PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1537621

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1537621

Industrial Centrifuges - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

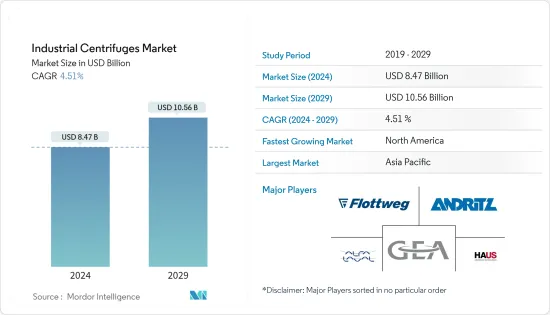

The Industrial Centrifuges Market size is estimated at USD 8.47 billion in 2024, and is expected to reach USD 10.56 billion by 2029, growing at a CAGR of 4.51% during the forecast period (2024-2029).

Over the long term, the growing demand from the chemical industry is expected to stimulate the growth of industrial centrifuges. Increasing investments in the chemical and manufacturing industry are expected to drive the growth of the market.

On the other hand, centrifuges' high capital costs and technical drawbacks are expected to hamper the growth of the market during the forecast period.

However, there is increased demand for energy-efficiency centrifuges in every step of the industrial process, with the growing trend that energy used is both a cost and a long-term environmental issue. Hence, depending on the energy sources and increased customer need for lower energy consumption, technical advancements in centrifuges are expected to create ample opportunities for the market players during the forecast period.

Asia-Pacific will likely dominate the market and is expected to register the highest CAGR during the forecast period. This growth is attributed to the increasing investments and demands from the processed food, pharmaceutical, and wastewater treatment industries.

Industrial Centrifuges Market Trends

The Chemical Industry to Dominate the Market

- In the chemical industry, industrial centrifuges are indispensable tools with many applications that contribute to the efficiency and quality of various processes. One primary application lies in separating chemicals from mixtures, a fundamental process in chemical manufacturing.

- Another critical role of industrial centrifuges in the chemical industry is clarification and purification. They clarify and purify chemical solutions by removing impurities, contaminants, or unwanted particles. Industrial centrifuges aid in refining chemical products by separating different components based on their physical properties, such as molecular weight or particle size.

- Chemical centrifuges' separation technology has also increased with the chemical industry's rapid development. For instance, in March 2023, GEA received an order from the chemical group Albemarle to install centrifuges. The order value for the two centrifuge packages is approximately USD 25.55 million. Specifically, GEA is going to supply four different types of centrifuges: decanter centrifuges, screen screw centrifuges, pusher centrifuges, and peeler centrifuges, and for the processing lines of each refinery.

- The chemical industry plays a significant role in the global economy and supply chain network. According to the American Chemistry Council, in 2022, the chemical industry's total worldwide revenue stood at USD 5.72 trillion. In 2022, the chemical industry revenue reached the highest value in the last 15 years.

- Rising global demand for chemicals across various industries, including pharmaceuticals, agriculture, and manufacturing, is prompting investments in infrastructure to meet increasing production needs. For instance, in September 2023, Sichuan Hebang Biotechnology Co. announced a significant investment of USD 800 million to establish a chemical production facility within the Java Integrated Industrial and Port Estate (JIIPE). Upon completion, the facility is expected to achieve an annual production capacity of 600,000 tons of sodium carbonate and ammonium chloride, with a glyphosate production capacity estimated at 200,000 tons.

- As chemical processing capacities grow, there is a greater need for separation and purification technologies like centrifuges to handle larger volumes of chemicals and ensure product quality and purity. As a result, centrifuge manufacturers stand to benefit from the growing opportunities in the global chemical industry.

- Owing to this factor, the demand for industrial centrifuges in the chemical sector will increase during the forecast period to meet the manufacturing and production quantities of chemicals.

Asia-Pacific to Dominate the Market During the Forecast Period

- Asia-Pacific is one of the fastest growing centrifuges markets, owing to the presence of China, which has one of the highest demands from the chemical and manufacturing, pharmaceutical, and wastewater treatment industries. Additionally, the electricity demand is growing rapidly in South Asian countries like India, Indonesia, and Malaysia due to a surge in population and industrial expansion.

- China is the second largest economy globally and one of the leaders in numerous power, pharmaceutical, chemical, manufacturing, food, and beverage industries. Due to these factors, China accounts for a significant share of the global industrial centrifuges market.

- In terms of GDP, China is the second-largest economy in the world. In 2023, the country's GDP reached USD 17.66 trillion. The growth in the country is gradually diminishing as the aging population, manufacturing to services, and external to internal demand, and the economy is rebalancing from investment to consumption.

- China's National Energy Administration (NEA) is examining the possibility of increasing the ambition of the country's clean energy programs this decade. The NEA proposes that China obtain 40% of its electricity from nuclear and renewable sources by 2030 and set its nuclear capacity target to 120-150 gigawatts by 2030. Such government policies and targets aid the country's development of nuclear power plants in the coming years and are anticipated to provide significant opportunities for the industrial centrifuges market.

- Similarly, India is one of the largest markets for industrial centrifuges in Asia-Pacific, owing to the increasing development activities in various industries.

- India is also investing in its petrochemical business, which is anticipated to create a rising demand for industrial centrifuges. For instance, in April 2024, the Chatterjee Group (TCG) announced plans to partner with local and global companies with its majority-owned petrochemical firm Haldia Petrochemicals Ltd (HPL) to build a more than USD 10 billion project in southern India. The private equity firm plans to make the oil-to-chemical project, capable of producing 3.5 million metric tons per year of ethylene and propylene, at Cuddalore in Tamil Nadu from 2028 to 2029.

- The refinery sector of Asia-Pacific has risen significantly over the last 10 years, and industrial centrifuge is vitally used during the refinery process. According to Statistical Review of World Energy Data, in 2022, the refinery capacity of Asia-Pacific was 36,189 thousand barrels daily, increased by 8.9 % compared to 2013. The number rises significantly during the forecast period, as many projects will start in the coming years.

- Therefore, with increasing demand from various end-user industries in the region, Asia-Pacific will likely be a market leader during the forecast period.

Industrial Centrifuges Industry Overview

The global industrial centrifuges market is moderately fragmented. Some of the major players in the market (in no particular order) include Andritz AG, HAUS Centrifuge Technologies, Alfa Laval AB, GEA Group, and Flottweg SE.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand from Various End-user Industries

- 4.5.2 Restraints

- 4.5.2.1 Higher Capital and Operational Cost

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Sedimentation

- 5.1.1.1 Clarifier/Thickener Centrifuges

- 5.1.1.2 Decanter Centrifuges

- 5.1.1.3 Disc Stack Centrifuges

- 5.1.1.4 Hydrocyclones

- 5.1.1.5 Other Sedimentation Centrifuges

- 5.1.2 Filtering

- 5.1.2.1 Basket Centrifuges

- 5.1.2.2 Scroll Screen Centrifuges

- 5.1.2.3 Peeler Centrifuges

- 5.1.2.4 Pusher Centrifuges

- 5.1.2.5 Other Filtering Centrifuges

- 5.1.1 Sedimentation

- 5.2 Design

- 5.2.1 Horizontal Centrifuges

- 5.2.2 Vertical Centrifuges

- 5.3 Operation Mode

- 5.3.1 Batch

- 5.3.2 Continuous

- 5.4 Industry

- 5.4.1 Food and Beverages

- 5.4.2 Pharmaceutical

- 5.4.3 Water and Wastewater Treatment

- 5.4.4 Chemical

- 5.4.5 Metal and Mining

- 5.4.6 Power

- 5.4.7 Pulp and Paper

- 5.4.8 Other Industries

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 NORDIC

- 5.5.2.8 Turkey

- 5.5.2.9 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Malaysia

- 5.5.3.7 Thailand

- 5.5.3.8 Indonesia

- 5.5.3.9 Vietnam

- 5.5.3.10 Rest of the Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Colombia

- 5.5.4.5 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Qatar

- 5.5.5.4 South Africa

- 5.5.5.5 Nigeria

- 5.5.5.6 Egypt

- 5.5.5.7 Rest of the Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 MSE Hiller

- 6.3.2 Andritz AG

- 6.3.3 Alfa Laval AB

- 6.3.4 GEA Group AG

- 6.3.5 Multotec Pty Ltd

- 6.3.6 Thomas Broadbent & Sons Ltd

- 6.3.7 Flottweg SE

- 6.3.8 Ferrum Ltd

- 6.3.9 HAUS Centrifuge Technologies

- 6.4 Market Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Demand for the Energy-efficient Industry Centrifuges