Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1645112

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1645112

Global Internal Combustion Engines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 125 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

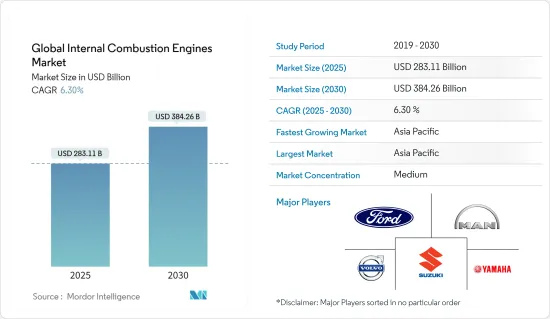

The Global Internal Combustion Engines Market size is estimated at USD 283.11 billion in 2025, and is expected to reach USD 384.26 billion by 2030, at a CAGR of 6.3% during the forecast period (2025-2030).

Key Highlights

- The increasing demand for automobiles and two-wheeler vehicles in Asia-Pacific is expected to drive the market during the forecast period.

- On the other hand, rising demand for non-GHG-emitting vehicles and supportive policies to adopt alternate fuel vehicles are expected to hamper the market's growth.

- Nevertheless, the increasing research & development and technological advancements in the internal combustion engine design are expected to present significant growth opportunities for the market during the forecast period.

- Asia-Pacific is expected to have a significant share of the market due to increasing industrial and commercial activities, which will translate to more vehicle sales during the forecast period.

Global Internal Combustion Engines Market Trends

The Diesel Segment is Expected to Witness Significant Growth

- Diesel engines are among the most significant internal combustion engines that have been in use since the 1870s. These engines are designed to generate mechanical energy after the combustion of an air-diesel mixture. No auxiliary component, such as a spark plug, is used to ignite the air-diesel mixture; instead, the elevating temperature of the air is used, which is compressed by a piston moving inside an engine block.

- These engines were earlier designed to power trains and factories. However, over the years, they have been used in several applications, such as power generation, automotive, construction, and agriculture equipment.

- The significant advantage of diesel engines is that they are more fuel-efficient than gasoline engines. They have fewer components than gasoline engines and, hence, have fewer maintenance issues. Diesel engines provide better acceleration, towing, and hauling potential than gasoline engines. They are designed to handle high compression and hard work and, hence, have a long lifespan.

- With increasing technological innovations in diesel engines to achieve better efficiency, the consumption of diesel is expected to increase over the forecast period. According to the Energy Information Administration, the total diesel consumption in the United States in December 2023 was 3.75 million barrels per day. The consumption is expected to increase with technological innovations in diesel engines.

- In February 2023, Cummins Inc. announced that it would launch the next engine in the fuel-agnostic series (the X10) in North America in 2026. The engine is expected to comply with US EPA's 2027 regulations. The diesel version of the engine is expected to be launched first.

- Thus, owing to the technological developments and increasing consumption of diesel, the segment is expected to witness significant growth.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific has various developing countries, such as India, China, and Japan, where urbanization and industrialization are growing rapidly. With the development of the economies of these countries, the e-commerce division is also increasing, thereby generating the need for internal combustion engines.

- The e-commerce sector has grown significantly in the past five years, mainly driven by the COVID-19 pandemic. E-commerce plays a vital role in people's daily lives. It is redefining commercial activities around the world. Apart from the e-commerce sector, the use of automobiles for traveling and other purposes has increased. As internal combustion engines are used as a primary source of energy in automobiles, an increase in the use of automobiles is expected to drive the demand for internal combustion engines.

- According to International Organization of Motor Vehicle Manufacturers, in 2023, motor vehicle production in Asia-Pacific amounted to 55,115,837 units, an annual growth rate of approximately 10% compared to previous year. Increase in the manufacturing of motor vehicle in the region is expected to increase the demand for internal combustion engines.

- According to an announcement by Carmaker Stellantis in September 2023, internal combustion engine (ICE) vehicles are expected to be on the road until 2050, making it necessary to contain carbon emissions until fully electric ones finally replace them.

- Thus, owing to the developments in the e-commerce segment and the rise in automobile usage, especially in developing countries, Asia-Pacific is expected to dominate the market during the forecast period.

Global Internal Combustion Engines Industry Overview

The global internal combustion engine market is semi-fragmented. Some of the key players in this market include Volvo Ab, Man SE, Yamaha Motor Co. Ltd, Suzuki Motor Corp, and Ford Motor Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50002227

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand for Automobiles

- 4.5.1.2 Increasing Demand for Two-Wheeler Vehicles

- 4.5.2 Restraints

- 4.5.2.1 Rising Demand for Non-GHG Emitting Vehicles

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Capacity

- 5.1.1 50 cm3 to 200 cm3

- 5.1.2 201 cm3 to 800 cm3

- 5.1.3 801 cm3 to 1500 cm3

- 5.1.4 1501 cm3 to 3000 cm3

- 5.2 Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Diesel

- 5.2.3 Others

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Spain

- 5.3.2.3 Russia

- 5.3.2.4 Turkey

- 5.3.2.5 Nordic Countries

- 5.3.2.6 Norway

- 5.3.2.7 Germany

- 5.3.2.8 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Malaysia

- 5.3.3.5 Indonesia

- 5.3.3.6 Thailand

- 5.3.3.7 Vietnam

- 5.3.3.8 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 United Arab Emirates

- 5.3.4.2 Saudi Arabia

- 5.3.4.3 Nigeria

- 5.3.4.4 Qatar

- 5.3.4.5 Egypt

- 5.3.4.6 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Colombia

- 5.3.5.4 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Volvo AB

- 6.3.2 Man SE

- 6.3.3 Yamaha Motor Co. Ltd

- 6.3.4 Suzuki Motor Corp

- 6.3.5 Ford Motor Company

- 6.3.6 Volkswagen Group

- 6.3.7 Toyota Motor Corporation

- 6.3.8 Hyundai Motor Company

- 6.3.9 Ducati Motor Holding SpA

- 6.3.10 Fiat Chrysler Automobiles NV

- 6.4 Market Ranking/Share (%) Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Increasing Research & Development and Technological Advancements in the Internal Combustion Engine Design

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.