PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521808

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521808

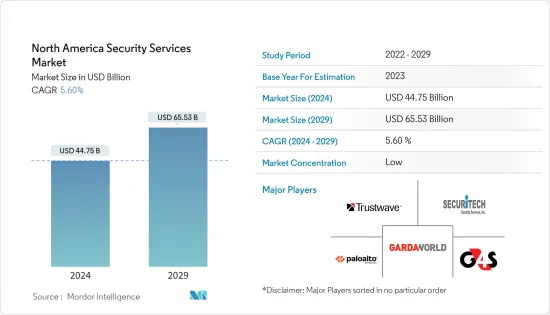

North America Security Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The North America Security Services Market size is estimated at USD 44.75 billion in 2024, and is expected to reach USD 65.53 billion by 2029, growing at a CAGR of 5.60% during the forecast period (2024-2029).

Key Highlights

- The emergence of advanced technologies, such as threat intelligence, machine learning, and artificial intelligence, creates a need for sophisticated security services that can effectively address the increasing threats. As AI-based technologies advance, the security services market is likely to continue to witness the development of specialized tools by experienced developers to address specific issues. The result of technological solutions has also led to an increase in acquisition activity as companies seek to gain a deeper understanding of emerging markets.

- Organizations are shifting to cloud-based services for scalability and flexibility. The importance of cloud security solutions in safeguarding data and applications is on the rise. For instance, in July 2023, the Government of the United States asserted that cloud computing can offer enhanced security, improved efficiency, and decreased expenses. Increased reliance on cloud services can enable the federal government to strengthen the provision of services to its citizens and protect its networks.

- The North American financial services sector is particularly vulnerable to cybercriminals, as it is home to a wealth of financial data. This data is held by banks, insurance companies, and financial technology companies and is the driving force behind the need for comprehensive security solutions to combat financial fraud and cyber-attacks. According to the FTC (Federal Trade Commission), financial fraud involving bank transfers or payments in the United States in 2022 caused losses of USD 1.59 billion. The evolving tactics of cybercriminals drive the demand for advanced security services and continuous monitoring.

- Cybercrime remains a significant issue in North America and influences the security services market. There has been a considerable increase in data breaches caused by phishing, credential theft, and ransomware. Data security is becoming increasingly difficult as the use of artificial intelligence and IoT technologies increases. As new cyberattack vectors emerge, organizations can be put at risk if security services are inadequate, thus impeding market development.

- Moreover, since the pandemic outbreak, economies of multiple countries, which feel significant, are still unable to recover as anticipated, which is bringing a shadow of economic recession, especially in North America. For instance, according to the International Monitory Fund (IMF) estimates, the real GDP growth of the United States is anticipated to remain in a slowdown phase till 2024 before regaining momentum again.

North America Security Services Market Trends

The IT and Infrastructure Segment is Expected to Hold Significant Market Share

- The IT and infrastructure sector is a significant driver of the need for security services, as they play a fundamental role in contemporary business operations, and security threats have become increasingly complex. Furthermore, with the increasing intricacy of network architectures and the proliferation of interconnected devices, the demand for network security services to identify and mitigate threats within IT infrastructures is growing.

- For instance, in April 2023, IBM introduced the QRadar Security Suite, designed to facilitate detecting and responding to threats. This suite includes a modernized, unified interface that simplifies the response of analysts throughout the entire attack lifecycle. Additionally, the suite is equipped with advanced artificial intelligence and automation capabilities that have been demonstrated to reduce alert triage times by an average of 55%.

- IAM (Identity and Access Management) solutions safeguard IT resources from unauthorized access. Security services provide organizations with the necessary tools to implement IAM best practices. For instance, in September 2023, Oracle announced updates to its Oracle Access Governance service to assist IT teams in better assigning, monitoring, and managing user access to applications and other technology resources. The cloud-native service offers comprehensive visibility into user interactions with technology resources, helping to mitigate risk by enabling only authorized users to access, view, and interact with restricted assets, including patents and databases, applications, and infrastructure resources such as cloud servers and services.

- The IT and infrastructure sectors are increasingly adopting advanced technologies such as AI (artificial intelligence), machine learning, and security analytics to detect and analyze potential threats. Security services are taking advantage of these technologies to improve their security. Furthermore, the shift toward cloud-based Managed Security Services is further supported by the growing adoption of advanced technologies, such as big data analytics, threat intelligence, and advanced automation platforms. To meet the industry's ever-changing needs, several market players are introducing comprehensive services through innovative and collaborative approaches.

- Network intrusion is a significant source of demand for security services in the IT and infrastructure sectors, as it can considerably impact the security of data, critical systems, and other sensitive information. According to BakerHostetler, network intrusion was identified as the most prevalent cybercrime attack on United States-based companies in 2022, which made up 45% of all incidents. In second place was the business e-mail compromise (BEC), accounting for 30% of all data security incidents in US-based companies, with 12% reporting inadvertent disclosure.

The United States Holds the Largest Market Share

- The prevalence of demand for security services in the United States results from a complex combination of factors, including its economic importance, its position as a technological and innovation center, its vast critical infrastructure resources, and the ever-changing threat environment. Innovative city solutions in the United States are expected to experience a surge in demand as investments in modernizing urban telecommunications networks to 5G technology will increase the digitization of city infrastructure and services, which in turn will create a need for security services.

- The United States is confronted with many cyber-attacks, such as nation-state cyber-attacks, ransomware, and data breaches. Organizations in various industries require cybersecurity services to protect themselves from these threats.

- For instance, in September 2023, the Cybersecurity Infrastructure Security Agency declared the launch of the "Secure Our World" program, a national cybersecurity public awareness initiative to teach all Americans how to protect themselves online. This program focuses on four basic steps individuals can take to remain secure online: using strong passwords, multi-factor authentication, recognizing and reporting phishing, and updating software.

- The United States has adopted advanced technologies such as 5G, internet of things (IoT), and artificial intelligence (AI). These technologies present novel security issues and stimulate the need for specialized security solutions. The implementation of 5G technology has enabled the rapid expansion of the Internet of IoT and sensors. However, many IoT devices possess limited security capabilities, making them susceptible to malicious attacks. As a result, the demand for security services is increasing due to the need to protect IoT ecosystems.

- The United States is home to one of the world's largest and most diversified economies, encompassing many businesses and industries. Defending this economic infrastructure against cyberattacks, physical security threats, and other vulnerabilities is a primary focus of security services. The Identity Theft Resource Center reported that 3,205 data compromises occurred in the United States in 2023, while more than 353.02 million individuals were exposed to data breaches, leaks, and exposures in the same year. While these three incidents are distinct, they all have one commonality: an unauthorized threat actor gains access to the sensitive data.

North America Security Services Industry Overview

The North American security services market is fragmented due to the presence of various small and large players. All the major players account for a significant share of the market and are focusing on expanding the consumer base in the region. Some of the significant players in the market are Trustwave Holdings Inc., Securitech Security Services, Palo Alto Networks, GardaWorld, G4S Limited, SOS Security Systems, Diebold Nixdorf, and Broadcom Inc. Companies are increasing the market share by forming multiple partnerships, collaborations, and acquisitions and investing in introducing new products to earn a competitive edge between 2024 and 2029.

- July 2023 - Artificial Intelligence Technology Solutions Inc. entered into a strategic partnership with its wholly owned subsidiary, Robotic Assistance Devices Inc. (RAD) and GardaWorld Security Systems. This partnership will enable RAD to deploy AI-enabled robotic devices across Canada. RAD's products are an ideal complement to existing physical security customers, providing them with a cost-effective and AI-powered solution to improve situational awareness through remote video monitoring. These products are designed to facilitate the detection of threats and events, including firearms, through automated and bi-directional voice communication.

- March 2023 - Trustwave partnered with Trellix to provide enhanced managed security services. The terms of the partnership stipulate that Trustwave will provide end-to-end security support for Trellix and offer MDR (Managed Detection and Response) services in collaboration with the security platform. Trustwave MDR, as provided by Trustwave, functions as a remote, external security operations center. Given the increasing complexity of modern security threats, the goal is to enable end-user companies to offload critical components of their security infrastructure. This measure is especially pertinent for mid-size companies, where the number of in-house security personnel may be less extensive.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Digital Disruption and Increased Compliance

- 5.1.2 Rapid Cloud Adoption

- 5.1.3 Growing Adoption of Managed Security Services

- 5.2 Market Challenges

- 5.2.1 The Increasing Frequency and Sophistication of Cyberattacks

- 5.2.2 High Implementation Costs

- 5.2.3 Lack of Awareness of Security Services

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Managed Security Services

- 6.1.2 Professional Security Services

- 6.1.3 Consulting Services

- 6.1.4 Threat Intelligence Security Services

- 6.2 By Mode of Deployment

- 6.2.1 On-Premise

- 6.2.2 Cloud

- 6.3 By End-user Industry

- 6.3.1 IT and Infrastructure

- 6.3.2 Government

- 6.3.3 Industrial

- 6.3.4 Healthcare

- 6.3.5 Transportation and Logistics

- 6.3.6 Banking

- 6.3.7 Other End-user Industries

- 6.4 By Country

- 6.4.1 United States

- 6.4.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Trustwave Holdings Inc.

- 7.1.2 Securitech Security Services

- 7.1.3 Palo Alto Networks

- 7.1.4 GardaWorld

- 7.1.5 G4S Limited

- 7.1.6 SOS Security Systems

- 7.1.7 Diebold Nixdorf

- 7.1.8 Broadcom Inc.

- 7.1.9 Allied Universal

- 7.1.10 Fujitsu Limited

- 7.1.11 Securitas Inc.

- 7.1.12 IBM Corporation

- 7.1.13 Fortra LLC

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET