PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851327

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851327

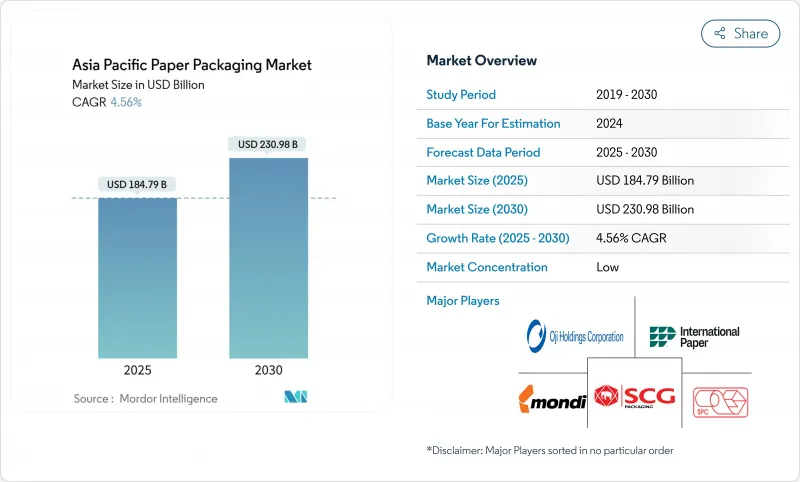

Asia Pacific Paper Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

Asia Pacific paper packaging market size reached USD 184.79 billion in 2025 and is forecast to climb to USD 230.98 billion by 2030, reflecting a 4.56% CAGR over the period.

Robust urbanization exceeding 60% across leading economies, coupled with e-commerce that already commands 80% of packaging demand, underpins near-term volume expansion. Region-wide adoption of Extended Producer Responsibility (EPR) regimes in Vietnam, Australia and Thailand is steering capital toward recycled grades and high-barrier coatings, thereby nudging average selling prices upward while trimming virgin-fiber exposure. Containerboard remains the workhorse substrate because corrugated formats dominate last-mile logistics, yet carton board is rapidly gaining favor in premium consumer goods and regulated healthcare channels as brand owners prioritize print quality, barrier functionality and sustainability. Producers are investing in AI-enabled design software and short-run digital printing to satisfy explosive SKU proliferation, even as hardwood pulp price swings and Chinese over-capacity keep margins under pressure.

Asia Pacific Paper Packaging Market Trends and Insights

Surge in e-commerce packaging demand

Corrugated formats now ship 80% of all e-commerce parcels in Asia Pacific, pushing annual box volumes to record highs and spurring mill conversions from newsprint to recycled containerboard.Chinese express shipments alone generated roughly 22 million tons of packaging waste in 2024, prompting municipal pilots that subsidize reusable corrugated totes. Regional sellers simultaneously deploy fit-to-product systems that trim board usage by up to 30% without sacrificing protection, heightening demand for algorithm-based design services. Manufacturers are therefore establishing micro-hubs that bring die-cutting and digital print capacity closer to fulfillment centers, allowing 24-hour turnaround on custom graphics. Intensifying competition in same-day delivery widens the opportunity for lightweight, high-strength fluting grades that lower last-mile freight costs.

Rapid shift toward recycled paper grades

Vietnam's EPR decree mandates 20% recycling for carton packaging beginning 2024, accelerating mill investment in closed-loop fiber recovery lines that boost de-inking capacity. Australia's 2024 draft regulation sets minimum recycled-content thresholds for all packaging, transferring liability to brand owners should targets be missed and elevating demand for certified post-consumer fiber. India already derives 70% of paper output from non-wood sources, offering domestic converters a cost hedge against virgin pulp volatility. Higher dependence on secondary fibers, however, raises energy intensity 15-20% owing to contaminant removal, prompting mills to pilot enzyme-assisted cleaning technologies. Early adopters tout double-digit EPR-fee savings, positioning recycled-grade specialists as preferred suppliers to multinational consumer-goods clients.

Pulp price volatility and supply shocks

Hardwood pulp averaged 30% price inflation during 2024 as climate events constrained forestry output, forcing Asian mills to announce USD 31.50 per-ton price hikes for early 2025. Currency depreciation in Indonesia and Thailand inflated landed costs a further 5-10%, eroding converter margins tied to fixed contracts. Import-heavy processors responded by forward-buying to lock in supplies, but storage constraints and inventory value-at-risk limit this tactic. Substitution toward recycled fibers lowers exposure, yet quality variation in recovered material heightens run-rate instability. Mills with captive plantations or balanced fiber baskets thus gain negotiating leverage over downstream box-plants.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of food, beverage and healthcare sectors

- EPR and content-mandate regulations across APAC

- Cost-competitive flexible plastic alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Containerboard controlled 58.34% of 2024 revenue as corrugated cases became the default shipper for omnichannel retail. The Asia Pacific paper packaging market size for containerboard is forecast to expand steadily, supported by fit-to-product algorithms that maintain board demand even as weights decline. Carton board's 5.54% CAGR reflects premium positioning: folding boxboard and solid bleached sulfate satisfy high-graphic food, beauty and pharma needs, capturing share from rigid plastics.

Investment momentum favors recycled containerboard, illustrated by Norske Skog's EUR 320 million Golbey conversion that will add 550,000 tpa of RCF-based liner by 2025. Integrated giants exploit captive OCC streams, whereas niche carton specialists capitalize on shorter change-over times and print-surface excellence. As EPR fees tilt cost curves toward recyclability, mid-sized independents face consolidation pressure or must pivot to service-driven carton niches.

Other Testliners held 39.56% of containerboard volume in 2024, benefiting from abundant recovered fiber and lower cost. Asia Pacific paper packaging market share for these grades could erode as brand owners demand stronger, brighter, white-top variants that lift shelf appearance. White-top kraftliner is growing fastest at 6.68% CAGR because high-definition flexo and digital graphics migrate onto shipper cartons, a trend amplified by social-media unboxing.

Folding boxboard dominated carton board grades at 41.45% while also leading grade growth at 6.23% CAGR. Next-generation clay and PVOH coatings grant water-vapor transmission rates suitable for dairy powders, anchoring FBB's expansion. Producers that retrofit curtain-coaters can pivot between grease-proof food liners and pharma blister-wallet backers, enhancing asset flexibility. Mills lacking coating capability will likely cede ground to integrated rivals that bundle substrate, design and compliance documentation.

The Asia Pacific Paper Packaging Market Report is Segmented by Packaging Type (Carton Board, Containerboard), Product (Folding Cartons, Corrugated Boxes, Liquid Packaging Board, Paper Bags), End-User Industry (Food, Beverage, Healthcare, Personal Care, Electronics, and More), and Country (China, India, Japan, Indonesia, Thailand, Vietnam, Australia, Rest of APAC). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Nine Dragons Paper (Holdings) Ltd

- Oji Holdings Corporation

- SCG Packaging PCL

- International Paper Co. (APAC)

- Mondi Group

- Smurfit WestRock plc

- Huhtamaki Oyj

- Rengo Co. Ltd

- DS Smith plc

- Pratt Industries

- Stora Enso Oyj

- Nippon Paper Industries

- APP (Asia Pulp & Paper) Group

- Visy Industries

- Harta Packaging Industries

- Sarnti Packaging Co. Ltd

- Hong Thai Packaging Co. Ltd

- New Asia Industries Co. Ltd

- C&H Paperbox (Thailand) Co. Ltd

- Continental Packaging (Thailand) Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in e-commerce packaging demand

- 4.2.2 Rapid shift toward recycled paper grades

- 4.2.3 Expansion of food, beverage and healthcare sectors

- 4.2.4 High-barrier coated paper replacing plastics

- 4.2.5 EPR and content-mandate regulations across APAC

- 4.2.6 Generative?AI-enabled design and short-run printing

- 4.3 Market Restraints

- 4.3.1 Pulp price volatility and supply shocks

- 4.3.2 Cost-competitive flexible plastic alternatives

- 4.3.3 Carbon-intensity pressure on paper mills

- 4.3.4 Chinese over-capacity driving price wars

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Type

- 5.1.1 Carton Board

- 5.1.2 Containerboard

- 5.2 By Grade

- 5.2.1 Carton Board

- 5.2.1.1 Solid Bleached Sulfate (SBS)

- 5.2.1.2 Solid Unbleached Sulfate (SUS)

- 5.2.1.3 Folding Boxboard (FBB)

- 5.2.1.4 Coated Recycled Board (CRB)

- 5.2.1.5 Uncoated Recycled Board (URB)

- 5.2.2 Containerboard

- 5.2.2.1 White-top Kraftliner

- 5.2.2.2 Other Kraftliners

- 5.2.2.3 White-top Testliner

- 5.2.2.4 Other Testliners

- 5.2.2.5 Semi-chemical Fluting

- 5.2.2.6 Recycled Fluting

- 5.2.1 Carton Board

- 5.3 By Product

- 5.3.1 Folding Cartons

- 5.3.2 Corrugated Boxes

- 5.3.3 Liquid Packaging Board

- 5.3.4 Paper Bags and Sacks

- 5.4 By End-User Industry

- 5.4.1 Food

- 5.4.2 Beverage

- 5.4.3 Healthcare and Pharmaceuticals

- 5.4.4 Personal Care and Cosmetics

- 5.4.5 Household Care

- 5.4.6 Electrical and Electronics

- 5.4.7 Other End-user Industry

- 5.5 By Country

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Japan

- 5.5.4 Indonesia

- 5.5.5 Thailand

- 5.5.6 Vietnam

- 5.5.7 Australia and New Zealand

- 5.5.8 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nine Dragons Paper (Holdings) Ltd

- 6.4.2 Oji Holdings Corporation

- 6.4.3 SCG Packaging PCL

- 6.4.4 International Paper Co. (APAC)

- 6.4.5 Mondi Group

- 6.4.6 Smurfit WestRock plc

- 6.4.7 Huhtamaki Oyj

- 6.4.8 Rengo Co. Ltd

- 6.4.9 DS Smith plc

- 6.4.10 Pratt Industries

- 6.4.11 Stora Enso Oyj

- 6.4.12 Nippon Paper Industries

- 6.4.13 APP (Asia Pulp & Paper) Group

- 6.4.14 Visy Industries

- 6.4.15 Harta Packaging Industries

- 6.4.16 Sarnti Packaging Co. Ltd

- 6.4.17 Hong Thai Packaging Co. Ltd

- 6.4.18 New Asia Industries Co. Ltd

- 6.4.19 C&H Paperbox (Thailand) Co. Ltd

- 6.4.20 Continental Packaging (Thailand) Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment