Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1645101

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1645101

Southeast Asia Hydrogen Generation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 110 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

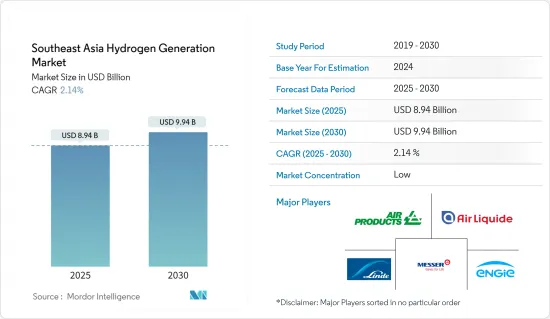

The Southeast Asia Hydrogen Generation Market size is estimated at USD 8.94 billion in 2025, and is expected to reach USD 9.94 billion by 2030, at a CAGR of 2.14% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as supportive government policies and regulations for desulphurization, greenhouse gas emissions, and encouraging the production and consumption of hydrogen are likely to drive the hydrogen generation market in the Southeast Asian region during the forecast period.

- On the other hand, the high production costs of hydrogen energy storage are expected to restrain the growth of hydrogen generation.

- Nevertheless, technological advancements in extracting hydrogen from renewable sources including nuclear, wind, solar, biomass, hydro, and geothermal coupled with the rising applications of hydrogen as a fuel, are poised to unlock lucrative growth opportunities for the hydrogen generation market in the years ahead.

- Indonesia is expected to witness significant growth in the Southeast Asian hydrogen generation market during the forecast period. Owing to to supportive goverment policies and investments.

Southeast Asia Hydrogen Generation Market Trends

Green Hydrogen is a Significant Segment

- Green hydrogen is produced through a process called electrolysis, which uses electricity to split water into hydrogen and oxygen. The electricity used in this process comes from renewable sources such as wind, solar, or hydropower. This ensures that the hydrogen produced is genuinely "green" and has minimal carbon emissions.

- In 2023, the region's hydrogen production reached approximately 3.6 million tons. This hydrogen was predominantly utilized in refining processes and the synthesis of chemicals like ammonia and methanol. Notably, almost all of this hydrogen was produced via natural gas steam reforming, which did not incorporate carbon capture, utilization, and storage (CCUS) technology.

- Significant investments evidence the ambitious outlook for green hydrogen in Southeast Asia. For instance, in October 2024, TTCL Public Company Limited secured a THB 1.2 billion contract to establish a green hydrogen plant in Laos. This project aims to enhance Laos's hydrogen production capacity using renewable energy.

- Further, in February 2024, Malaysia's largest green hydrogen project, a 60MW plant in Perak state powered by floating solar, secured 1.88 billion ringgit (USD 393.6 million) from private investors. This kind of investments highlights the rising demand for the green hydrogen market in the Southeast Asia region.

- The region's attempt to minimize emissions, mainly from heavy industries like petrochemicals, iron and steel, and power generation, are resulting in measures to exceed green hydrogen production and usage. As a result, investments in green hydrogen infrastructure are accelerating, and collaborative projects are emerging across Southeast Asia. This momentum is expected to significantly contribute to the region's decarbonization goals and energy transition efforts.

- In October 2024, Senoko Energy and Gentari signed an MoU to explore importing hydrogen gas from Malaysia to Singapore, aiming to integrate it into Senoko's gas turbine assets by 2029. This collaboration seeks to reduce carbon emissions significantly, supporting Singapore's 2050 Net Zero target.

- Moreover, In 2023, Meranti, a steel manufacturer, announced plans to build Southeast Asia's first green flat steel plant in Thailand. The plant will use hydrogen to replace coal and employ electric arc furnace technology powered by renewable energy to produce green steel. Expected to be operational by 2027, the facility will have an annual production capacity of 2 million tons, reducing carbon emissions by 4 million tons annually.

- According to International Renewable Energy Agency (IRENA) In 2023, Southeast Asia saw significant renewable energy capacities, with Vietnam leading at 46,012 MW, followed by Thailand at 12,547 MW, Malaysia at 9,052 MW, the Philippines at 7,832 MW, and Singapore at 1,147 MW. This substantial renewable energy infrastructure provides a strong foundation for green hydrogen production.

- Therefore, owing to such factors, the green hydrogen segment is likely to significantly impact the hydrogen generation market during the forecast period.

Indonesia to Witness Significant Growth

- As Indonesia pivots towards renewable energy to achieve its net-zero emissions goal by 2060, hydrogen energy is emerging as a focal point. With its abundant resources and strategic positioning, Indonesia is poised to become a regional leader in hydrogen production, particularly in green hydrogen, which is derived from renewable sources.

- According to the findings in the Indonesia Hydrogen Energy Outlook 2024, by 2060, Indonesia's hydrogen demand is expected to increase to around 2 million tonnes per annum (MTPA) due to the increasing demand for Ammonia.

- According to the World Steel Association, Indonesia's steel production has steadily increased from 8.56 million tonnes in 2019 to 16.8 million tonnes in 2023. This rising steel production underscores the growing industrial demand, which drives the need for hydrogen, mainly green hydrogen, as a cleaner alternative to traditional fossil fuels.

- Indonesia is shifting its focus to renewable energy in pursuit of its net-zero emissions target for 2060. Central to this transition is hydrogen energy. Leveraging its rich resources and advantageous location, Indonesia is on track to establish itself as a regional powerhouse in hydrogen production, especially green hydrogen sourced from renewables.

- For instance, in October 2024, Sembcorp Industries, through its subsidiary Sembcorp Utilities Pte Ltd, signed an agreement with PT PLN Energi Primer Indonesia to establish a green hydrogen production facility in Sumatra, Indonesia. This facility will produce 100,000 metric tonnes annually, making it Southeast Asia's largest green hydrogen initiative. The project aims to create a regional green hydrogen hub connecting Sumatra, the Riau Islands, and Singapore.

- In October 2024, PT Pertamina Power Indonesia ("Pertamina NRE"), PT Pertamina Geothermal Energy Tbk ("PGE"), and Genvia solidified their partnership by signing a Memorandum of Understanding (MoU). Their collaboration centers on green hydrogen production, utilizing advanced solid oxide electrolyzer (SOEL) technology alongside geothermal heat sources. The MoU includes a technical and economic assessment of Genvia's state-of-the-art high-temperature SOEL technology, with the goal of optimizing energy consumption in green hydrogen production.

- Additionally, PT Kilang Pertamina Internasional planned to construct a blue ammonia facility in Bintuni Bay, West Papua Province. The plant is expected to commence operations in 2030, aiming for a blue ammonia production capacity of around 875,000 TPA (tons per annum) of blue ammonia, which is expected to create a demand for blue hydrogen of around 150,000 TPA. The facility is designed to process 90 million standard cubic feet per day (MMSCFD) of natural gas.

- Therefore, based on the above-mentioned factors, Indonesia is expected to witness significant growth in the Southeast Asia hydrogen generation market during the forecast period.

Southeast Asia Hydrogen Generation Industry Overview

The Southeast Asia hydrogen generation market is consolidated. Some of the major players in the market (in no particular order) include Linde PLC, Messer Group GmbH, Air Liquide SA, Air Products and Chemicals Inc., Engie SA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50002211

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand From Refining And Industrial Sector

- 4.5.1.2 Favourable Government Policies

- 4.5.2 Restraints

- 4.5.2.1 High Capital Costs For Hydrogen Energy Storage

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Source (Qualitative Analysis)

- 5.1.1 Blue Hydrogen

- 5.1.2 Green Hydrogen

- 5.1.3 Grey Hydrogen

- 5.2 Technology

- 5.2.1 Steam Methane Reforming (SMR)

- 5.2.2 Coal Gasification

- 5.2.3 Other Technologis

- 5.3 Application

- 5.3.1 Oil Refining

- 5.3.2 Chemical Processing

- 5.3.3 Iron & Steel Production

- 5.3.4 Other Applications

- 5.4 Geography

- 5.4.1 Indonesia

- 5.4.2 Malaysia

- 5.4.3 Vietnam

- 5.4.4 Singapore

- 5.4.5 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Linde Plc

- 6.3.2 Air Liquide SA

- 6.3.3 Messer Group GmbH

- 6.3.4 Engie S.A.

- 6.3.5 Cummins Inc.

- 6.3.6 Air Products and Chemicals Inc.

- 6.3.7 Taiyo Nippon Sanso Holding Corporation

- 6.3.8 Enapter S.r.l.

- 6.4 Market Ranking/ Share Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.