PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521777

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521777

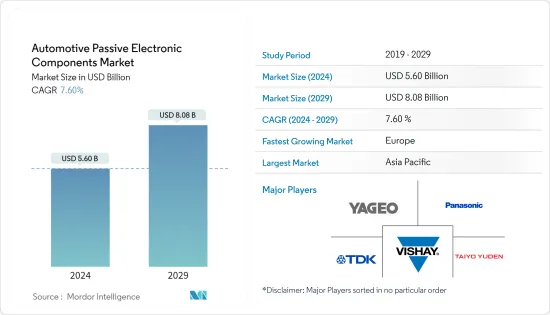

Automotive Passive Electronic Components - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Automotive Passive Electronic Components Market size is estimated at USD 5.60 billion in 2024, and is expected to reach USD 8.08 billion by 2029, growing at a CAGR of 7.60% during the forecast period (2024-2029).

Key Highlights

- The automotive industry is leading the way in the increasing need for passive components. The demand for electronic vehicle systems is rising for various uses, such as electronic control units (ECUs) under the hood, infotainment systems, and advanced driver assistance systems (ADASs). Automotive electronic systems require high-quality components to guarantee dependable performance, like capacitors for filtering and storing energy, varistors for circuit protection, connectors for small ECUs, and RF and microwave passive components and antennas for connectivity support.

- Automobile manufacturers increasingly integrate electronic components into traditional combustion engine vehicles to enhance fuel efficiency, reduce emissions, and improve overall vehicle performance. This trend drives the demand for passive electronic components like resistors, capacitors, and inductors. For instance, according to SIAM India, during the fiscal year 2023, more than 3.89 million passenger vehicles were sold in the domestic market.

- ADAS (advanced driver assistance systems), such as collision avoidance systems and adaptive cruise control, rely heavily on passive electronic components like capacitors for sensor signal processing, filtering, and data transmission. Modern vehicles feature advanced infotainment systems, telematics, and connectivity solutions that require passive components for wireless communication, signal processing, and data transmission.

- As automotive electronics become more compact and integrated, passive components must meet increasingly stringent size and weight requirements. Miniaturization challenges, such as maintaining performance while reducing package size, can limit market growth. In addition, designing and manufacturing automotive-grade passive electronic components require significant research, development, and testing. High development costs limit innovation in the market.

- Environmental concerns, including sustainability and climate change, influence automotive industry trends and regulations. Growing emphasis on ecological sustainability may drive the adoption of vehicles' energy-efficient and environmentally friendly electronic components. Moreover, trade policies, tariffs, and trade agreements can impact the cost and availability of automotive components. Changes in trade policies may disrupt supply chains, affect pricing, and influence market competition.

Automotive Passive Electronic Components Market Trends

Capacitors to Witness Significant Growth

- Advancements in capacitor technology have led to the development of smaller, lighter, and more efficient capacitors. This enables automotive manufacturers to design compact and lightweight electronic systems, reducing overall vehicle weight and improving fuel efficiency. The increasing adoption of ADAS (advanced driver assistance systems), infotainment systems, and automobile connectivity features require robust and reliable electronic components. Capacitors support implementing these features by providing a stable power supply and ensuring the smooth operation of sensors, cameras, and communication modules.

- For instance, in August 2023, TDK Corporation in India (Nasik) was set for business prospects as it has enhanced its capacity. This specific facility in Nashik is growing its production capabilities and has introduced a new structure spanning approximately 23,000 square meters. In the coming four years, more production lines will be established for DC capacitors used in automotive sectors. These capacitors will be manufactured for the local market in India and overseas export. The increase in capacity creates new prospects that will support the company's medium-term growth strategy.

- Stringent government regulations and fuel economy standards drive the demand for energy-efficient automotive systems. Capacitors help optimize energy usage and minimize power losses, aligning with regulator requirements and sustainability goals. Capacitors are integral to the functioning of automotive electronic systems, and the demand is expected to continue growing as vehicle electrification, connectivity, and automation trends accelerate.

- For instance, in May 2024, Hyundai Motor Co. planned to utilize the investment already set aside for the United States to manufacture hybrid vehicles at its EV plant. The third-largest automaker globally, along with affiliate Kia Corp, intends to use funds allocated for EV and battery manufacturing facilities in Georgia to produce hybrid cars. Hyundai Motor Group of South Korea, which includes Hyundai Motor and Kia, announced plans to invest USD 12.6 billion in building new electric vehicle and battery production plants in Georgia, marking its most significant investment outside of South Korea.

Europe to Hold Significant Market Share

- Europe is home to some of the world's largest automotive markets, including the United Kingdom, Germany, and France. Europe accounts for a significant portion of worldwide vehicle production and sales. The rising demand for commercial and passenger vehicles in these countries contributes to the market for passive electronic components used in various automotive systems.

- Europe is experiencing rapid growth in the adoption of electric vehicles (EVs), battery electric vehicles (BEVs), and hybrid electric vehicles (HEVs). European government incentives and technological advancements are driving the shift toward electrified powertrains. This transition increases the demand for passive electronic components such as capacitors, inductors, and resistors used in electric drivetrains, battery management systems, and onboard electronics. For instance, in 2023, electric cars, including both BEV and PHEV, accounted for approximately 4.8& of passenger cars in Germany, as reported by KBA. The proportion of electric vehicles has steadily risen each year within the specified time frame, particularly for BEV models.

- The automotive industry in European countries like the United Kingdom, Germany, and France is at the forefront of innovation, strongly focusing on developing advanced vehicle technologies. This includes the integration of smart features, connectivity solutions, and ADAS. These technologies require various passive electronic components to support functions such as vehicle networking.

- For instance, in November 2023, the United Kingdom government allocated EUR 150 million (USD 189 million) as part of a larger EUR 4.5 billion (USD 5.7 million) investment to support British manufacturing and stimulate economic expansion. This funding is aimed at the connected and automated mobility (CAM) sector up to 2030. The budget allocated to help CAM will be supplemented by industry contributions, which will allow the United Kingdom's Centre for Connected and Autonomous Vehicles (CCAV) to solidify the UK's position as a global leader in the creation, advancement, implementation, and production of self-driving technologies, products, and services.

Automotive Passive Electronic Components Industry Overview

The automotive passive electronic components market is very competitive. The market is highly concentrated due to various small and large players. All the major players account for a significant market share and focus on expanding the global consumer base. Some significant players in the market are Yageo Corporation, Panasonic Corporation, TDK Corporation, Vishay Intertechnology Inc., Taiyo Yuden Corporation, and many more. Companies are increasing their market share by forming multiple collaborations, partnerships, and acquisitions and investing in introducing new products to earn a competitive edge during the forecast period.

March 2024: JF Kilfoil Company expanded its representation of Knowles' products to include the Cornell Dubilier brand in the Midwest market. This partnership was established due to Knowles' acquisition of Cornell Dubilier, which allowed the company to offer a broader range of film, electrolytic, and specialty capacitors. The product range comprises single-layer capacitors, trimmers, aluminum electrolytic capacitors, aluminum polymer capacitors, film capacitors, mica capacitors, and supercapacitors. These items are known for their reliability, longevity, and excellent performance in challenging situations.

September 2023: Knowles Precision Devices acquired Cornell Dubilier for USD 263 million in cash. This acquisition will include film, electrolytic, and mica capacitor products and is anticipated to enhance non-GAAP EPS by 2024. Cornell Dubilier's diverse range of power film, electrolytic, and mica capacitors, combined with Knowles' Precision Devices segment, will offer a valuable proposition and expanded product portfolio to current and potential customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Snapshot

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Usage of Advanced Electronic Devices in the Industry

- 5.1.2 Increasing Preference for Miniaturized Designs

- 5.2 Market Restraints

- 5.2.1 Fluctuating Prices of Critical Metals Used in Manufacturing of Passive Electronic Components/ Challenges in the manufacturing of various Passive Components

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Capacitors

- 6.1.1.1 Ceramic Capacitors

- 6.1.1.2 Tantalum Capacitors

- 6.1.1.3 Aluminum Electrolytic Capacitors

- 6.1.1.4 Paper and Plastic Film Capacitors

- 6.1.1.5 Supercapacitors

- 6.1.2 Inductors

- 6.1.3 Resistors

- 6.1.3.1 Surface-mounted Chips

- 6.1.3.2 Network and Array

- 6.1.3.3 Other Specialty

- 6.1.4 EMC Filters

- 6.1.1 Capacitors

- 6.2 By Geography***

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Middle East and Africa

- 6.2.6 Latin America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Yageo Corporation

- 7.1.2 Panasonic Corporation

- 7.1.3 TDK Corporation

- 7.1.4 Vishay Intertechnology Inc.

- 7.1.5 Taiyo Yuden Corporation

- 7.1.6 Kyocera Corporation (includes AVX Corporation)

- 7.1.7 Knowles Precision Devices

- 7.1.8 Murata Manufacturing Co. Ltd

- 7.1.9 Samsung Electro-Mechanical

- 7.1.10 KOA Corporation

- 7.1.11 Rubycon Corporation

- 7.1.12 Nippon Chemi-Con Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET