PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1536978

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1536978

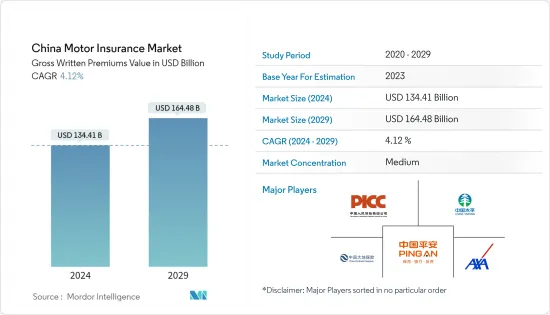

China Motor Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The China Motor Insurance Market size in terms of gross written premiums value is expected to grow from USD 134.41 billion in 2024 to USD 164.48 billion by 2029, at a CAGR of 4.12% during the forecast period (2024-2029).

Motor insurance is the largest non-life insurance segment in China, contributing more than 70% of the total non-life insurance premium. Post pandemic, the market has recovered. The motor insurance market is expanding at a constant pace due to the increasing affordability of consumers, increasing demand for personal mobility solutions, raising disposable income, improved standard of living, and growing middle class. The increasing economic activities in China are increasing the demand for commercial vehicles. The E-commerce industry is growing rapidly all over China, which is increasing the demand for transportation solutions, which in turn is increasing the demand for commercial vehicles all over China. The increasing adoption of personal vehicles and commercial vehicles in China is expected to increase the demand for vehicle insurance in the near future. In addition, the increasing number of road traffic accidents in China increased the demand for vehicle insurance. Vehicle insurance provides financial protection to vehicle owners against the physical damage caused by accidents and auto theft.

Government imposition of mandatory motor liability insurance, significantly boosted motor insurance in China. New regulations were implemented to include more foreign insurance companies in order to increase competitiveness. Although China includes a high e-commerce penetration, motor insurance sales in China are dominated by offline channels. Insurance firms set up selling points in car sales stores, providing an opportunity for the client with a car and insurance at the same place while the commission is provided to the car sales store. The Chinese online sales of motor insurance were less compared to the other countries. Still, within the online segment, the sales of insurance through mobile internet were high compared to other counterparts. It signifies insurance customers in China tend to use mobile to search and buy insurance products.

China Motor Insurance Market Trends

Recovery in Vehicle Sales is Driving Motor Insurance Market

China's vehicle sales increased 12% last year to reach 30.09 million units, surpassing the 3% growth target from the previous year. It was driven by higher global demand, particularly for electric vehicles, as well as fierce competition between automakers who offered discounts and new models. Additionally, there was a renewed appetite for commercial vehicles. China remained the world's largest car market in the current year, with record auto production and sales. Vehicle production and sales in China increased two-digit year-on-year in the current year. The passenger vehicle market continued to grow, with CV volume recovering to four million units.

In comparison, NEWvolume increased to more than nine million units and a market share of more than 30%. With the rising middle-class population in China, the needs and demands of consumers are changing. Sales data from China automobile dealers' association, shows that the new growth engine for the industry is young adults living in developing cities. Meanwhile, tier 2, 3, and 4 towns are developing fast and offer a new generation of young consumers willing and able to afford a car. Moreover, the motor insurance segment is expected to grow as automobile sales improve due to the proposed extension of subsidy for electric vehicles last year.

The Rise of Usage-Based Insurance in China's Motor Insurance Landscape

China, being one of the largest automotive and electrical vehicle markets, holds quite potential for Usage-based motor insurance. Despite a large and mature auto insurance market, the UBI market in China is still in the infancy stage. Numerous enterprises have begun actively delving into the implementation of UBI in both passenger cars and commercial vehicles through the execution of pilot programs. However, the development of UBI pre-pandemic was short-lived due to the absence of precise regulations to support Usage-based insurance products.

In September 2020, the China Banking and Insurance Regulatory Commission (CBIRC) issued the regulation named "Guide on Implementing Comprehensive Reform of Auto Insurance". It was the first time that the authority recognized the UBI in its regulation.

The mature automobile market, favorable regulation from the authorities, and improved digital and data processing capabilities all make China a potential market for UBI.

China Motor Insurance Industry Overview

The Chinese motor insurance market is highly competitive, with major international players. The Chinese motor insurance market presents opportunities for growth during the forecast period, which is expected to drive market competition further. However, the recently reformed government policies welcoming foreign players into the country with 100% ownership might increase the competitiveness among the major players as many global giant insurers are already in the race to capture potential market share in the country. Some of the major players in the market include PICC, Ping An, China Pacific, China Taiping, and China Continent Insurance, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in Internet Penetration and Online Sales

- 4.3 Market Restraints

- 4.3.1 Intense Competition and Regulatory Complexities

- 4.4 Market Oppurtunities

- 4.4.1 Digital Transformation by the Companies

- 4.5 Value Chain Analysis

- 4.6 Industry Attractiveness: Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Insights into Technological Advancements in the Industry

- 4.8 Insights on Various Regulatory Trends Shaping the Market

- 4.9 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Insurance Type

- 5.1.1 Compulsory Auto Liability Insurance

- 5.1.2 Commercial Auto Insurance

- 5.2 By Distribution Channel

- 5.2.1 Direct

- 5.2.2 Agent

- 5.2.3 Online

- 5.2.4 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 PICC

- 6.2.2 Ping An

- 6.2.3 China Pacific

- 6.2.4 China Continent Insurance (CCIC)

- 6.2.5 China Taiping

- 6.2.6 Axa Tianping

- 6.2.7 China United Property Insurance

- 6.2.8 Samsung Property Insurance

- 6.2.9 Huatai Property Insurance

- 6.2.10 Bohai Property Insurance *

7 FUTURE MARKET TRENDS

8 DISCLAIMER AND ABOUT US