PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852167

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852167

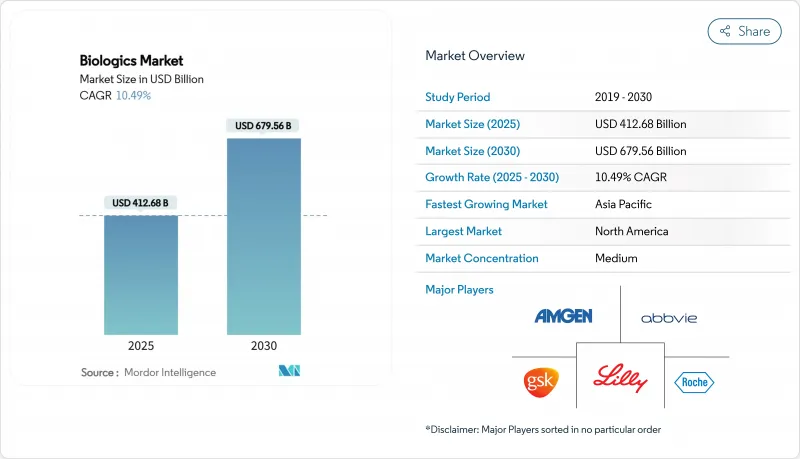

Biologics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The biologics market size reached USD 412.68 billion in 2025 and is projected to advance to USD 679.56 billion by 2030, reflecting a 10.49% CAGR over the forecast period.

Strong demand for precision oncology agents, next-generation monoclonal antibodies, and gene-based therapeutics steers this expansion. Heightened chronic disease prevalence, accelerated regulatory designations, and sustained venture funding continue to move these complex therapies from research pipelines into routine care. Manufacturing investment exceeding USD 15 billion since 2024 builds new capacity in North Carolina, Denmark, and Germany, positioning producers to ease recent supply bottlenecks. At the same time, innovators adopt continuous perfusion and single-use bioreactors to combine speed with lower upfront costs, while payers increasingly embrace biosimilars to contain spending.

Global Biologics Market Trends and Insights

Rising Global Chronic Disease Burden

Cancer, autoimmune disorders, and metabolic diseases present complex pathways that small-molecule drugs no longer address fully. Oncology uses of biologics command 36.54% share and post a 13.78% CAGR as immunotherapies move into earlier treatment lines. Rheumatoid arthritis patients treated with novel B-cell depletion antibodies report 87% flare reduction, illustrating superior clinical control. GLP-1 agonists for diabetes and obesity have outstripped supply, prompting Novo Nordisk to commit USD 4.1 billion to new fill-finish space. Rare disease therapies enjoy orphan incentives that allow premium pricing, creating many small but profitable niches.

Accelerated Regulatory Approvals and Designations

The FDA's streamlined interchangeability guidance lets biosimilar developers bypass switching studies if analytical sameness is proven. RMAT and breakthrough labels shortened timelines for seven cell and gene therapies cleared in 2024, including lifileucel for melanoma and fidanacogene elaparvovec for hemophilia B. EMA alignment with U.S. policy now delivers simultaneous trans-Atlantic launches, trimming duplication costs. China's National Medical Products Administration has overhauled its process, enabling Akeso to bring ivonescimab forward with data that outperforms global standards.

High Manufacturing and Development Costs

A single biologics plant demands capital above USD 1 billion, as illustrated by Novo Nordisk's Clayton expansion and Eli Lilly's USD 3 billion Wisconsin site. Although single-use systems reduced build time, frequent bag changeovers and specialized media lift operating expense. End-to-end programs span 10-15 years and can cost USD 300 million in trials alone, limiting small biotech participation. Supply bottlenecks in CHO media, resins, and sterile syringes inflate costs and threaten scheduling. Any deviation during scale-up risks product integrity, making rigorous process validation essential and expensive.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Biosimilar Adoption Globally

- Continuous Innovation in Biologic Modalities

- Complex Regulatory and Quality Compliance Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Monoclonal antibodies contributed USD 274.4 billion, equal to 66.43% of the biologics market size in 2024, benefiting from decades of manufacturing refinement. The class spans oncology, autoimmune, and inflammatory uses, and its predictable pharmacology supports broad payer acceptance. In contrast, gene-based biologics post a 12.32% CAGR through 2030, propelled by first-in-class approvals for hemophilia and inherited retinal diseases. Vaccines remain a steady pillar as governments fund pandemic readiness, while recombinant proteins face downward price pressure from mature biosimilars.

Pipeline investment tilts toward cell-based modalities, evidenced by seven fresh FDA approvals in 2024 that validated allogeneic CAR-T and stem cell products. ADCs and multispecific antibodies broaden precision oncology by fusing targeting domains with cytotoxic or immune-modulatory payloads. Over 250 protein-engineering programs now optimize half-life, tissue penetration, and immunogenicity profiles. These shifts collectively raise the biologics market value proposition and expand therapeutic range, underwriting sustained double-digit growth.

Oncology accounted for 36.54% of the biologics market size in 2024 and will rise at a 13.78% CAGR, mirroring rapid uptake of checkpoint inhibitors, ADCs, and CAR-T therapies. Autoimmune conditions follow, as next-generation bispecific antibodies demonstrate superior disease control relative to TNF inhibitors. Infectious disease biologics develop beyond prophylactic vaccines into post-exposure therapeutics against viral and bacterial threats.

Metabolic and endocrine disorders add scale as GLP-1 agonists extend indications to chronic weight management, triggering worldwide capacity projects valued above USD 15 billion. Ophthalmology stands to gain from gene therapy that delivers durable benefit after a single administration. Rare disease pipelines, spurred by orphan incentives, deepen the addressable patient pool. Collectively, diversified applications reinforce resilience in the biologics market even if one therapeutic area softens.

The Biologics Market Report is Segmented by Product (Monoclonal Antibodies, Vaccines, and More), Application (Oncology, Autoimmune & Inflammatory, and More), Source (Mammalian Cell-Culture, and More), Manufacturing Technology (Single-Use Bioreactors, and More), End-User (Pharmaceutical & Biotech Companies, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America sustained leadership with 40.54% biologics market share in 2024, buoyed by robust reimbursement, venture capital depth, and an FDA that expedites breakthrough designations. The region channels more than USD 15 billion into new capacity, transforming the Research Triangle into a global hub anchored by Novo Nordisk, Eli Lilly, and Amgen. Although growth moderates to 9.8% CAGR as penetration matures, competitive intensity rises as biosimilars take hold.

Asia-Pacific delivers the quickest 11.54% CAGR as China, Japan, and India refine regulatory pathways and invest in biomanufacturing. China's streamlined approval timeline allows domestic players to launch innovative oncology biologics that challenge Western incumbents. Japan leverages tax incentives and public funding to support translational research, while South Korea's Samsung Biologics exports CDMO capacity globally. India capitalizes on low-cost talent for biosimilar and early-phase projects, further enlarging the region's footprint.

Europe maintains steady 9.2% CAGR on the back of mature biosimilar frameworks and high public health spending. Germany and Switzerland host high-value production for complex antibodies, whereas Ireland and Denmark entice multinational expansions via favorable corporate tax regimes. Aging demographics and chronic disease prevalence sustain underlying demand, and pan-EU harmonization of regulatory guidance reduces market entry friction.

- Abbvie

- Amgen

- Eli Lilly and Company

- Roche

- GlaxoSmithKline

- Johnson & Johnson

- Merck

- Pfizer

- Sanofi

- Bristol-Myers Squibb

- AstraZeneca

- Novartis

- Gilead Sciences

- Biogen

- Regeneron Pharmaceuticals

- Lonza Group

- Samsung Group

- Celltrion

- Takeda Pharmaceutical Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Chronic Disease Burden

- 4.2.2 Accelerated Regulatory Approvals and Designations

- 4.2.3 Expansion of Biosimilar Adoption Globally

- 4.2.4 Continuous Innovation in Biologic Modalities

- 4.2.5 Growth in Outsourced Manufacturing Capacity

- 4.2.6 Increasing Healthcare Expenditure in Emerging Markets

- 4.3 Market Restraints

- 4.3.1 High Manufacturing and Development Costs

- 4.3.2 Complex Regulatory and Quality Compliance Requirements

- 4.3.3 Supply Chain Constraints for Critical Raw Materials

- 4.3.4 Intensifying Environmental Sustainability Scrutiny

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Monoclonal Antibodies

- 5.1.2 Vaccines

- 5.1.3 Recombinant Proteins/Hormones

- 5.1.4 Cellular-based Biologics

- 5.1.5 Gene-based Biologics

- 5.1.6 Multispecific & ADCs

- 5.1.7 Other Products

- 5.2 By Application

- 5.2.1 Oncology

- 5.2.2 Autoimmune & Inflammatory

- 5.2.3 Infectious Diseases

- 5.2.4 Metabolic & Endocrine

- 5.2.5 Ophthalmology

- 5.2.6 Rare & Genetic Disorders

- 5.2.7 Other Applications

- 5.3 By Source

- 5.3.1 Mammalian Cell-Culture

- 5.3.2 Microbial Expression

- 5.3.3 Plant-based & Insect-cell Systems

- 5.4 By Manufacturing Technology

- 5.4.1 Single-use Bioreactors

- 5.4.2 Stainless-steel Fed-Batch Systems

- 5.4.3 Continuous Perfusion Platforms

- 5.5 By End-user

- 5.5.1 Pharmaceutical & Biotech Companies

- 5.5.2 Contract Development & Manufacturing Organizations (CDMOs)

- 5.5.3 Hospitals & Specialty Clinics

- 5.5.4 Academic & Research Institutes

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Amgen Inc.

- 6.3.3 Eli Lilly and Company

- 6.3.4 F. Hoffmann-La Roche AG

- 6.3.5 GlaxoSmithKline plc

- 6.3.6 Johnson & Johnson

- 6.3.7 Merck & Co., Inc.

- 6.3.8 Pfizer Inc.

- 6.3.9 Sanofi SA

- 6.3.10 Bristol Myers Squibb

- 6.3.11 AstraZeneca plc

- 6.3.12 Novartis AG

- 6.3.13 Gilead Sciences Inc.

- 6.3.14 Biogen Inc.

- 6.3.15 Regeneron Pharmaceuticals

- 6.3.16 Lonza Group AG

- 6.3.17 Samsung Biologics

- 6.3.18 Celltrion Inc.

- 6.3.19 Takeda Pharmaceutical Co.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment