PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1640539

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1640539

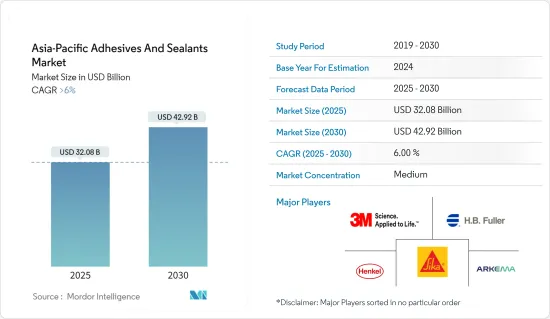

Asia-Pacific Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Asia-Pacific Adhesives And Sealants Market size is estimated at USD 32.08 billion in 2025, and is expected to reach USD 42.92 billion by 2030, at a CAGR of greater than 6% during the forecast period (2025-2030).

The region was negatively affected by the COVID-19 pandemic. The adhesives and sealants market in the region also faced a similar situation. However, the market has now reached pre-pandemic levels, and it is expected to grow at a significant pace.

Expanding packaging and building and construction industries around the globe are likely to drive demand for adhesives and sealants during the forecast period.

However, strict environmental regulations set by the government on the use of volatile organic compounds are anticipated to hamper market expansion.

The innovation and development of bio-based adhesives and shifting focus toward adhesive bonding for composite materials are likely to offer opportunities for the adhesives and sealants market.

China stands to be the largest market for adhesives and sealants in the region, where the consumption is driven by the end-user industries, such as automotive, construction, electronics, and packaging.

APAC Sealants & Adhesives Market Trends

Packaging Segment to Dominate the Market

- Packaging products in paper packaging comprises folding cartons, corrugated boxes, paper bags, and liquid paperboard. With the considerable increase in organized retail, the demand for paper packaging is anticipated to increase due to the rapid increase in supermarkets and modern shopping centers.

- An extremely high proportion of industrial products are sold in packages, either due to stability requirements for storage and transport or aesthetic reasons. Most packaging materials presently used are different materials laminated together, which require the use of adhesives.

- One of the critical factors that have been accelerating the growth of the segment includes a growing e-commerce platform and increasing consumption with the rise in income levels of the masses.

- China is a major contributing country in the APAC region for the packaging industry. In a 2021-2025 "five-year plan," China announced it would improve its plastic recycling and incineration capacities, promote "green" plastic products, and combat the misuse of plastic in packaging and agriculture. The new five-year plan would push merchants and delivery companies to reduce "unreasonable" plastic wrapping and increase garbage incineration rates in cities to about 800,000 tons per day by 2025, up from 580,000 tons last year. Such developments are expected to increase the country's demand for recyclable flexible plastic packaging. Over the projection period, the rise of e-commerce giants like Alibaba is expected to fuel the packaging market. For example, Chinese shoppers received approximately 1.9 billion shipments during Alibaba's Double 11 shopping event, which lasted 10 days.

- In India, plastic packaging is growing at a significant rate of 20-25% annually and has reached 6.8 million tons, whereas paper packaging is valued at 7.6 million tons. These trends positively impacted the consumption of adhesives in the packaging sector.

- In June 2022, the Central Pollution Control Board (CPCB), a federal agency under the Ministry of the Environment, released a list of steps to outlaw specific single-use plastic products by June 2022. Such measures are anticipated to drive the demand for paper packaging in the country.

- Moreover, in a country such as India, the growing demand for online food ordering is increasing, pushing the usage of packaged food boxes in the food packaging market. For instance, in February 2022, Zomato, one of the prominent food delivery companies, said that the average monthly active food delivery restaurants have grown by 6x, and average monthly transacting customers have grown by 13x on Zomato over the past five years.

- Online retail shopping is increasing at a higher rate with the rising internet technologies and web applications, which have primarily supported the packaging industry's growth.

- According to the British Chamber of Commerce in Korea, South Korea's F&B business is defined by hypermarket dominance and expanding sales through e-commerce platforms. The F&B market in South Korea is expected to reach GBP 76.1 billion (USD 89.98 billion) by 2024.

- Furthermore, the government initiatives for sustainable packaging are mandating the adoption of paper packaging products. For instance, as part of South Korea's 2050 carbon neutrality goal, the South Korean Ministry of Environment has announced that disposable cups from chain cafes and fast-food restaurants will require a 300 KRW (USD 0.25) deposit starting on June 10, 2022. This regulation applies to chains with more than 100 branches and 38,000 stores.

- Therefore, with extensive application in the paper, board, and packaging industry and increased demand for packaging materials mainly due to the growing e-commerce industry, the consumption of adhesives and sealants in this segment is expected to increase further in the region over the forecast period.

China to Dominate in the Asia-Pacific Region

- China dominates the region's consumption of adhesives and sealants. Growing construction activities, increasing consumption in the packaging industry, and electronics production to support demand in the international market are some of the key factors driving the consumption of the adhesives and sealants market in the country.

- China's growth is fueled mainly by rapid expansion in the residential and commercial building sectors and the country's expanding economy. China is encouraging and enduring a continuous urbanization process, with a projected rate of 70% by 2030. As a result, increased building activity in nations like China is projected to fuel the region's adhesive industry. All such factors tend to increase the demand for adhesives across the region.

- According to the National Bureau of Statistics of China, the value of construction output accounted for CNY 31.2 trillion (USD 4.5 trillion) in 2022, up from CNY 29.31 trillion (USD 4.2 trillion) in 2021. Moreover, as per the forecast given by the Ministry of Housing and Urban-Rural Development, China's construction sector is expected to maintain a 6% share of the country's GDP going into 2025.

- China's passenger electric vehicle (EV) market continues to grow at an impressive rate, with EV sales rising by 87% YoY in 2022. BYD, Wuling, Chery, Changan, and GAC are some of the top Chinese brands that dominate the EV market, with local brands commanding 81%. Additionally, in 2022, BYD increased its market share by over 11% Y-o-Y, with six out of the top 10 EV models in the Chinese market coming from the brand.

- Moreover, the Chinese government estimates a 20% penetration rate of electric vehicle production by 2025. Hence, this is anticipated to increase the production and consumption of vehicle batteries, thus increasing demand for adhesives and sealants in the market.

- Furthermore, China has one of the world's largest electronics production bases and offers tough competition to the existing upstream producers, such as South Korea, Singapore, and Taiwan. Electronic products, such as smartphones, OLED TVs, and tablets, have the highest growth rates in the consumer electronics segment of the market in terms of demand.

- In China, electronics production is projected to grow with the rising demand for electronic products in countries importing electronic products from China and the increase in the disposable income of the middle-class population.

- Hence, all such trends in the end-user industries are expected to drive the growth of the adhesives and sealants market in the country over the forecast period.

APAC Sealants & Adhesives Industry Overview

The Asia-Pacific adhesives and sealants market is partially consolidated in nature. The major players (not in any particular order) include 3M, Arkema, Sika AG, H.B. Fuller Company, and Henkel AG & Co. KGaA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Packaging Industry in South-East Asia Countries

- 4.1.2 Growing Demand in Construction Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations Regarding VOC Emissions

- 4.2.2 High Fluctuations in Raw Material Pricing

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Adhesives Resin

- 5.1.1 Polyurethane

- 5.1.2 Epoxy

- 5.1.3 Acrylic

- 5.1.4 Silicone

- 5.1.5 Cyanoacrylate

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins (Polyester, Rubber, etc.)

- 5.2 Adhesives Technology

- 5.2.1 Solvent-borne

- 5.2.2 Reactive

- 5.2.3 Hot Melt

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Sealants Resin

- 5.3.1 Silicone

- 5.3.2 Polyurethane

- 5.3.3 Acrylic

- 5.3.4 Epoxy

- 5.3.5 Other Resins (Bituminous, Polysulfide UV-Curable, etc.)

- 5.4 End-User Industry

- 5.4.1 Aerospace

- 5.4.2 Automotive

- 5.4.3 Building and Construction

- 5.4.4 Footwear and Leather

- 5.4.5 Healthcare

- 5.4.6 Packaging

- 5.4.7 Woodworking And Joinery

- 5.4.8 Other End-user Industries (Electronics, Consumer/DIY, etc.)

- 5.5 Geography

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Japan

- 5.5.4 South Korea

- 5.5.5 Indonesia

- 5.5.6 Malaysia

- 5.5.7 Thailand

- 5.5.8 Vietnam

- 5.5.9 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 Avery Dennison Corporation

- 6.4.5 Beardow Adams

- 6.4.6 Dow

- 6.4.7 DuPont

- 6.4.8 Dymax Corporation

- 6.4.9 Franklin International

- 6.4.10 H.B. Fuller Company

- 6.4.11 Henkel AG & Co. KGaA

- 6.4.12 Huntsman International LLC

- 6.4.13 ITW Performance Polymers (Illinois Tool Works Inc.)

- 6.4.14 Jowat AG

- 6.4.15 Mapei Inc.

- 6.4.16 Tesa SE (A Beiersdorf Company)

- 6.4.17 Pidilite Industries Ltd.

- 6.4.18 Sika AG

- 6.4.19 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation and Development of Bio-based Adhesives

- 7.2 Shifting Focus Toward Adhesive Bonding for Composite Materials