PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521855

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521855

Healthcare Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

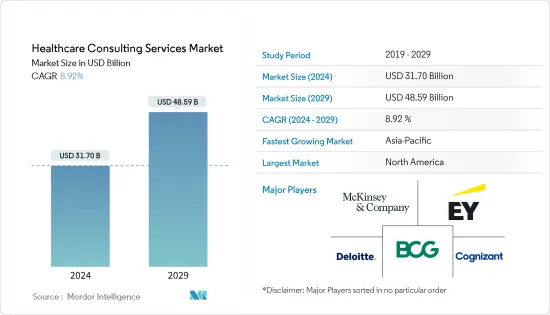

The Healthcare Consulting Services Market size is estimated at USD 31.70 billion in 2024, and is expected to reach USD 48.59 billion by 2029, growing at a CAGR of 8.92% during the forecast period (2024-2029).

The major factors driving the market growth include the rising demand for healthcare products and the rising need to improve the quality of care and reduce healthcare costs.

Healthcare has witnessed substantial changes in the past few years in terms of serving the growing patient population. The healthcare consulting services market is mainly driven by the rapid adoption of global digitalization. Robust IT support with agile methods is a competitive advantage for healthcare providers in achieving increased profitability, simplifying inventory management, improving quality, and controlling costs.

The integration of healthcare consulting services with medicine is expected to deliver benefits, like identifying individuals who may benefit from lifestyle changes or preventative care, analyzing patient characteristics, classifying broad-scale disease profiling to identify predictive events and support prevention initiatives, and analyzing the cost and outcomes of care to identify cost-effective treatments. For example, the International Diabetes Federation 2022 estimated that by 2045, the global expenditures for diabetes treatment are expected to grow to USD 1,054 billion due to technological advancements, which can primarily be attributed to the high adoption of wireless and wearable devices and applications. Therefore, such a huge expenditure on chronic diseases is anticipated to increase the adoption of healthcare consulting services to develop strategies for the reduction of the healthcare burden on patients.

Furthermore, the rising partnerships among the healthcare providers and the healthcare consulting service providers are also anticipated to increase the demand in the market studied during the forecast period, driving the market's growth. For instance, in June 2023, a syndicate of four businesses: data analyst Vuit, advisory firm Develop Consulting, healthcare improvement specialist Innovative Online Products, and training provider Click2 Learn launched an Integrated Improvement Partnership for National Health Service (NHS) in the United Kingdom. This will help the NHS realize efficiencies within the UK healthcare system and develop strategies for efficiency savings and capacity building across the NHS.

Furthermore, there has been a rise in IT healthcare consulting opportunities due to favorable government policies in developed and developing regions. Other factors include increasing government support for healthcare IT solutions and the changing technology landscape during the forecast period. However, the high cost of deployment is expected to restrain the growth of the market.

Healthcare Consulting Services Market Trends

Hospitals Segment Expected to Hold a Significant Share in the Healthcare Consulting Services Market During the Forecast Period

- Hospitals are digitalizing their business practices in IT security services, support services, resource planning, IT infrastructure management, mobile computing, and cloud-based solutions. With scalable operations, healthcare providers have witnessed increased revenues in the healthcare consulting services market.

- IT consulting in hospitals can help achieve a more significant and continuous flow of information within a digital healthcare infrastructure. Outsourced IT consulting services include analytics dashboards, development and maintenance of clinical platforms, network optimization services, IT procurement, and cloud services.

- Rising partnerships among hospitals and healthcare consulting firms are anticipated to increase the demand for IT consulting services to sustain hospital revenue growth and thereby boost segment growth. For instance, in October 2023, Cura, a virtual healthcare solutions provider, partnered with the Saudi German Hospital Group to revolutionize patient access to healthcare services. This partnership allows patients to utilize various healthcare services, including online consultations, remote monitoring, and health information exchange integrated across all Saudi German Hospital Group locations.

- Furthermore, the hospitals are also taking support for revenue cycle management, enterprise resource planning (ERP) support service, and population health, which are also anticipated to contribute to the market's growth. In addition, the transition from fee-for-service (FFS) to value-based care is increasing the pressure on healthcare providers. Thus, hospitals are anticipated to hold a significant market share during the forecast period.

North America Holds a Significant Share in the Market and is Expected to Continue the Same During the Forecast Period

- The market's growth in North America is attributed to changes in medicare payments and regulations. As a result, healthcare providers are increasingly dependent on healthcare IT consulting companies.

- Furthermore, with regulatory reforms in the United States, there is increased competition among payers for cost savings and customer satisfaction. Healthcare payers and providers are undergoing technological transformation as they are applying novel operating models that need IT support from consulting firms.

- According to data published by the United States Department of Health and Human Services in 2024 in the form of an Annual Performance Plan and Report, the number of participants served by the state/jurisdiction maternal, infant, and early childhood home visiting (MIECHV) program in FY2023 was 164,470 compared to 188,067 in FY2024. Thus, the increase in maternal, infant, and early childhood visits fuels the demand for maternal, fetal, and infant care, boosting the growth of the healthcare consulting services market.

- In addition, in the United States, government funding programs that provide healthcare services like the Centers for Medicare and Medicaid Services for people aged 65 years and older, as well as some people with disabilities working in partnership with the state governments, are likely to boost the market.

- Rising partnerships among healthcare consulting firms in the home healthcare domain are anticipated to propel the market's growth. For instance, in March 2024, Brinster & Bergman entered a partnership with Gary Carpenter and Associates, a home healthcare consulting firm, to assist home healthcare agencies with strategies for exploring state regulatory and tax laws.

- Moreover, small and big healthcare providers are outsourcing healthcare consulting services to third-party providers, as they cannot handle all the complex changes in the healthcare system. With innovative approaches, such as data security and analytics, healthcare providers benefit by improving the experience of patients and, therefore, gaining increased revenues. This is likely to contribute to the growth of the healthcare consulting services market in North America.

Healthcare Consulting Services Industry Overview

The healthcare consulting services market is highly fragmented and experiencing healthy growth owing to the greater adoption of healthcare consulting services by smaller and mid-sized end users. Moreover, healthcare consulting service market penetration is expected to increase in Asia-Pacific, offering growth opportunities for new entrants. Some of the players operating in the market are Accenture, Deloitte Touche Tohmatsu LLC, The Boston Consulting Group, Cognizant, and McKinsey and Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Healthcare Products

- 4.2.2 Rising Need to Improve the Quality of Care and Reduce Healthcare Costs

- 4.3 Market Restraints

- 4.3.1 Availability of Similar Technology

- 4.3.2 High Cost of Deployment

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Service Type

- 5.1.1 Digital Consulting

- 5.1.2 IT Consulting

- 5.2 By Component

- 5.2.1 Services

- 5.2.2 Solutions

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Clinics

- 5.3.3 Life Science Companies

- 5.4 By Application

- 5.4.1 Financial

- 5.4.2 Operations Management

- 5.4.3 Population Health

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Deloitte Touche Tohmatsu Limited

- 6.1.2 McKinsey & Company

- 6.1.3 Accenture Consulting

- 6.1.4 Huron Consulting

- 6.1.5 PWC

- 6.1.6 Ernst & Young

- 6.1.7 The Boston Consulting Group

- 6.1.8 Bain & Company

- 6.1.9 KPMG

- 6.1.10 Cognizant

- 6.1.11 IQVIA

- 6.1.12 ZS

7 MARKET OPPORTUNITIES AND FUTURE TRENDS