PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1536833

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1536833

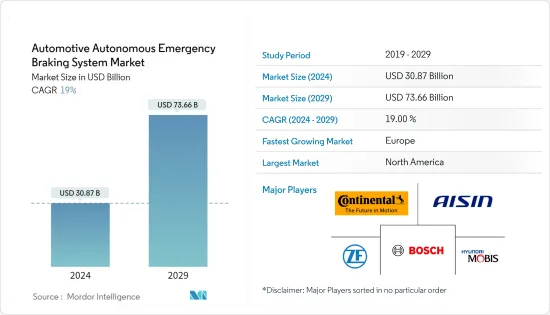

Automotive Autonomous Emergency Braking System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Automotive Autonomous Emergency Braking System Market size is estimated at USD 30.87 billion in 2024, and is expected to reach USD 73.66 billion by 2029, growing at a CAGR of 19% during the forecast period (2024-2029).

Over the medium term, increasing awareness about safety among consumers and authorities has led to significant developments in the automotive automated emergency brake system, resulting in improved security and reduced accidents on the road. With further technological advancements, the market is expected to see even safer and more reliable brake systems.

Factors such as individual vehicle manufacturers incorporating advanced braking systems in their vehicles to improve braking efficiency and industry players offering a wide range of products are further expected to drive market growth during the forecast period.

Annually, around 1.25 million people are killed in road accidents, with the highest numbers being registered in developing countries. Many governments worldwide have started imposing stringent regulations to curb the rising number of road accidents.

Major OEMs have started increasingly investing in R&D efforts to develop advanced technologies. Increasing concerns regarding vehicle safety, the growing adoption of advanced braking systems, the emergence of advanced AI-powered systems, and an increase in government vehicle safety norms, combined with a rise in vehicle production worldwide, are expected to propel the automotive autonomous emergency braking system market during the forecast period.

Many original equipment manufacturers are equipping AEB systems in most of their medium and luxury car ranges. This is resulting in the increasing production of autonomous vehicles. During the forecast period, the production of such vehicles is expected to record a CAGR of over 21%.

Automotive Autonomous Emergency Braking System Market Trends

Passenger Cars Hold Major Market Share

The rise in demand for advanced safety features in vehicles and the increase in passenger car sales across major regions worldwide are likely to result in major growth for the market over the coming years.

Automatic emergency braking is an advanced safety technology system that autonomously slows or completely stops a vehicle in order to prevent an accident if the driver fails to respond. As with other advanced driver assistance technologies, automatic emergency braking is not 100% foolproof.

To cater to this growing demand, several automakers are launching new vehicle models with these technologies. Tesla is already offering AEB features as standard across all its cars, while other automakers like Daimler, BMW, and Ford are expected to provide AEB in all their upcoming models. Tesla's cars are equipped with all the necessary hardware to achieve full autonomy. For instance,

* In November 2023, Renault introduced the Dacia Duster SUV in France. The new SUV offers a 4x4 Terrain Control transmission with five driving modes and an automatic emergency braking system.

* In November 2023, Toyota Motor Corporation introduced the Crown Signia mid-size crossover SUV in the North American market. The new SUV is equipped with an automatic emergency braking system.

The growing interest among vehicle owners worldwide in autonomous emergency braking systems is driving the global market. This demand has also been fueled by a rising number of road accidents. Governments worldwide are encouraging the development of several kinds of safety features in order to avoid road accidents.

Rising disposable incomes and customer preferences increasingly transitioning toward cars with fully loaded safety features are driving the market. The passenger cars segment is expected to lead the market during the forecast period.

As per research by EURO NCAP, 75% of all collisions in urban driving environments occur at speeds below 25 mph, with AEB having led to a 38% reduction in rear-end crashes. Autonomous vehicle technology offered with level 4 and 5 autonomous cars may become a large market worldwide over the coming years.

In line with the abovementioned developments globally, the demand for automatic emergency braking systems in passenger cars will be high over the coming years.

North America Expected to Lead the Market

Autonomous braking is provided with 51% of the model lines offered by OEMs across the United States. Tesla and Volvo offer AEB as a standard feature in 100% of their vehicles.

The US Department of Transportation's National Highway Traffic Safety Administration (NHTSA) recently issued a notice of proposed regulations that would require automatic emergency braking and pedestrian AEB systems for passenger vehicles and light trucks.

The proposed rule is expected to dramatically reduce pedestrian-related accidents and rear-end collisions. The NHTSA estimates that this proposed rule, if finalized, would save at least 360 lives per year and reduce the number of injuries by at least 24,000 annually.

In addition, these AEB systems would lead to a significant reduction in property damage caused by rear-end collisions. Many accidents could be avoided entirely, while others would be less destructive.

The Department's other road safety actions include the preparation of the Vulnerable Road User Safety Assessment to assist states with the required assessments for 2023. The safety performance of the state in terms of vulnerable road users and its plan to improve their safety are among the parameters assessed.

In line with growing technological advancements, OEMs must remain active in achieving their AEB commitments or face the possibility of brand erosion due to falling behind other market players in safety advances. In particular, the incorporation of AEB into the US government's safety ratings may alter consumer perception.

Based on the aforementioned developments, the market is expected to witness high growth in the upcoming period.

Automotive Autonomous Emergency Braking System Industry Overview

The automotive autonomous emergency braking system market is dominated by several key players, such as Robert Bosch GmbH, Continental AG, ZF Friendrichagen AG, Hyundai Mobis, and Hitachi Automotive System Ltd. Key players continue to gain a competitive edge in the global market by engaging in strategic approaches. Consistent advancements and innovations in braking systems have assisted manufacturers in gaining traction in the competitive market. For instance,

* In July 2023, ZF Friedrichshafen AG and Volta Trucks signed a long-term agreement for the integration of components and parts in the all-electric Volta Zero electric truck. ZF provided the OnGuardACTIVE advanced emergency braking system, the electronic braking system including the brake pedal box, the ESCsmart electronic stability control, and the OnHand electro-pneumatic handbrake.

* In June 2023, the US National Highway Transportation Safety Administration (NHTSA) announced that heavy trucks and buses must include automatic emergency braking equipment (AEB) within five years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rise in Demand for Safety Features in Vehicles

- 4.2 Market Restraints

- 4.2.1 High Costs Associated with the System

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.2 By Technology

- 5.2.1 LiDar

- 5.2.2 Radar

- 5.2.3 Camera

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Mergers and Acquisitions

- 6.3 Company Profiles*

- 6.3.1 Robert Bosch GmbH

- 6.3.2 WABCO Holdings Inc.

- 6.3.3 Hyundai Mobis Co. Ltd

- 6.3.4 Denso Corporation

- 6.3.5 ZF Friedrichshafen AG

- 6.3.6 Continental AG

- 6.3.7 Autoliv Inc.

- 6.3.8 Valeo SA

- 6.3.9 Aisin Corporation

- 6.3.10 Delphi Automotive PLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS