PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690783

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690783

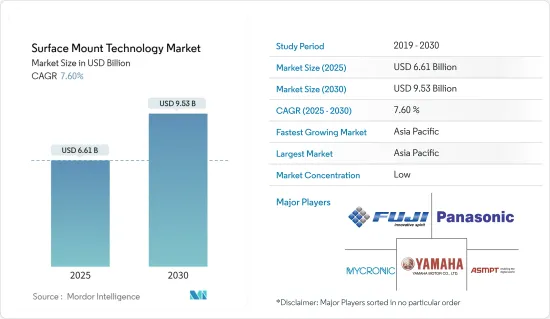

Surface Mount Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Surface Mount Technology Market size is estimated at USD 6.61 billion in 2025, and is expected to reach USD 9.53 billion by 2030, at a CAGR of 7.6% during the forecast period (2025-2030).

Surface mount technology (SMT) is a method for constructing electronic circuits in which the components are mounted directly onto the surface of printed circuit boards (PCBs). This contrasts with older through-hole technology, where components are inserted into holes drilled into the PCB. Components used in SMT, known as SMDs, have small metal tabs or end caps that can be soldered directly onto the PCB surface. This allows for using smaller, lighter, and more components on a single PCB.

After the effect of the pandemic, the market for laptops and servers is witnessing a surge in demand. According to the India Electronics and Semiconductor Association (IESA), more data is stored on the cloud as work-from-home increases and more collaboration tools are deployed. A surge in demand is witnessed in the server, data centers, and computing segments. US-based Micron Technology also reported a more robust demand from data centers due to the remote-work economy, increased gaming, and e-commerce activity. Additionally, as per Cloudscene, as of March 2024, there are 5,381 data centers in the United States, the most of any country worldwide. A further 521 are in Germany, while 514 are in the United Kingdom.

Miniaturization of electronic components has made it possible to build small portable and handheld computer devices that can be carried anywhere. As a result, smaller, lighter devices with high processing capacity are available on the market. They are becoming more wearable since components can be easily embedded (for example, in clothing bags) and carried for long periods. Components are shrinking, putting new demands on the design of the PCBs they are mounted on. NCAB Group is firmly committed to IPC's efforts in defining standards for ultra-dense Ultra HDI PCBs and anticipates being able to provide them to clients in 2023.

Surface mount technology (SMT) has emerged as a pivotal element in modern electronics manufacturing, eclipsing traditional through-hole methods with its myriad benefits. A standout advantage of SMT lies in its drastic reduction of necessary PCB drilling. Manufacturers slash both time and costs by sidestepping the drilling process, a notable boon for intricate, high-density boards. This shift streamlines production and trims labor and material expenses, bolstering the overall cost-effectiveness of the manufacturing process.

Surface mount technology has revolutionized the electronics manufacturing industry by enabling the production of smaller, more efficient, and cost-effective electronic devices. However, despite its numerous advantages, SMT is unsuitable for all applications. SMT is unsuitable for high-power and high-voltage components, such as transformers and power circuitry. These components generate heat and carry high electric loads, which SMT is not designed to handle effectively.

According to the US Congressional Budget Office, defense spending in the United States is predicted to increase yearly until 2033. Defense outlays in the United States amounted to USD 746 billion in 2023. The forecast predicts an increase in defense outlays up to USD 1.1 trillion in 2033.

Surface Mount Technology (SMT) Market Trends

Consumer Electronics End-user Industry Segment is Expected to Hold Significant Market Share

- In the automotive industry, SMT is used in Electronic Control Units (ECU), dashboard displays, radar and camera modules, Battery Management Systems (BMS), safety assistance systems, and more. SMT has emerged as a pivotal manufacturing process in the automotive application. Renowned for its efficiency, precision, and reliability, SMT is crucial in bolstering various automotive electronic products, including advanced driver-assistance systems (ADAS), infotainment systems, and vehicle control systems.

- In modern cars, the on-board control system acts as the vehicle's 'brain,' overseeing and harmonizing the functions of its electronic components. The on-board control system is crucial in their seamless operation, from navigation to audio and air conditioning. Central to the reliability of these control systems is SMT technology. This technology enables the precise mounting of minuscule electronic components on circuit boards, ensuring the systems operate efficiently and reliably.

- The Engine Control Unit (ECU) is the automotive electronic system's nucleus, overseeing critical operations like engine performance, transmission, and braking. Surface-mount technology (SMT) is essential in assembling microchips, resistors, capacitors, and other surface-mounted components onto the ECU.

- Furthermore, Artificial Intelligence technology is poised to see increased adoption in the automotive sector. The precision and efficiency of Surface Mount Technology (SMT) in electronic assembly are set to bolster the production of AI chips and processors. Consequently, automotive electronic products will have enhanced autonomous decision-making abilities, advancing intelligent driving and vehicle automation.

- As highlighted by the IEA, the global automotive industry is undergoing a significant transformation, with potentially far-reaching implications for the energy sector. According to projections, the rise of electrification is anticipated to result in a daily elimination of the need for 5 million barrels of oil by 2030.

- The IEA's report also revealed a substantial increase in electric vehicle sales, with 3.5 million units sold in 2023 compared to 2022, marking a 35% growth. Notably, over 250,000 new registrations were recorded weekly, and over 250,000 new registrations were recorded weekly throughout the year. In 2023, electric vehicles accounted for approximately 18% of all vehicles sold, a significant increase from 2% five years ago and 14% in 2022. These trends indicate that solid growth is expected to persist as the electric vehicle market matures. Additionally, it was projected that 70% of the electric vehicle stock in 2023 would consist of battery electric vehicles.

Asia Pacific is Expected to Witness Fastest Growth

- Asia-Pacific, particularly countries like Japan, China, South Korea, Taiwan, and Southeast Asia, has become a global hub for electronics manufacturing. The region's robust manufacturing infrastructure, skilled labor force, and supportive government policies attract multinational corporations and promote the growth of local electronics industries. Demand for tablets, smartphones, and other electronic devices continues to grow, necessitating efficient and high-volume production capabilities by surface mount technology. The company projects that by implementing SMT (Surface Mount Technology) locally, the value addition will increase to 25% from the current 15%.

- For instance, in August 2023, the Indian government is actively engaging with global electronics firms to ramp up local value addition in products assembled in India, targeting a significant increase of 60-80% over the next five to ten years. To achieve this, the government is urging industries in India to adopt advanced production methods, like surface-mount technology (SMT) lines.

- Silicon Carbide (SiC) is increasingly in the spotlight for its high-temperature resilience, superior electrical conductivity, and remarkable energy efficiency. As the demand for electric vehicles (EVs), solar panels, and advanced power management rises with Industry 4.0, SiC manufacturing's significance has heightened. Wide Band Gap conductors are a natural fit given the imperative for minimal power consumption in these sectors.

- In February 2024, Continental Device India Limited (CDIL) took a significant step by inaugurating a new assembly line specifically for SiC Surface Mount Technology (SMT) components. This move positions CDIL as India's pioneer in SiC component manufacturing. With this enhancement, CDIL can now produce a range of auto-grade devices, such as SiC Schottky Diodes, SiC MOSFETs, Zeners, Rectifiers, and TVS Diodes, catering to both global and domestic markets.

- In April 2024, TDK Corporation introduced the B40910 series, a line of hybrid polymer capacitors designed to handle up to 4.6 A (at 100 kHz and +125 °C). These surface mount components boast impressively low ESR values of 17 mΩ and 22 mΩ at room temperature.

- Notably, unlike standard electrolytic capacitors with liquid electrolytes, the ESR of TDK's capacitors shows minimal variation with temperature. These compact components, measuring 10 x 10.2 mm or 10 x 12.5 mm (D x H), feature a rated voltage of 63 V and offer capacitances ranging from 82 µF to 120 µF. Thus, SMT manufacturers drive the need for the technology by integrating and innovating technologies. These efforts contribute to the widespread adoption and growth of surface mount technology (SMT) in various industries.

Surface Mount Technology (SMT) Industry Overview

Surface Mount Technology market is highly fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are Fuji Corporation, Yamaha Motor Co. Ltd, Mycronic AB, ASMPT, and Panasonic Corporation. Players in the market are adopting partnerships and acquisitions to enhance their product offerings and gain competitive advantage.

March 2024 - Nordson Corporation introduced a new Latin America Tech Center based in Queretaro, Mexico, to allow manufacturers in the region to get timely feedback on the best fluid dispensing equipment for their assembly fluid, parts, substrates, and production requirements. The lab has a 3D printer, scales, and other measurement equipment to determine the correct fluid dispensing equipment for each customer's unique application requirements.

January 2024 - Yamaha Motor Co. Ltd announced the launch of YRM10, a surface mounter with the title of being the fastest in its class regarding mounting performance. With an impressive speed of 52,000 CPH, it outshines its competitors in the 1-Beam/1-Head category. This device is compact and space-saving and offers a range of component compatibility and versatility, making it a next-generation solution for high-speed modular assembly.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Surface Mount Technology Market

5 MARKET DYNAMICS

- 5.1 Rising Demand For Miniaturization of Technology

- 5.1.1 Fewer Holes Required to Drill on PCBs Compared to Other Technologies

- 5.2 Market Challenges

- 5.2.1 SMT is Unsuitable for Any Large, High-Power and High-Voltage Parts and Parts Undergoing Frequent Mechanical Stress

- 5.2.2 High Initial Cost and Rework Issues

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Passive Components

- 6.1.1.1 Resistors

- 6.1.1.2 Capacitors

- 6.1.2 Active Components

- 6.1.2.1 Transistors

- 6.1.2.2 Integrated Circuits

- 6.1.1 Passive Components

- 6.2 By End-user Industry

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive

- 6.2.3 Industrial Electronics

- 6.2.4 Aerospace and Defense

- 6.2.5 Healthcare

- 6.2.6 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fuji Corporation

- 7.1.2 Yamaha Motor Co. Ltd

- 7.1.3 Mycronic AB

- 7.1.4 ASMPT

- 7.1.5 Panasonic Corporation

- 7.1.6 Nordson Corporation

- 7.1.7 Juki Corporation

- 7.1.8 Hanwa Precision Machinery Co. Ltd

- 7.1.9 Zhejiang Neoden Technology Co. Ltd

- 7.1.10 Europlacer Limited

- 7.1.11 Viscom SE

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS