PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1536906

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1536906

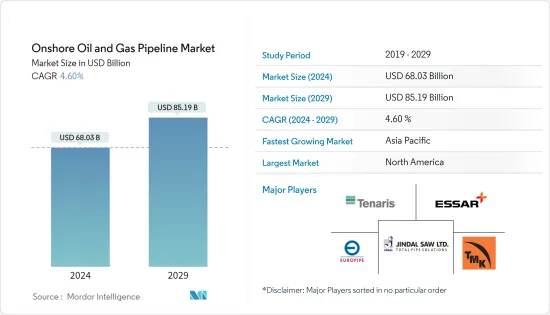

Onshore Oil And Gas Pipeline - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Onshore Oil And Gas Pipeline Market size is estimated at USD 68.03 billion in 2024, and is expected to reach USD 85.19 billion by 2029, growing at a CAGR of 4.60% during the forecast period (2024-2029).

Key Highlights

- Factors such as the availability of abundant natural gas reserves and the lower cost compared to other fossil fuel types are expected to supplement the demand for natural gas from multiple end-users, including power generation. This, in turn, is expected to boost the gas pipeline segment during the forecast period.

- However, the global shift toward renewable sources for electricity generation poses a huge threat to the oil and gas demand, which is likely to be a major challenge for the growth of onshore oil and gas pipeline installations during the forecast period.

- Nevertheless, the rise in onshore exploration and production projects is expected to create excellent opportunities for the market players in the years to come, as these projects are paving the way for the pipeline industry to grow more.

- Asia-Pacific is expected to witness significant growth during the forecast period, with the majority of the demand coming from countries like China, India, etc.

Onshore Oil & Gas Pipeline Market Trends

Natural Gas Pipeline Type to Dominate the Market

* Onshore pipelines are laid in the country's inland areas or a region. Onshore pipelines are of different types: mains, crossings, feeder lines, transmissions, spur lines, and above-ground and underground pipelines.

* The expansion of existing onshore pipeline projects is being done in countries to cater to growing demand. As per the US Energy Information Administration (EIA), about 5.2 billion cubic feet per day (Bcf/d) of natural gas intrastate pipeline capacity was added in the United States of America in 2023. Most of the intrastate pipeline additions were made in Texas and Louisiana to fulfill natural gas demand in the United States Gulf Coast Markets.

* Moreover, the main mileage of gas distribution systems has grown in recent years. As per the United States of Transportation, in 2023, the distribution main mileage stood at 1,367,244 miles, an increase of 1% from the previous year. Considering the increase in the utilization of gas from end-consumers, the gradual growth of main mileage for gas distribution systems is likely to persist soon.

* Likewise, By 2030, owing to factors such as environmental benefits and the quest for energy security in regions such as the Middle East, Africa, and Asia-Pacific, the demand for natural gas is expected to witness significant growth among all fuel types.

* In July 2024, Iran commenced the development of the Iranian Gas Trunk Line-IGAT XI pipeline of 1200 kilometers to fulfill the natural gas demand of its provinces, such as Bushehr, Fars, Yazd, and Isfahan. The project owned by National Iranian Gas Co. is likely to be completed by 2027. Such developments are likely to help the oil and gas pipeline market grow in the forecast period.

* The development of new natural gas sources, such as shale gas deposits, and the resulting price pressure are increasing the international trade of natural gas. Hence, these developments are expected to increase the demand for pipeline network expansion during the forecast period.

Asia-Pacific Expected to Witness Significant Demand

* The energy consumption in Asia-Pacific is expected to increase by up to 48% by 2050. According to the International Energy Agency (IEA), China is expected to contribute 30% of the world's energy increase until 2025. Crude oil and natural gas consumption has witnessed significant growth in the region in recent years, mainly due to increasing demand from emerging economies like India and China.

* As of January 2024, Santos - Australia's oil & gas major, decided to commence the construction of a gas pipeline project worth about USD 4.3 billion that would connect the Barossa gas field to a processing plant in the northern Australian city of Darwin. The project will likely increase natural gas availability in Australia in the future.

* India is also modifying its gas pipeline infrastructure to meet the growing demand. The nation aims to increase the natural gas share to 15% in the energy basket. It expects USD 66 billion investment in building the gas infrastructure, including onshore gas pipeline, CGD, and LNG regasification terminals by 2030. Moreover, in December 2020, the Indian government announced a USD 60 billion investment for creating gas pipeline infrastructure, primarily onshore, which covers expanding Compressed Natural Gas pipeline networks (CGD) in 232 geographical areas across the country by 2024.

* Oil consumption in the Asia-Pacific has witnessed an increasing trend in recent years. As per the Statistical Review of World Energy, oil consumption stood at 1615 million tonnes in 2022, an increase of 0.5 % from the previous year. It is likely to grow more in the forecast period.

* Therefore, significant factors like the increasing demand for crude oil and natural gas and new pipeline infrastructure in the Asia-Pacific are expected to drive growth in the global onshore oil and gas pipeline market.

Onshore Oil And Gas Pipeline Industry Overview

The onshore oil and gas pipeline market is fragmented. Some of the key players in this market include (in no particular order) Tenaris SA, Essar Group, Jindal SAW Ltd, Europipe GmbH, and TMK Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Installed Pipeline Historic Capacity and Forecast in Kilometers, till 2029

- 4.4 Inter-Regional Pipeline Import Capacity in BSCM, till 2029

- 4.5 Inter-Regional Pipeline Export Capacity in BSCM, till 2029

- 4.6 Brent Crude Oil and Henry Hub Spot Prices Forecast, till 2029

- 4.7 Onshore CAPEX Forecast in USD billion, till 2029

- 4.8 Recent Trends and Developments

- 4.9 Government Policies and Regulations

- 4.10 Market Dynamics

- 4.10.1 Drivers

- 4.10.1.1 Availability of abundant natural gas reserves and the lower cost compared to other fossil fuel types

- 4.10.1.2 Growing investments to increase production to fulfill global demand

- 4.10.2 Restraints

- 4.10.2.1 The global shift toward renewable sources for electricity generation

- 4.10.1 Drivers

- 4.11 Supply Chain Analysis

- 4.12 Porter's Five Forces Analysis

- 4.12.1 Bargaining Power of Suppliers

- 4.12.2 Bargaining Power of Consumers

- 4.12.3 Threat of New Entrants

- 4.12.4 Threat of Substitutes Products and Services

- 4.12.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Oil Pipeline

- 5.1.2 Gas Pipeline

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Norway

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Spain

- 5.2.2.5 NORDIC

- 5.2.2.6 Russia

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Indonesia

- 5.2.3.4 Malaysia

- 5.2.3.5 Vietnam

- 5.2.3.6 Thailand

- 5.2.3.7 Rest of Asia Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South Africa

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 South Africa

- 5.2.5.4 Egypt

- 5.2.5.5 Nigeria

- 5.2.5.6 Qatar

- 5.2.5.7 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Essar Group

- 6.3.2 Jindal SAW Ltd

- 6.3.3 Tenaris SA

- 6.3.4 Europipe GmbH

- 6.3.5 CPW America Co.

- 6.3.6 TMK Group

- 6.3.7 Baoshan Iron & Steel Co. Ltd

- 6.3.8 TC Energy Corporation

- 6.3.9 WorleyParsons Limited

- 6.3.10 Mastec Inc.

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS