PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690744

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690744

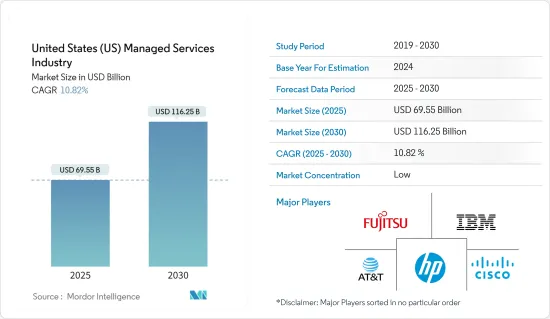

United States (US) Managed Services Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The United States Managed Services Industry is expected to grow from USD 69.55 billion in 2025 to USD 116.25 billion by 2030, at a CAGR of 10.82% during the forecast period (2025-2030).

Key Highlights

- Managed services comprise outsourcing specific IT functions or processes to third-party providers, aiming to streamline operations and reduce costs. This approach enhances service quality, operational efficiency, and customer satisfaction while lowering expenses.

- Market research indicates that the soaring number of Internet of Things (IoT) devices has heightened the demand for managed IoT services, emphasizing the need to secure, monitor, and optimize these connected devices. In response, IT infrastructure providers are collaborating on IoT solutions.

- Hybrid IT combines on-premise infrastructure with cloud-based solutions. The rise of the Internet of Things (IoT) has prompted organizations to rethink their customer engagement strategies. Managed service providers (MSPs) play a crucial role in bolstering security within the IoT ecosystem, ensuring robust protection.

- Relatively speaking, managed services are known to be cost-effective and efficient, as compared to in-house services in the US, as they enable organizations to focus on their core competencies while outsourcing the non-core areas.In the US managed services market outlook, the integration of diverse technologies and adherence to industry regulations often pose challenges. Companies must navigate a web of standards and legal requirements, impacting the implementation and operation of managed services.

- The initial days of the COVID-19 pandemic and subsequent lockdowns caused a temporary dip in demand as businesses focused on survival and delayed non-essential investments. This led to a delay in implementing managed services contracts. However, the surge in remote work highlighted the need for security, cloud migration, collaboration tools, and networking, creating opportunities for industry growth among Managed Service Providers (MSPs).

United States (US) Managed Services Industry Trends

Cloud to Witness Significant Market Growth

- Cloud-based managed services offer flexibility and scalability, empowering service providers to remotely access, monitor, and resolve issues within the cloud environment. Furthermore, market data shows that the adoption of technologies like AI/ML, big data analytics, threat intelligence, and advanced automation platforms is propelling this transition to cloud-based services. Market players are launching innovative and collaborative services in response to industry trends.

- For example, in November 2023, SonicWall, a global cybersecurity provider, acquired Solutions Granted Inc. (SGI), a Managed Security Service Provider (MSSP) catering to hundreds of Managed Service Providers (MSPs). This acquisition bolsters SonicWall's commitment to its partners. It expands its portfolio to include US-based Security Operations Center services (SOCaaS), Managed Detection and Response (MDR), and other tailored managed services for MSPs and MSSPs.

- The IT and Telecom sector holds a significant market share in the cloud-managed services industry. For the 2023 fiscal year, the US federal government allocated around USD 24.4 billion for major federal IT investments, where cloud-managed services are gaining traction in the United States due to their ability to streamline IT operations, bolster security, and offer scalable solutions, thereby reflecting a steady market growth rate.

- These services facilitate remote management and maintenance of cloud infrastructure, which enables businesses to focus on their core objectives while leveraging external expertise, thereby fostering industry growth. The demand for managed services is set to rise as cloud adoption continues to surge, fostering innovation and efficiency in the digital realm.

IT and Telecom to be the Largest End-user Vertical

- The telecom industry in the United States has a strong demand for managed security services and is identified as one of the major significant industry trends. This is primarily due to the telecom companies' handling of vast volumes of sensitive data, including customer information and network infrastructure details, making them prime targets for cyberattacks. Additionally, the complexity of telecom networks and the evolving nature of cyber threats necessitate specialized expertise for effective protection.

- With the advent of 5G networks, the focus has shifted to ensuring end users' security and quality experiences, a shift highlighted in the industry overview of telecom-managed services. According to VIAVISION, as of April 2023, 5G network access was available in 503 United States cities, the most of any country globally, and this requires a significant shift in managing and optimizing networks, moving away from the traditional technology-centric approach. As a result, there is a rising demand for telecom-managed services to aid in this transition, contributing to market growth.

- In July 2023, Dataprise, a leading provider of managed IT, cybersecurity, and cloud solutions, acquired RevelSec, a Texas-based security managed service provider. This acquisition expands Dataprise's national presence and enhances its vertical expertise while providing RevelSec clients access to a broader range of services from Dataprise.

- According to the market report, managed infrastructure holds a significant market share, driven by innovations like IoT, AI, and edge computing, which necessitate advanced network infrastructure. Managed services play an important role in facilitating the adoption of these technologies.

United States (US) Managed Services Industry Overview

The United States managed services market overview is fragmented and is dominated by largest companies, such as Fujitsu Limited, Cisco Systems Inc., IBM Corporation, AT&T Inc., and HP Inc., among other companies that have a strong client base in the market. These players are constantly providing increased and enhanced offerings. Companies are employing powerful competitive strategies in order to survive in the market and retain their clients, thereby intensifying competitive rivalry in the market.

- February 2024 - Ubiquity partnered with Fujitsu to augment Last-Mile Digital Infrastructure Resilience. Ubiquity would utilize the Fujitsu Network Operations Center to support last-mile fiber broadband infrastructure in four major US markets. Fujitsu delivers Ubiquity with 24x7 managed network services from their carrier-class NOC in Texas.

- January 2024 - Cisco, in collaboration with Hitachi Vantara, the subsidiary of Hitachi Ltd specializing in data storage, infrastructure, and hybrid cloud management, unveiled Next-Gen hybrid cloud managed services. These services are specifically tailored to tackle the persistent data management hurdles faced by contemporary businesses. The joint solution, known as Hitachi EverFlex with Cisco Powered Hybrid Cloud, combines automation solutions and predictive analytics. It aims to equip organizations with a forward-looking toolkit for streamlined infrastructure management, cost optimization, and enhanced operational efficiency.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Shift to Hybrid IT

- 5.1.2 Improved Cost and Operational Efficiency

- 5.2 Market Challenges

- 5.2.1 Integration and Regulatory Issues and Reliability Concerns

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Type

- 6.2.1 Managed Data Center

- 6.2.2 Managed Security

- 6.2.3 Managed Communications

- 6.2.4 Managed Network

- 6.2.5 Managed Infrastructure

- 6.2.6 Managed Mobility

- 6.3 By Enterprise Size

- 6.3.1 Small and Medium Enterprises

- 6.3.2 Large Enterprises

- 6.4 By End-user Vertical

- 6.4.1 BFSI

- 6.4.2 IT and Telecom

- 6.4.3 Healthcare

- 6.4.4 Entertainment and Media

- 6.4.5 Retail

- 6.4.6 Manufacturing

- 6.4.7 Government

- 6.4.8 Other End-user Verticals

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fujitsu Limited

- 7.1.2 Cisco Systems Inc.

- 7.1.3 IBM Corporation

- 7.1.4 AT&T Inc.

- 7.1.5 HP Inc.

- 7.1.6 Microsoft Corporation

- 7.1.7 Verizon Communications Inc.

- 7.1.8 Dell Technologies Inc.

- 7.1.9 Rackspace Technology Inc.

- 7.1.10 Tata Consultancy Services Limited

- 7.1.11 Citrix Systems Inc.

- 7.1.12 Wipro Limited

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET