PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521908

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521908

Food-grade Post-Consumer Recycled (PCR) Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Food-grade Post-Consumer Recycled Packaging Market size in terms of shipment volume is expected to grow from 5.86 Million tonnes in 2024 to 8.37 Million tonnes by 2029, at a CAGR of 7.38% during the forecast period (2024-2029).

Key Highlights

- The increasing need for reducing energy use, lowering emissions, promoting a circular economy, achieving sustainability targets, reducing packaging waste, FDA and other regulations for contact-sensitive applications, and regulatory pressure are the major factors propelling the demand for food-grade post-consumer recycling packaging solutions.

- Packaging recycling rates worldwide are increasing due to the development of recycling infrastructure, advanced recycling processes, effective processing techniques, and positive government response. This will result in increased availability of post-consumer recycled material. According to the Environment Agency, the packaging recycling target in the United Kingdom is expected to reach 80% by the end of 2024, compared to 77% in 2023. The increasing recycling rate is expected to aid the growth of food-grade post-consumer recycling packaging solutions.

- End-user brands are trying to adhere to regulatory measures to stay ahead of the competition and address the growing consumer awareness for post-consumer recycled packaging. For instance, Keurig Dr Pepper, an American beverage company, committed to reducing virgin plastic use by 20% across the company's product packaging portfolio by 2025 and increasing recycled content in plastic packaging.

- Packaging manufacturers are developing innovative, contact-sensitive, post-consumer recycled packaging solutions using advanced technologies. Furthermore, raw material manufacturers, providers, and converters are adopting the latest recycling technology to offer food-grade PCR material.

- In 2024, Borealis AG received letters of no objection (LNOs) from the US Food & Drug Administration (FDA) for its Borcycle M post-consumer recycled plastics (PCR) used for food-grade packaging. This material is sensitive to packaging applications, including cosmetics, personal care, and food contact. The company developed Borcycle M post-consumer recycled plastics (PCR) using transformational mechanical recycling technology. This technology offers post-consumer plastic waste another life in an energy-efficient way.

- Besides this, the need for more material availability due to the improper recycling of plastic material creates supply issues. The improperly discarded packaging material creates contamination problems during recycling, which may hamper the market's growth. The continuous effort by the recyclers and increasing investments driven by EPR are projected to improve recycling collection and infrastructure. This is expected to overcome the concern of material availability.

Food-grade Post-Consumer Recycled (PCR) Packaging Market Trends

Rising Adoption of Recycled Packaging Solutions in the Food and Beverage Industry

- Food and beverage products are mostly packed in food-grade packaging to maintain their quality and avoid any chemical reaction when in contact with the packaging solution. These solutions include bottles, cans, pouches, and liquid cartons made from plastic, glass, metal, or paper.

- Considering the increasing focus on sustainable packaging solutions, along with propelling regulation and consumer awareness, brand owners are looking for post-consumer recycled packaging solutions. For instance, in October 2023, Coca-Cola India launched Coca-Cola in 250-mL and 750-mL rPET bottles. Furthermore, in April 2024, Coca-Cola rolled out 500-ml bottles made from rPET in Hong Kong. The company aims to implement 50% recycled material across its packaging lines by 2030. This showcases the company's journey toward a circular economy and a sustainable and greener future.

- Packaging manufacturers are also trying to offer innovative post-consumer recycled packaging solutions for food contact packaging to take advantage of growing opportunities. The companies are focusing on adopting an advanced recycling process to cater to the regulatory requirements for food contact packaging and contact-sensitive applications.

- In March 2024, Amcor Group GmbH collaborated with INEOS Olefins & Polymers Europe and PepsiCo to launch a new snack packaging for PepsiCo's snack brand, Sunbites Crisps. The new packaging contains 50% recycled plastic. Post-consumer plastic packaging waste is converted using Plastic Energy's technology. Pyrolysis oil is used as an alternative to traditional fossil feedstock to produce recycled material and compile it to meet food contact performance requirements.

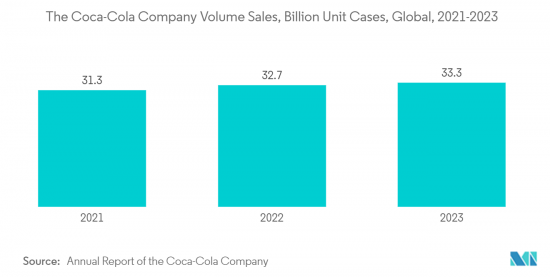

- The increasing consumption of food and beverage products and the brand's focus on sustainable packaging fuel the growth of food-grade post-consumer recycled packaging solutions. The surge in the unit volume sales of the beverage and food brands aids the market's growth. The major non-alcoholic beverage brand, the Coca-Cola Company, sold 33.3 billion unit cases (one unit case equal to 192 US fluid ounces of finished beverage) in 2023 compared to 32.7 billion unit cases in 2022.

Increasing Regulatory Pressure in Various Regions to Include a Minimum Percentage of Recycled Content for Packaging Products

- Increasing packaging waste, which leads to various environmental problems, has created the need for sustainable packaging solutions such as recyclable, post-consumer recycled material, biodegradable, and others. To overcome the sustainability concern, governments and other regulatory agencies in various regions, such as Europe, Canada, the United States, and others, are putting pressure on using post-consumer recycled material for packaging solutions. This would result in lower greenhouse gas emissions and lower energy consumption and contribute to a circular economy.

- For instance, in April 2024, the European Parliament adopted the Packaging and Packaging Waste Regulation (PPWR), which would contribute to the transition to a circular economy. It includes various provisions for packaging solutions, such as the requirement that any plastic packaging placed on the market contain a minimum percentage of recycled content.

- The minimum percentage of recycled content will depend upon the packaging type, such as 30% PCR for single-use plastic beverage bottles, 30% PCR for contact-sensitive PET packaging, and 10% PCR for contact-sensitive other plastic packaging. These minimum percentages would increase from 2040. Such provision in the region is expected to drive the demand for food-grade post-consumer recycled packaging solutions.

- Similarly, the Action Plan on Zero Plastic Waste by the Canadian Council of Ministers of the Environment endorsed a provision stating a 50% recycled content requirement in plastic packaging products by 2030. The scope includes beverage packaging containers, non-food bottles, and other rigid containers and trays.

- In early 2023, California, Washington, New Jersey, and Maine passed laws requiring post-consumer recycled content in plastic packaging. California's law requires 25% PCR for glass and plastic beverage bottles by 2025 and 50% by 2050, while Washington's law requires 25% PCR for plastic beverage bottles by 2026 and 15% PCR for plastic wine and dairy containers by 2025.

- Food-grade packaging is required for products that come in contact with it to avoid damage. The increasing provision and regulation over the use of post-consumer recycled material for beverage products is expected to aid the growth of food-grade post-consumer recycled packaging.

Food-grade Post-Consumer Recycled (PCR) Packaging Industry Overview

The food-grade post-consumer recycled (PCR) packaging market is fragmented, with various global and local players. The packaging players in the market are trying to offer food-grade post-consumer recycled packaging solutions to adhere to the growing regulatory pressure, attain sustainability targets, and cater to the demand for minimum PCR content for packaging type. The key players in the market are developing new solutions to strengthen the market share and stay ahead of the competitors.

- In April 2024, Amcor Group GmbH announced the launch of a one-liter polyethylene terephthalate (PET) bottle made from 100% post-consumer recycled (PCR) content for carbonated soft drinks (CSD). The company focuses on expanding the product portfolio for responsible packaging made from recycled content and helping customers meet sustainability commitments and requirements.

- In April 2024, Klockner Pentaplast announced the launch of food packaging trays made with 100% recycled PET (rPET). With the launch of 100% recycled PET food trays, the company is focusing on creating a more sustainable packaging industry without compromising quality or safety.

- In December 2023, Novolex Holdings LLC introduced packaging containers for food made with a minimum of 10% post-consumer recycled (PCR) content. These containers are recyclable. The launch of new products will help the company reduce the environmental impact and support the circular economy.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Geopolitical Scenario Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Consumer Awareness and Need for Lowering Greenhouse Gas Emissions to Overcome the Sustainability Concerns

- 5.1.2 Increasing Regulatory Pressure to Include a Minimum Percentage of Recycled Content for Packaging Products

- 5.2 Market Restraint

- 5.2.1 Inadequate Recycling Infrastructure Leads to Improper Supply of Materials and Results in High Prices

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Plastic

- 6.1.1.1 Polyethylene Terephthalate (PET)

- 6.1.1.2 Polyethylene (PE)

- 6.1.1.3 Polypropylene (PP)

- 6.1.1.4 Other Plastics

- 6.1.2 Glass

- 6.1.3 Metal

- 6.1.4 Paper & Paperboard

- 6.1.1 Plastic

- 6.2 By Product Type

- 6.2.1 Bottles and Containers

- 6.2.2 Cans

- 6.2.3 Pouches and Bags

- 6.2.4 Trays and Clamshells

- 6.2.5 Other Product Types

- 6.3 By End-user Industry

- 6.3.1 Food

- 6.3.2 Beverage

- 6.3.3 Personal Care and Cosmetics

- 6.3.4 Healthcare and Pharmaceuticals

- 6.3.5 Other End User Industry

- 6.4 Geography***

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.2.5 Spain

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.5 Middle East and Africa

- 6.4.5.1 Saudi Arabia

- 6.4.5.2 South Africa

- 6.4.5.3 Egypt

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Berry Global Group Inc.

- 7.1.2 Amcor Group GmbH

- 7.1.3 Novolex Holdings LLC

- 7.1.4 Tekni-Plex Inc.

- 7.1.5 Klockner Pentaplast

- 7.1.6 Coveris Management GmbH

- 7.1.7 Hoffmann Neopac AG

- 7.1.8 Silgan Dispensing Systems (Silgan Holdings Inc.)

- 7.1.9 Greiner Packaging International GmbH

- 7.1.10 Avery Dennison Corporation

- 7.1.11 Nussbaum Matzingen AG

- 7.1.12 Gallo Glass Company

- 7.1.13 Great Little Box Company Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET