PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521686

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521686

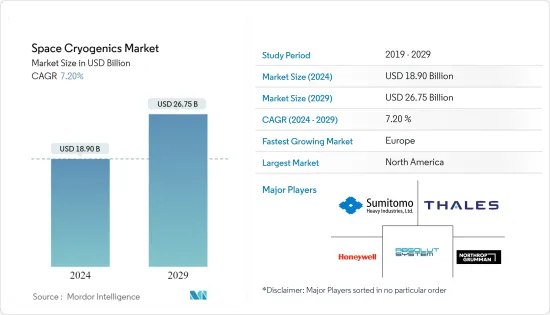

Space Cryogenics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Space Cryogenics Market size is estimated at USD 18.90 billion in 2024, and is expected to reach USD 26.75 billion by 2029, growing at a CAGR of 7.20% during the forecast period (2024-2029).

The space cryogenics market growth can be attributed to the increasing simplicity of operations in onboard spacecraft. With space missions becoming more complex, the demand for cryogenic systems that can deliver reliable performance over extended periods is growing.

Advancements in cryogenic technologies are leading to the development of more robust and efficient cryogenic systems to withstand harsh space conditions. Advancements and developments in cryogenic devices, such as sensors and cold electronics in space-based applications, are driving market growth.

Cryogenic sensors and cold electronics are devices that benefit from the development of materials science. Substantial financial investments are required for the development, testing, and deployment of cryogenic infrastructure, which includes storage tanks, insulation, transfer systems, and cooling mechanisms. Hence, high operating expenses and capital expenditures required for cryogenic setups are major factors hindering the growth of the space cryogenics market.

Space Cryogenics Market Trends

The Space Science Missions Segment will Account for the Highest Market Share During the Forecast Period

The space science missions segment is expected to account for the largest share of revenue over the forecast period, owing to the increasing use of cryogenics in space missions. Globally, space organizations have been taking the initiative to launch satellites, rockets, and others. For instance, in May 2023, a second-generation navigation satellite that utilizes a GSLV rocket with a cryogenic upper stage was successfully launched by the Indian Space Research Organization (ISRO). The NVS-01 will supplement the country's regional navigation system by delivering precise and real-time navigation.

In November 2022, the American space agency, NASA, launched the Artemis-1 mission at Florida's Kennedy Space Center. During the launch, the core stage engines shut down eight minutes after liftoff and separated from the rest of the rocket. After this, the Interim Cryogenic Propulsion Stage (ICPS) was used to propel the Orion spacecraft. The four solar panels of the Orion spacecraft were deployed by NASA. Orion decoupled from the ICPS and completed 'translunar injection.' It is now traveling toward the lunar orbit. Such developments are expected to lead the segment during the forecasted years.

Europe will Witness the Highest Growth During the Forecast Period

In the space cryogenics market, Europe is projected to witness the highest growth as a result of the ongoing and planned space initiatives during the forecast period. For instance, to ensure that the United Kingdom leads the creation of a space telescope to study exoplanets, in 2022, the UK government announced an investment of USD 31.05 million. With this funding, the country is envisioned to continue leading the mission's scientific operations and data processing while also receiving the payload module, cryogenic cooler, and optical ground support equipment for Ariel.

In July 2023, the French parliament approved a seven-year military spending program for 2024-2030 that includes USD 6.7 billion for space programs, which is a 45% increase from the previous period. In September 2023, the German government presented a new Space Strategy and laid its goals and opportunities for space travel until 2030.

In October 2023, the UK Space Agency and a US spaceflight services company, Axiom Space, signed an initial agreement as they bid to send British astronauts into orbit for two weeks. The mission with the UK would be commercially sponsored and supported by the European Space Agency. Hence, increasing activities in the space industry in this region are leading to a rise in demand for space cryogenics, which is expected to drive growth in market revenue.

Space Cryogenics Industry Overview

The space cryogenics market is consolidated, with leading players having the highest market share. Some of the key market players include THALES, Northrop Grumman Corporation, Absolut System, Sumitomo Heavy Industries Ltd, and Honeywell International Inc.

These companies are leaders in cryogenic technology and suppliers of cryogenic coolers. Companies are investing in the R&D of cryogenic systems that offer automated controls, remote monitoring, and maintenance capabilities to help streamline spacecraft operations and reduce the risk of human error. By reducing the complexity of cryogenic systems and enhancing their ease of use, spacecraft operators can focus on mission objectives rather than intricate system management.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Cooling Type

- 5.1.1 High-Temperature Coolers

- 5.1.2 Low-Temperature Coolers

- 5.2 By Application

- 5.2.1 Earth Observation

- 5.2.2 Telecom Applications

- 5.2.3 Technology Demonstration Missions

- 5.2.4 Cryo-Electronics Applications

- 5.3 By Temperature

- 5.3.1 Less Than 120 K

- 5.3.2 120 K

- 5.3.3 More Than 150K

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Russia

- 5.4.2.4 France

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of Latin America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Israel

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 THALES

- 6.2.2 Absolut System

- 6.2.3 Sumitomo Heavy Industries Ltd

- 6.2.4 Air Liquide

- 6.2.5 Oxford Instruments

- 6.2.6 Parker Hannifin Corporation

- 6.2.7 Honeywell International Inc.

- 6.2.8 RICOR

- 6.2.9 Creare

- 6.2.10 Northrop Grumman Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS