PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1641958

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1641958

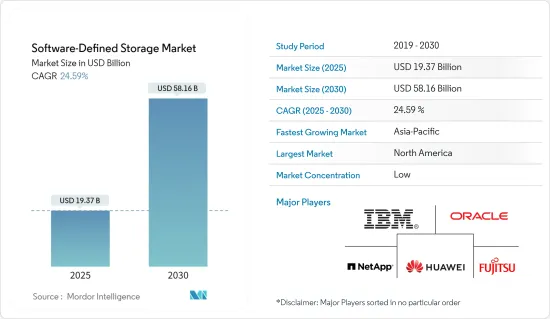

Software-Defined Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Software-Defined Storage Market size is estimated at USD 19.37 billion in 2025, and is expected to reach USD 58.16 billion by 2030, at a CAGR of 24.59% during the forecast period (2025-2030).

The software-defined storage (SDS) enables organizations to abstract storage resources from the hardware platform, offering flexibility, efficiency, and faster scalability. In the software-designed data center (SDDC) architecture, resources can be easily automated and orchestrated rather than residing in siloes. The need to improve efficiency and business processing with data drives the demand for SDS solutions in small and medium-sized enterprises.

Due to the competitive environment, companies have shifted their focus toward new technology to have a competitive edge. SDS usage helps minimize the cost by automating process controls and replacing traditional hardware with software.

The booming volume of unstructured data across various enterprises augments the demand for a scalable storage architecture that is reliable and secure. In addition, with the proliferation of IoT globally, the data generated at the edge is rapidly increasing. The SDS model addresses these needs by increasing deployment flexibility and enabling organizations to use the software with any storage platform through a single interface.

Due to this technology's advantages over traditional storage methods, enterprises or IT organizations undergoing digital transformation will likely adopt SDS for their data storage needs. However, the need for more skilled operators to manage the transition toward SDS and security concerns will hinder the market's growth.

The key vendors in the market have been rolling out SDS software solutions with enhanced data protection and reliability, owing to the growing requirements of large companies in the banking and telecom sectors.

The COVID-19 pandemic resulted in private and public sectors shifting from traditional channels to digital channels to enable citizens, businesses, and public sector staff to access public services and securely share data from remote locations. Software-defined storage has proven its importance for businesses during the pandemic and is anticipated to see continued growth in data storage post-pandemic.

Software-Defined Storage Market Trends

The BFSI Segment is Expected to Witness Significant Growth

- The banks are a highly regulated operational environment with exponential data growth and require highly secure and highly available storage capabilities to integrate, scale up, and out with appliances that link together across sites. The software-defined storage solutions help improve BFSI operations, including handling massive data sets, limited access to files with encryption, and even data backup and recovery.

- The BFSI segment is highly competitive, leveraging technology to ensure its IT infrastructure is highly flexible to meet dynamic market demands. Software-defined data centers enable banks to launch an aggregator app, consolidating the frequently used apps by retail customers. Benefits such as ease of operation from a single app for different use cases like food, travel, and e-commerce and integration of payment options are helping customers in everyday banking activities.

- The rising need for better managing vast data from BFSI contributes a substantial share of the software-defined storage market. The BFSI segment is anticipated to record the fastest growth during the forecast period, attributed to the increasing demand for customer data analysis to achieve a competitive advantage and boost the ongoing digital transformation in the segment.

- With the increase in the digital economy, data is an essential part of the banking industry. Software-defined infrastructure and storage solutions enable global banks to rapidly access, analyze, and share on-premises data in the cloud from front-to-back office operations.

Asia-Pacific is Expected to Witness Fastest Growth

- Asia-Pacific is experiencing rapid growth in the volume of unstructured data across various enterprises, which is being stored in on-premises devices and cloud environments. Also, with the proliferation of the internet of things (IoT) across the region, the data generated at the edge is drastically increasing.

- The adoption of online payments is rising exponentially, generating a huge amount of data daily, which the companies need to process, propelling the demand for software-defined storage solutions.

- Moreover, the key vendors, such as FalconStor, which provides SDS in China through Huawei, indicated that customers/enterprises in Asia-Pacific, including China, are one of the greatest potential markets for IT services and are positive about switching to modern storage solutions. The propensity to shift is mainly to overcome challenges such as data security, recovery, and the integration of virtual and non-virtualized resources.

- The use of cloud storage is poised to increase aggressively, driven by the country's rising number of internet users.

- Emerging economies like China and India are still dependent on traditional hardware for storage and the need for digital transformation to stay up with technological advancements; these countries are expected to provide a potential commercial opportunity for software-defined storage (SDS) suppliers during the forecast period.

Software-Defined Storage Industry Overview

The software-defined storage market is fragmented, with major players like IBM Corporation, Oracle Corporation, and NetApp Inc. The key players in the market are continuously innovating new products and rising activities such as mergers and acquisitions and capacity expansion, further increasing the competition.

November 2023: DDN, a provider of multi-cloud data management solutions, has announced DDN Infinia, a next-generation software-defined storage platform. This platform leverages data orchestration and AI-based optimization to accelerate computing and generative AI. DDN Infinia combines multi-tenancy, containerization, and the highest levels of speed and efficiency with ease of management and powerful security attributes. The solution simplifies workflows for the data management demands.

September 2023: TD Securities, a Canadian investment bank that focuses on wholesale banking such as currency conversion and large trades, introduced its TD Securities' block storage setup made up of several storage pockets, making it hard to maintain. General infrastructure specialists managed storage at TD Securities. TD Securities has thus selected to move forward with a software-defined storage system, Dell PowerMax.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of Macroeconomic on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapidly Growing Volume of Data Across Enterprises

- 5.1.2 Increased Demand for Industrial Mobility for Remotely Managing the Process Industry

- 5.2 Market Challenges

- 5.2.1 High Cost and Compliacted in Installation

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Block

- 6.1.2 File

- 6.1.3 Object

- 6.1.4 Hyper-converged Infrastructure

- 6.2 By Size of Enterprise

- 6.2.1 Small and Medium Enterprise

- 6.2.2 Large Enterprise

- 6.3 By End-user Industries

- 6.3.1 BFSI

- 6.3.2 Telecom and IT

- 6.3.3 Government

- 6.3.4 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Oracle Corporation

- 7.1.3 Netapp Inc.

- 7.1.4 Huawei Technologies Co. Ltd

- 7.1.5 Fujitsu Limited

- 7.1.6 Genetec Inc.

- 7.1.7 VMWare Inc. (Dell Inc.)

- 7.1.8 Hitachi Vantara Corp.

- 7.1.9 Pure Storage Inc.

- 7.1.10 Promise Technology Inc.

- 7.1.11 FalconStor Software Inc.

- 7.1.12 StarWind Software Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET