PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521590

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521590

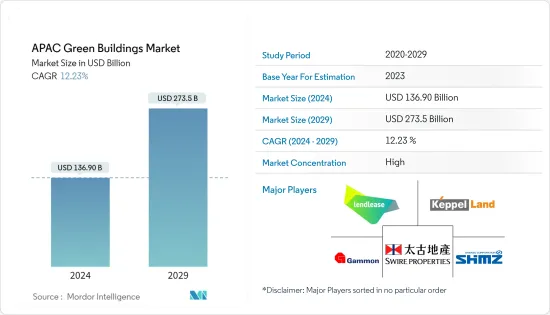

APAC Green Buildings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The APAC Green Buildings Market size is estimated at USD 136.90 billion in 2024, and is expected to reach USD 273.5 billion by 2029, growing at a CAGR of 12.23% during the forecast period (2024-2029).

Key Highlights

- The Asia-Pacific region is home to 60% of the world's 4.3 billion inhabitants, with over 2 billion living in cities. The region is home to 16 out of the 28 world's largest cities (10 million or more people in each city), and the urban population is projected to grow to 3.3 billion by 2050.

- With the growing population, there is a demand for new buildings. Developing low and net zero carbon (NCC) buildings is key to improving people's quality of life, reducing environmental impact, and increasing economic opportunities. Green Building Councils are responding to the challenges and opportunities they face on the ground across the Asia-Pacific Region (APR).

- In most South and Southeast Asian countries, there are mandatory energy efficiency and environmental rating schemes in addition to voluntary schemes. For example, in India, the Energy Conservation Building Code of 2017 and in Sri Lanka, the Energy Building Code of 2020 set energy efficiency and renewable energy use standards.

- Both aim to accelerate the transition to green, energy-efficient buildings. In some cases, the two mechanisms work together to leverage each other's capabilities and resources to increase the multiplier effect in the construction sector. The current certification systems include the GRIHA certification in India, the Green Mark certification in Singapore, and the Greenship certification in Indonesia.

- The sector has evolved significantly since the first set of standards. The latest set of mandatory and optional building standards is putting pressure on the industry to accelerate the transition to net-zero. Net-Zero buildings in South & Southeast Asia include the Indira Paryavaran Bhawan Office building in New Delhi, India Bayalpata Hospital in Nepal, Nepal nzeb@sede campus building in Singapore Uni Kl British Malaysia Institute in Malaysia net zero buildings in South and Southeast Asia.

APAC Green Buildings Market Trends

The Commercial Segment's Increasing Demand for Green Buildings

According to the report, green certifications for buildings have increased five-fold since 2010, reflecting the growing awareness of green certifications amongst developers and occupiers alike.

There are regional variations in green certifications as well. For example, in Q3 2023, it was found that Bengaluru had the highest percentage of green-certified buildings, followed by Hyderabad and Chennai, with nearly three out of every five certified assets.

India had approximately 691 million square feet of Grade A office stock in Q3 2023, of which 61% have at least one Green Certification.

Retrofitting skills will be a key part of the transformation of the sector. With over half of the region's premium office space having been built before 2011, there's plenty of scope to modify existing buildings or retrofit them.

For example, refurbishing existing buildings sustainably to improve their efficiency - known as green retrofitting - could be a great way to improve the performance of existing buildings, helping to reduce energy consumption and carbon emissions.

APAC cities are facing a shortage of sustainable office buildings. Hong Kong's demand for high-quality, green office space is expected to reach its highest level in two years, resulting in a significant supply shortage. A shortage of 84% of low-carbon office space in Sydney by 2028 is expected. This imbalance between demand and supply is hindering the decarbonization of the sector.

India is Dominating the Market

The construction of green buildings is now common in most of the region due to its various advantages, such as lower energy consumption and lower maintenance and operating costs. Governments, especially in developing countries, are introducing new initiatives and policies to promote green construction.

With the rapid growth of commercialization, industrialization, and urbanization in developing countries, the green building industry has lucrative opportunities. According to the IFC, green buildings can be viewed as a key low-carbon and sustainable investment opportunity in developing countries.

Southeast Asia's leading companies are setting science-driven goals and working together across value chains to create a green economy for the future. Bilateral agreements and new infrastructure are laying the groundwork for global and regional carbon markets, intending to preserve and restore the region's ecosystems.

With 10 million new homes being built every year, India offers tremendous opportunities for green building development, both in the residential and commercial sectors. Today, more than 40% of India's commercial Grade A office inventory is green-certified, and this percentage is expected to increase to more than 50% over the next decade, in line with global ESG trends. The BRSR framework mandated by the Securities and Exchange Board of India (SEBI) mandates ESG disclosure in order to promote transparency and accountability for sustainable practices.

APAC Green Buildings Industry Overview

The green building market has become increasingly competitive, with countries and companies recognizing the importance of sustainability and energy efficiency. Several key players have emerged in this market, each offering unique solutions and services to meet the growing demand for green buildings.

One of the major players in the market is the construction industry itself. Many construction companies have embraced green building practices and incorporated sustainable design principles into their projects. These companies often work closely with architects, engineers, and other professionals to ensure that their buildings meet the highest sustainability standards. Some of the major players in the market include Lendlease Keppel Land, Shimizu Corporation, Swire Properties, Gammon Construction, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Insights on Supply Chain/Value Chain Analysis of the Green Buildings Industry

- 4.4 Brief on Different Structures Used in the Green Buildings Industry

- 4.5 Cost Structure Analysis of the Green Buildings Industry

- 4.6 Impact of COVID 19 on the Market

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.1.1 Energy Efficiency in Construction Driving the Market

- 5.1.2 Flexibility and Customization Options Driving the Market

- 5.2 Restraints

- 5.2.1 Limited Availability of Suitable Land for Construction Hindering the Market

- 5.2.2 Lower Quality Compared to Traditional Construction

- 5.3 Opportunitites

- 5.3.1 Demand Across Various Sectors Driving the Market

- 5.3.2 Energy Efficient Construction Driving the Market

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers / Buyers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Exterior Products

- 6.1.2 Interior products

- 6.1.3 Other Products ( Building Systems, Solar Systems, Etc.)

- 6.2 By End User

- 6.2.1 Residential

- 6.2.2 Office

- 6.2.3 Retail

- 6.2.4 Institutional

- 6.2.5 Other End Users

- 6.3 By Geography

- 6.3.1 China

- 6.3.2 Japan

- 6.3.3 India

- 6.3.4 Australia

- 6.3.5 South Korea

- 6.3.6 Rest of APAC

7 COMPETITIVE LANDSCAPE

- 7.1 Overview (Market Concentration and Major Players)

- 7.2 Company Profiles

- 7.2.1 Lendlease

- 7.2.2 Keppel Land

- 7.2.3 Shimizu Corporation

- 7.2.4 Swire Properties

- 7.2.5 Gammon Construction

- 7.2.6 Sino Group

- 7.2.7 WSP

- 7.2.8 CapitaLand

- 7.2.9 Obayashi Corporation

- 7.2.10 Sun Hung Kai Properties*

- 7.3 Other Companies

8 FUTURE OF THE MARKET

9 APPENDIX