PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521419

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521419

Commercial Aircraft Disassembly - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

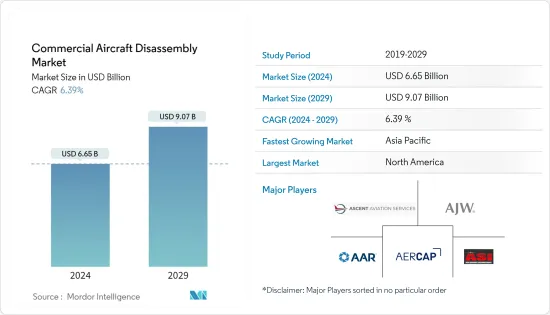

The Commercial Aircraft Disassembly Market size is estimated at USD 6.65 billion in 2024, and is expected to reach USD 9.07 billion by 2029, growing at a CAGR of 6.39% during the forecast period (2024-2029).

Key Highlights

- According to Oliver Wyman's MRO outlook, the average age of commercial aircraft will decline dramatically over the next decade as airlines renew their fleets with more fuel-efficient models. This will drive average annual retirements to increase by 20-25% compared to the previous decade.

- With the aviation industry aiming at utilizing sustainable efforts, the recycling of aircraft parts from end-of-life aircraft is becoming increasingly popular. Engine MRO service providers and leasing companies are witnessing an increasing demand for some types of older engines in their portfolios, such as the Rolls-Royce Trent 700 and the Airbus A330 Powerplant, owing to lower fuel prices that have encouraged airlines to fly their aircraft for longer durations.

- However, the use of expensive alloys in the recycling process increases the overall cost of the process, which is a challenge to the market growth.

Commercial Aircraft Disassembly Market Trends

Narrow Body Segment to Dominate Market Share During the Forecast Period

- Narrow body segment is expected to hold the largest market share primarily due to the airlines' widespread use of narrow-body aircraft for both short and medium-haul routes. Advanced capabilities coupled with various other advantages such as low cost of operation and fuel efficiency in short-haul routes have led to narrow-body aircraft being the most preferred type of aircraft to be used by various low-cost carrier companies worldwide.

- Moreover, the success of the low-cost carrier business model has generated a massive demand for newer-generation narrow-body aircraft in recent years due to their advantages. Technological advancements in newer-generation narrow-body aircraft are making it possible to fly longer distances. Boeing's B737 and Airbus A320 are two of the most-sold aircraft narrow body aircraft.

- For instance, in December 2022, Air India announced that they are close to completing a deal to order more than 200 Boeing aircraft, which includes 190 narrowbody Boeing B737 MAX aircraft, as a part of a historic fleet expansion that will be split with Airbus. The return of the Boeing B737 MAX into service in late 2020 will also help the growth of the narrow-body segment.

Asia-Pacific to Witness Highest Growth During the Forecast Period

- The robust economic growth, favorable population, and demographic profiles of the populace in developing countries in the Asia-Pacific region are driving the air passenger traffic in the region. The region has seen a significant increase in air passenger traffic during the past decade, mostly due to the tourist destinations in the region and the ease of access to air travel, which is expected to continue during the forecast period.

- In addition to China and India, which are two of the largest aviation markets in the world, countries like Indonesia, Vietnam, Thailand, and the Philippines are experiencing an unprecedented increase in air passenger traffic from tourists exploring cheaper holiday locations.

- As airlines in this region modernize their fleets, demand for aircraft disassembly and recycling services is expected to rise. For instance, in September 2022, China Airlines announced that they had finalized an order for up to 24 Boeing B787 Dreamliners, as the carrier looks forward to continuing to upgrade its fleet with more modern and fuel-efficient airplanes.

- According to the Airbus Outlook, 2320 aircraft will retire between 2023 and 2042 in China as a result of continuous fleet modernization. Thus, such modernizing efforts will create growing market opportunities to reuse, repair, and recycle older aircraft and contribute to a circular economy.

Commercial Aircraft Disassembly Industry Overview

The commercial aircraft disassembly market is consolidated with a handful of players owing the major market share. The major players operating in the commercial aircraft disassembly, dismantling & recycling market are Ascent Aviation Services, A J Walter Aviation Ltd., AAR, AerCap Holdings N.V., and Air Salvage International Ltd.

These major players operating in this market have adopted various strategies comprising mergers and acquisitions, investment in R&D, collaborations, partnerships, regional business expansion, and new product launches. Collaborative partnerships between aircraft manufacturers, airlines, recycling companies, and regulatory bodies have emerged as a driving force behind the expansion of the commercial aircraft disassembly, dismantling, and recycling market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Disassembly and Dismantling

- 5.1.2 Recycling and Storage

- 5.1.3 Used Serviceable Material

- 5.1.4 Rotable Parts

- 5.2 By Aircraft Type

- 5.2.1 Narrow-body Aircraft

- 5.2.2 Wide-body Aircraft

- 5.2.3 Regional Jets

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Israel

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Ascent Aviation Services

- 6.2.2 A J Walter Aviation Limited

- 6.2.3 AAR

- 6.2.4 AerCap Holdings N.V.

- 6.2.5 AerSale, Inc.

- 6.2.6 Air Salvage International Ltd

- 6.2.7 Aircraft End-of-Life Solutions AELS

- 6.2.8 Magellan Aerospace

- 6.2.9 CAVU Aerospace Inc.

- 6.2.10 China Aircraft Leasing Group Holdings Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS