PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1645079

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1645079

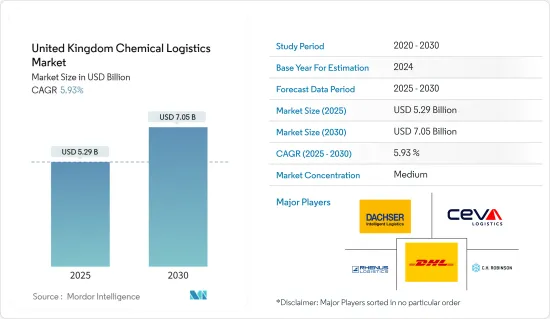

United Kingdom Chemical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The United Kingdom Chemical Logistics Market size is estimated at USD 5.29 billion in 2025, and is expected to reach USD 7.05 billion by 2030, at a CAGR of 5.93% during the forecast period (2025-2030).

There are strict legal requirements for chemical logistics operations in the United Kingdom. Directive 2001/45/EEC of the European Parliament and of the Council of 27 June 2001, which amends Council Directive 89 /655 / EEC on the minimum health and safety requirements for the application of work equipment to workers at work. (Second individual Directive under Article 16 (1) of Council Directive 89 /391 / EEC).

According to industry experts, the revenue from chemicals and chemical products is set to increase by USD 9.28 billion in 2023 up to USD 9.56 billion in 2024 for the category of soap and detergents, perfumes, cleaners, and polishings or toilet preparations.

The value added in the UK chemicals market is reported to amount to USD 12.76 billion in 2024 from USD 12.28 billion in 2023. Innovation and technical progress are frequent drivers of the chemicals sector. Investing in R&D and introducing new and improved products or processes can increase the value added by companies in the United Kingdom chemical market.

United Kingdom Chemical Logistics Market Trends

The Impact of Brexit on Trade with the United Kingdom

Chemical products imported into the United Kingdom have severely declined, indicating an effect of Brexit. According to industry experts, while transactions worth USD 13.22 billion were done in 2021, only USD 10.02 billion was done in 2022. The country saw a decline of almost 24% in the period.

Business transactions between China and the UK have taken a turn. The import value of chemical products has fallen sharply from USD 6.0 billion in 2021 to USD 2.95 billion in 2022.

The United Kingdom's exports to non-EU countries, particularly to the United States, have performed poorly. Partially, this is due to the United Kingdom being in a weaker position to benefit from increased demand, as it seems to be declining mainly in non-exporting markets. The export value of miscellaneous chemical products to the United States has fallen from USD 1.25 billion in 2021 to USD 1.11 billion in 2022.

Chemical Consumption in the United Kingdom

The United Kingdom's import value of fertilizers has been rising, indicating the country's consumption of chemicals and the need for logistics. According to Statista, in 2022, the United Kingdom imported USD 2.62 billion worth of fertilizers.

Croda International Plc is the largest chemical company in the United Kingdom in terms of revenue, followed by Johnson Matthey Plc. According to industry experts, their 2022 net income in the United Kingdom was GBP 193.9 million (USD 244.12 million) and GBP 177 million (USD 222.84 million), respectively. This indicates the value of the country's consumption of chemicals.

Also, in November 2023, LyondellBasell, a supplier of polyolefins in the chemical industry, announced that it is setting up a new distribution center for its grades in the United Kingdom. As part of their commitment to improve the customer experience by placing stocks in customers' facilities, which reduces lead times for orders, this strategic move is a continuation of these efforts. This distribution hub in the United Kingdom is an integral part of LyondellBasell's global footprint.

United Kingdom Chemical Logistics Industry Overview

The market for chemical logistics in the United Kingdom is competitive, owing to the presence of various companies. The e-commerce logistics market in the United Kingdom is moderately fragmented and depicts competition among the market players. The competitive landscape is dynamic, with ongoing developments and competition driving companies to adapt to emerging trends, technological progress, and changing consumer preferences. Global logistics giants such as DHL have a strong presence, providing a range of services from express delivery to supply chain management. However, the chemical logistics industry in the United Kingdom has relatively high entry barriers due to stringent regulations and strict safety and environmental standards. DHL International Gmbh, Dachser, and Rhenus Logistics are among the most important players in this sector.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Industry Value Chain Analysis

- 4.4 Government Regulations and Initiatives

- 4.5 Insights into the 3PL

- 4.6 Value Chain / Supply Chain Analysis

- 4.7 Demand and Supply Analysis

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.1.1 Adherence to Stringent Regulations

- 5.1.2 Globalization of Supply Chains

- 5.2 Restraints

- 5.2.1 Environmental Concerns

- 5.3 Opportunities

- 5.3.1 Green Logistics

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers / Buyers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Transportation

- 6.1.2 Warehousing, Distribution, and Inventory Management

- 6.1.3 Consulting & Management Services

- 6.1.4 Customs & Security

- 6.1.5 Green Logistics

- 6.1.6 Other Services

- 6.2 By Mode of Transportation

- 6.2.1 Roadways

- 6.2.2 Railways

- 6.2.3 Airways

- 6.2.4 Waterways

- 6.2.5 Pipelines

- 6.3 By End User

- 6.3.1 Pharmaceutical Industry

- 6.3.2 Cosmetic Industry

- 6.3.3 Oil and Gas Industry

- 6.3.4 Specialty Chemicals Industry

- 6.3.5 Other End Users

7 COMPETITIVE LANDSCAPE

- 7.1 Overview (Market Concentration and Major Players)

- 7.2 Company Profiles

- 7.2.1 DHL

- 7.2.2 DACHSER

- 7.2.3 Rhenus Logistics

- 7.2.4 C.H. Robinson

- 7.2.5 CEVA Logistics

- 7.2.6 Den Hartogh

- 7.2.7 BDP International

- 7.2.8 Streamline Shipping

- 7.2.9 Hoyer Group

- 7.2.10 Suttons Group*

- 7.3 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX