PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692112

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692112

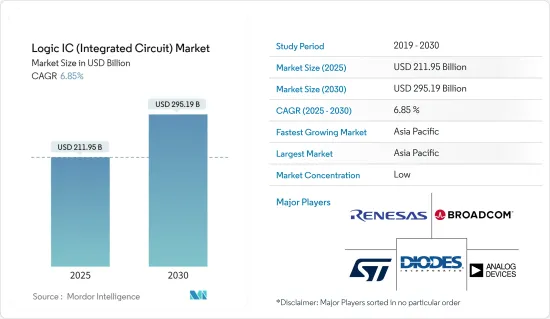

Logic IC (Integrated Circuit) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Logic IC Market size is estimated at USD 211.95 billion in 2025, and is expected to reach USD 295.19 billion by 2030, at a CAGR of 6.85% during the forecast period (2025-2030). In terms of shipment volume, the market is expected to grow from 67.97 billion units in 2025 to 83.46 billion units by 2030, at a CAGR of 4.19% during the forecast period (2025-2030).

Ongoing advancements in semiconductor manufacturing processes have led to the development of more complex and efficient logic ICs. Smaller transistor sizes, improved performance, and lower power consumption enable the creation of high-performance logic ICs for a wide range of applications. A logic IC is very flexible and can be used in various applications. One can configure them to perform multiple logical functions, such as AND, OR, NOT, and XOR. This flexibility allows for designing and developing intelligent circuits that meet requirements in different industries, such as consumer electronics, automotive, telecommunications, and industry automation.

Key Highlights

- Logic ICs have significantly aided the miniaturization and integration of electronic devices. The development of the technology to manufacture semiconductors has produced small, more complex logic circuits on a single chip in recent years. This integration increases functionality while reducing electronic systems' physical size and energy consumption so that they can be used in portable devices, wireless technology, or space-constrained applications. Display drivers, general purpose logic, and MOS touch screen controllers are some of the logic components that have gained significant market traction in recent years.

- Furthermore, advances in end-user industries have created the need for small and robust semiconductor devices. For instance, nowadays, smartphones require a smaller PCB board, unlike traditional PCB boards. There has also been the advent of IoT devices, such as wearables with irregular and different shapes, which can only be achieved through miniaturization. This is expected to boost the need for miniaturized IC components significantly.

- The advent of the IoT and IIoT has largely impacted the design and size of electronics, with the introduction of technologies like smart homes, offices, wearables, remote monitoring, and control. Moreover, OEMs and designers consider miniaturization a primary focus while creating wearable technologies.

- Another advancement that demands miniaturized electronic components is portable electronic equipment, which requires smaller and thinner semiconductor systems for saving space and miniaturization. Due to highly integrated, high-speed applications like aerospace and electric vehicles, the demand for improved electrical performance to minimize noise effects is also evident. As a result of these considerations when designing end products, logic IC components are becoming increasingly important in developing advanced electronic systems.

- Logic ICs are expected to perform a wide range of complex functions. The demand for more state-of-the-art features and capabilities in electronic devices grows as technology advances. Designers need to incorporate complex logic circuits and algorithms to meet these requirements. This increased functionality leads to larger and more intricate designs, making it challenging to manage and optimize the complex interactions between different components.

- The market has undergone substantial changes due to the COVID-19 pandemic, impacting customer behavior, business revenues, and various aspects of corporate operations. The pandemic revealed previously unnoticed risks on the supply side, potentially resulting in shortages of essential parts and components. Consequently, semiconductor companies are proactively restructuring their supply chains to enhance resilience, and these adjustments may persist in the post-pandemic era.

Logic IC (Integrated Circuit) Market Trends

The Automotive Segment to Witness Rapid Growth

- Logic ICs are essential in vehicle control and communications systems. They are used in engine control units (ECUs), transmission control units (TCUs), antilock braking systems infotainment, airbag control modules, systems, and various other electronic control units. ICs can process and execute sophisticated algorithms and logical functions for vehicle control, monitoring, and communication.

- Consumers expect vehicles to offer advanced features, convenience, and a seamless user experience, including comfort, safety, and convenience, such as advanced driver assistance, intelligent lighting systems, personalized settings, and voice control. Meeting consumer expectations and providing innovative features drive the demand for logic ICs in the automotive industry.

- Various ADAS technologies, such as automatic emergency braking, lane departure warning, and adaptive cruise control, are becoming more prevalent in modern vehicles. Logic ICs are critical in processing sensor data, enabling real-time decision-making, and controlling vehicle functions. Future trends may involve the development of more advanced ADAS features, requiring logic ICs with higher computational power, low latency, and enhanced sensor fusion capabilities.

- In the automotive industry, safety and functional requirements are of great importance. Logic ICs ensure various automotive systems' safe and reliable operation, including ADAS, autonomous driving, and powertrain control. The need for high-performance, reliable logic ICs that meet stringent safety standards, such as ISO 26262, drives the demand in the automotive market.

- The pursuit of autonomous vehicles is a significant trend in the automotive industry. Logic ICs are essential for the complex processing and decision-making required for autonomous driving.

- According to Roland Berger, in 2025, the penetration rate of level 4 light autonomous vehicles is expected to be 1%, with a gradually increasing market share in subsequent years. Furthermore, 5% of the global market is anticipated to comprise level 4 light autonomous vehicles by 2030. As self-driving technology advances, logic ICs with increased processing power, advanced sensor integration, and robust safety features are likely to be in demand.

- Moreover, due to environmental concerns and government regulations, the shift toward the use of electric vehicles is gaining momentum. EVs are based on advanced power electronics and battery management, which requires specialized logic ICs to ensure optimum energy use, motor control, or charging infrastructure integration.

- According to the latest report from IEA, over 10 million electric vehicles were bought worldwide in 2022, and sales were estimated to increase by 35% in 2023 to reach 14 million. In 2023, China, Europe, the United States, and other regions sold 13.9 million electric vehicles.

Asia-Pacific to Register Major Growth

- Asia-Pacific consists of the analysis of only China and Japan. The region is a dynamic and rapidly growing segment of the global semiconductor industry. With emerging economies, strong manufacturing capabilities, and growing demand for electronic devices, Asia-Pacific is pivotal in driving innovation, production, and consumption of logic ICs.

- Asia-Pacific is a global manufacturing hub for semiconductor production, with countries such as China and Japan leading in semiconductor manufacturing and assembly. The presence of leading semiconductor foundries, assembly and testing facilities, and electronics manufacturing services enables efficient and cost-effective production of logic ICs. It is home to a vast and rapidly expanding consumer electronics market and automotive market with developments in ADAS and EVs along with increasing industrialization and automation.

- China is known as a global leader in the automotive and mobility industry owing to the consistent performance of the domestic market and its enormous potential. The Chinese Ministry of Industry and Information Technology projects that domestic vehicle production will reach 35 million by 2025, further strengthening its position as the world's leading car manufacturer. According to CAAM, China's new energy vehicle sales amounted to 846,000 units, 808,000 of which were passenger EVs and 39,000 were commercial electric vehicles during August 2023. Sales of BEVs and PHEVs recorded 559,000 and 248,000 vehicles, respectively.

- Furthermore, according to the forecast from China's automotive logistics market, it is expected that the battery electric vehicles (BEV) in the new energy passenger vehicle category will have 84% of the market share by 2025, which leads to major technological advancements in the segment like integration of ADAS in BEVs. In 2024, China is likely to achieve a threshold in adopting intelligent driving systems. The replacement cycle of vehicles could be shortened by more rapid adoption of AD levels than anticipated. An increase in supply may be accompanied by intensive consumer education and media exposure, which will accelerate Chinese consumers' shift toward smart driving.

- The rapid growth of EV markets in Asia-Pacific is expected to impact the logic integrated circuit (IC) market significantly. As EVs incorporate more advanced technologies like ADAS and intelligent driving systems, the demand for ICs, especially those for processing and control systems, will likely surge. Additionally, the shift toward EVs necessitates developing charging infrastructure, which relies heavily on IC technology. As a result, semiconductor companies specializing in logic ICs are poised to benefit from the expanding EV markets across the region.

Logic IC (Integrated Circuit) Market Overview

The logic IC market is fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are STMicroelectronics NV, Renesas Electronics Corp., Analog Devices Inc., Broadcom Inc., and Diodes Incorporated. The various players in the market are adopting different strategies, such as acquisitions and partnerships, to enhance their product offerings and gain a sustainable competitive advantage.

- In April 2024, a long-term agreement was signed between Centrica Energy and STMicroelectronics for the supply of electricity produced from renewable sources in Italy. It is a 10-year contract for energy produced by a new solar farm in Italy.

- In April 2024, Renesas started the operation of Kofu Factory, a dedicated wafer fab. It is located in Kai City, Yamanashi Prefecture, Japan. The Kofu Factory previously operated both 150 mm and 200 mm wafer fabrication lines under Renesas Semiconductor Manufacturing Co., a subsidiary of Renesas.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain/Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Analysis of Macroeconomic Trends on the Market

- 4.5 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Focus on Device Integration

- 5.1.2 Increasing Capital Expenditure of Fabs to Augment Production Capacity

- 5.2 Market Restraints

- 5.2.1 Complexity Associated with Logic IC Design

6 MARKET SEGMENTATION

- 6.1 By IC Type

- 6.1.1 Digital Bipolar

- 6.1.2 By MOS Logic

- 6.1.2.1 MOS General Purpose

- 6.1.2.2 MOS Gate Arrays

- 6.1.2.3 MOS Drivers/Controllers

- 6.1.2.4 MOS Standard Cells

- 6.1.2.5 MOS Special Purpose

- 6.2 By Application

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive

- 6.2.3 IT and Communication

- 6.2.4 Computer

- 6.2.5 Other Applications

- 6.3 By Geography

- 6.3.1 Americas

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 STMicroelectronics NV

- 7.1.2 Renesas Electronics Corp.

- 7.1.3 Analog Devices Inc.

- 7.1.4 Broadcom Inc.

- 7.1.5 Diodes Incorporated

- 7.1.6 NXP Semiconductors NV

- 7.1.7 ON Semiconductor Corporation

- 7.1.8 Texas Instruments Inc.

- 7.1.9 Intel Corporation

- 7.1.10 Toshiba Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET