, Analog Devices Inc., and Microchip Technology Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- July 2024 - Analog Devices Inc., a global player in semiconductors, teamed up with Flagship Pioneering, a pioneer in bio-platform innovations, to fast-track the evolution of a fully digitized biological realm. By merging ADI's prowess in analog and digital semiconductor engineering with Flagship Pioneering's applied biology expertise, the collaboration aims to unveil deeper biological insights, refine measurements, enhance diagnostics, and introduce innovative interventions.

- April 2024 - Microchip Technology acquired Neuronix AI Labs, enhancing its power-efficient, AI-driven edge solutions on field programmable gate arrays (FPGAs). Neuronix AI Labs specializes in neural network sparsity optimization, allowing for reduced power consumption, size, and computational needs in tasks like image classification, object detection, and semantic segmentation, all while ensuring high accuracy.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact Analysis of COVID-19 and Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Usage of Connected Devices and Communication Technologies

- 5.1.2 Increasing Demand for Consumer Electronics Such as Smartphones, Tablets, and Wearables, Driving Demand in the Market

- 5.2 Market Restraints

- 5.2.1 Complexity in Design and Integration Challenges in the Manufacturing Process

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 CAN Interface IC

- 6.1.2 USB Interface IC

- 6.1.3 Display Interface IC

- 6.1.4 Other Product Types

- 6.2 By End-user Industry

- 6.2.1 Consumer Electronics

- 6.2.2 Telecom

- 6.2.3 Industrial

- 6.2.4 Automotive

- 6.2.5 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Infineon Technologies AG

- 7.1.2 Renesas Electronics Corporation

- 7.1.3 Texas Instruments Incorporated

- 7.1.4 Analog Devices, Inc.

- 7.1.5 Microchip Technology Inc

- 7.1.6 NXP Semiconductors Nv

- 7.1.7 Broadcom Inc.

- 7.1.8 SEIKO Epson Corporation

- 7.1.9 Toshiba Corporation

- 7.1.10 ON Semiconductor Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK