PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521868

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521868

Shared Mobility - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

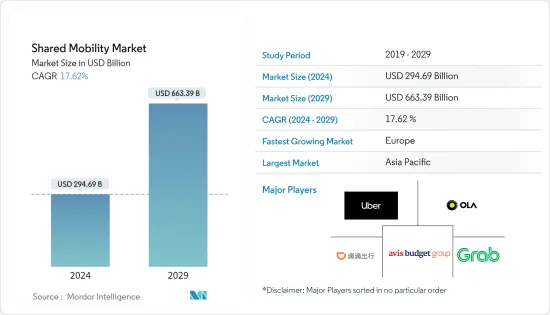

The Shared Mobility Market size is estimated at USD 294.69 billion in 2024, and is expected to reach USD 663.39 billion by 2029, growing at a CAGR of 17.62% during the forecast period (2024-2029).

In the long term, consumers' increasing preference toward ride-hailing, car-sharing, and rental services owing to the lower cost of transportation will drive the shared mobility market across the world. Due to the increasing traffic congestion and higher ownership cost of purchasing new vehicles, consumers tend to avail ride-hailing as a preferred medium for their daily commutes. Further, the integration of various new entrants with a strong competitive edge is expected to disrupt the market. For instance, inDrive, a ride-hailing platform, offers a bid-based platform suitable for both drivers and consumers, as it helps negotiate a fixed price for short-distance travel and avoids the surge price charged by other competitors.

Key Highlights

- In Q3 2023, Beijing, Changchun, and Chongqing were the leading cities in China with the highest rush hour congestion. The rush hour congestion index in Beijing touched 2.09 in Q3 2023, followed by Changchun with an index of 2.05 and Chongqing with an index of 1.97 during the same period.

- According to the TomTom Index, London, Dublin, and Toronto were the major city centers across the world with the highest traffic congestion in 2023. The average time to travel 10 km in London is 37 minutes and 20 seconds, the highest in the world.

The ease of travel and the convenience of driving through traffic are leading to an increasing demand for two-wheeler hailing and sharing services, especially in Asia-Pacific. Some prominent countries with a significant shared micro-mobility market across Asia-Pacific include India, China, and Vietnam, which are attributed to the lower cost charged compared to availing a car-hailing service. Further, in recent years, there has been a massive penetration of electric two-wheelers in the shared mobility industry to complement the government's decarbonization effort, which is expected to foster the growth of the shared mobility market between 2024 and 2029.

Key Highlights

- In August 2023, Green and Smart Mobility (GSM) announced the commencement of its e-motorcycle-hailing service in Vietnam to solidify its market position and compete with players such as GoJek and Grab. Further, the company stated its plan to operate 60,000 e-motorcycles on Vietnamese roads in five localities across the country.

Moreover, increasing investment in the corporate sector and the worldwide urbanization rate contribute to consumers migrating to urban areas for better employment opportunities. With more consumers migrating to urban areas, there is a massive demand for jobs in these areas, which, in turn, is expected to expand the market for employee transportation needs. To cater to the increasing need for employee transportation, various shared mobility players are strategizing to enter this space by offering on-demand shuttle services, which, in turn, positively impact the demand for the shared mobility market worldwide.

Shared Mobility Market Trends

The Passengers Cars Segment is Expected to Gain Traction Between 2024 and 2029

Passenger cars are extensively utilized in ride-hailing, car-sharing, rental, and leasing services. Operators or individual owners deploy various car makes, such as hatchbacks, sedans, and sports utility vehicles (SUVs), to enhance customers' convenience. Therefore, the growing urbanization rate and the influx of tourists worldwide are significant determinants for the growth of the passenger cars segment, owing to their massive requirement for ride-hailing and rental services. Moreover, the rising investment in the corporate sector to expand job opportunities and expand economic growth leads to businesses demanding leasing services for employee transportation purposes, which, in turn, is positively impacting the demand for passenger cars segment.

- According to the World Tourism Organization, the total number of international tourist arrivals worldwide reached 1,258.66 million in 2023 compared to 960.19 million in 2022, representing a 31.0% Y-o-Y growth between 2022 and 2023.

- According to the Population Reference Bureau, North America, Latin America, and Europe were the leading continents worldwide with the highest urban population in 2023. The share of urban population as a percentage of the overall population in North America touched 83% in 2023, followed by Latin America (82%) and Europe (75%) during the same period.

To complement the government's effort to decarbonize the transport sector, ride-hailing operators and rental providers worldwide increasingly prefer deploying electric passenger cars in their fleets. Further, with more consumers demanding electric passenger cars as their preferred choice of transportation, these players are expected to invest hefty sums in acquiring new-age vehicles in their fleet to meet the surging demand, which, in turn, will positively impact the growth of this market segment.

- In November 2023, Green and Smart Mobility (GSM), a Vietnamese-based ride-hailing company, announced the launch of its electric taxi service in Laos and Vietnam to position its brand as a sustainable mode of shared transportation. The company plans to deploy Vinfast VF5 electric cars to expand its fleet, which will be available to consumers in Vietnam and Laos.

The shared mobility market is anticipated to witness the integration of various ride-hailing and rental companies worldwide, attributed to the lucrative opportunity that the market presents. As more companies integrate into the ecosystem, a massive demand will exist for passenger cars to be utilized for shared mobility. Moreover, consumers are shifting their preferences toward availing of lower-cost private transportation, which is further expected to foster the growth of this segment.

Asia-Pacific is the Largest Shared Mobility Market Across the World

Consumers' increasing preference toward availing private mediums of transportation for traveling purposes owing to the rising need for convenience in personal mobility, high internet penetration rate, and the growing number of tourists in Asia-Pacific serve as significant drivers for the growth of the shared mobility market. Moreover, this region witnesses a substantial demand for two-wheeler hailing services due to the worsening traffic congestion and the need for faster city travel, which, in turn, positively impacts the growth of this segment.

- According to the World Tourism Organization, the number of international tourist arrivals in Asia-Pacific reached 233.43 million in 2023 compared to 91.52 million in 2022, representing a Y-o-Y growth of 155.0% between 2022 and 2023.

- According to the TomTom Index, Bengaluru and Pune in India were the sixth and seventh cities with the highest traffic congestion worldwide, respectively. The average travel time for commuters to travel 10 km in Bengaluru was 28 minutes and 10 seconds, while it reached 27 minutes and 50 seconds in Pune.

Further, integrating electric vehicles in shared mobility fleets can significantly reduce carbon emissions from the economy. Hence, governments across Asia-Pacific are increasingly strategizing to promote the use of electric vehicles in rental, ride-hailing, and other shared mobility fleets. Various new entrants are investing hefty sums in deploying electric cars in their fleets to cater to the increasing consumer demand.

- In September 2023, Ola Cabs announced the launch of its e-bike service in Bengaluru to promote the electrification of ride-hailing fleets across India. Between September 2023 and January 2024, the company witnessed a 40% expansion in this segment by completing more than 1.75 million rides. The company plans to launch this service across cities in India in the coming years.

Moreover, the expanding corporate investment in countries such as China, South Korea, and India is actively leading to companies demanding rental solutions, which, in turn, is further anticipated to contribute to the surging growth of the shared mobility market in the region. In the coming years, Asia-Pacific will witness companies spending hefty sums to enhance their digital platforms to attract consumers and actively seek partnerships with automakers to acquire vehicles in their fleet at a lower cost.

Shared Mobility Industry Overview

The shared mobility market is fragmented and highly competitive due to the presence of various international and domestic players operating in the ecosystem. Some prominent players include Uber Technologies Inc., ANI Technologies Pvt. Ltd, Avis Budget Group Inc., Beijing DiDi Chuxing Technology Co. Ltd, Grab Holdings Inc., Hertz Global Holdings, Lyft Inc., Drive Now (BMW AG), Europcar Mobility Group, Cabify, Curb Mobility, and BlaBlaCar. These players actively seek to expand their business into other geographies to enhance their brand visibility and constantly focus on improving consumer experience.

- In April 2024, Yulu announced its partnership with Yuva Mobility to launch franchise-based partner-led shared mobility services in Indore and Madhya Pradesh, India. The partnership will witness the introduction of electric vehicles offered to consumers as shared mobility services. Further, the company aims to expand its customer base to cater to the surging demand for EVs among students, leisure riders, tourists, and professionals in these cities.

- In April 2024, Hoop Carpool announced that it had raised an investment from Mango Startup Studio in the form of a convertible equity loan. The investment aims to facilitate a six-month trial period during which Mango employees and other car-sharing riders will use Hoop Carpool services for their daily commutes.

The market is anticipated to witness various mergers and acquisitions between firms operating in the ecosystem, which will assist them in enhancing their profitability prospects and help cater to a broader customer base.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Preference of Consumers toward Ride-Hailing Services is Expected to Foster the Growth of the Market

- 4.2 Market Restraints

- 4.2.1 Strict Government Regulations to Govern the Shared Mobility Industry Hampers the Growth of the Market

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

- 5.1 By Type

- 5.1.1 Ride-Hailing

- 5.1.2 Car Sharing

- 5.1.3 Shared Micromobility (E-Bikes, E-Scooters, etc.)

- 5.1.4 Rental and Leasing

- 5.1.5 Others (Shuttle Services, Bus Services, etc.)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles (Pickup Vans, etc.)

- 5.2.3 Buses and Coaches

- 5.2.4 Two-Wheelers

- 5.3 By Business Model

- 5.3.1 Peer-to-Peer (P2P)

- 5.3.2 Business-to-Business (B2B)

- 5.3.3 Business-to-Consumer (B2C)

- 5.4 By Propulsion Type

- 5.4.1 Internal Combustion Engine (ICE)

- 5.4.2 Electric

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 South America

- 5.5.4.2 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Uber Technologies Inc.

- 6.2.2 ANI Technologies Pvt. Ltd (Ola Cabs)

- 6.2.3 Avis Budget Group Inc.

- 6.2.4 Beijing Didi Chuxing Technology Co. Ltd

- 6.2.5 Hertz Global Holdings

- 6.2.6 Grab Holdings Inc.

- 6.2.7 Lyft Inc.

- 6.2.8 Drive Now (BMW AG)

- 6.2.9 Europcar Mobility Group

- 6.2.10 Cabify

- 6.2.11 Zoomcar Holdings

- 6.2.12 Revv

- 6.2.13 Curb Mobility LLC

- 6.2.14 BlaBlaCar

- 6.2.15 Wingz Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 High Cost of Ownership of Private Vehicles Fuels the Market Demand