PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1641903

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1641903

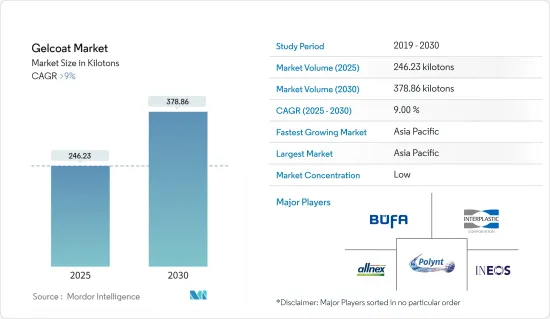

Gelcoat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Gelcoat Market size is estimated at 246.23 kilotons in 2025, and is expected to reach 378.86 kilotons by 2030, at a CAGR of greater than 9% during the forecast period (2025-2030).

The COVID-19 pandemic is expected to impact the Gelcoat Market in 2020 and 2021, driven by reduced economic and commercial activities. Declines in construction and industrial output will keep demand low, but recovery is anticipated with revived trade and government guidelines.

Key Highlights

- Growing demand for gelcoat in the automotive and transportation industry is set to drive market growth. This sector dominated the gelcoat market due to automakers' efforts to produce lightweight vehicles with composites, aligning with government guidelines for improved fuel efficiency and reduced carbon dioxide (CO2) emissions. Gelcoats are key to enhancing the aesthetics of these composite components.

- Polyester Gelcoats are extensively used in various industries, particularly in the transportation and marine sectors. Their popularity in the marine industry is due to their excellent properties, including water resistance, UV protection, and corrosion resistance. This rising demand for polyester gelcoats contributes to market growth.

- Styrene, the predominant monomer in polyester resin-based gelcoats, has raised safety and health concerns due to its extensive use. This poses challenges for market expansion as many governments have implemented strict regulations to reduce styrene emissions from gelcoats and resins, consequently limiting market growth in the forecast period.

- Asia-Pacific dominated the Gelcoat Market across the globe with the largest consumption in a country such as India, China, etc.

Gelcoat Market Trends

Automotive and Transportation (including Aerospace and Marine) segment to lead the Market

- As per OICA, the Global Automotive Industry is currently growing at a substantial rate of 6% in 2022 over 2021. In 2022, various developed and developing countries across the world, including China, Germany, South Korea, Canada, the United Kingdom, and Italy, experienced an increase in automotive production. In 2022, over 85 Million Units of Motor vehicles were manufactured.

- The National Marine Manufacturers Association (NMMA) reports that the recreational boating industry in the U.S. generated an estimated US230.3 billion in sales in 2022.

- According to Invest India, during January 2021, a total of 161 projects in the marine industry, at a cost of US$12 billion, have been completed, and 178 projects at a cost of INR 1,96,578 Crores (US$ 26,595 million) are under implementation.

- As per IATA, it expects a year-over-year increase in total revenues of 9.7% to reach USD 803 Billion in 2023. This marks the first instance of industry revenues surpassing the USD 800 Billion threshold since 2019 when it reached USD 838 Billion. The growth in expenses is projected to be limited to an 8.1% annual rise.

- All these factors are likely to rapidly drive the market during the forecast period.

Asia-Pacific Region to Dominate the Gelcoat Market

- Asia-Pacific region dominated the global market share. The increasing investments and production in end-user industries, aerospace, automotive, marine, construction, etc, are driving the demand for Gelcoat Market in the region.

- A consortium involving Toshiba, Hitachi, Zosen Corp, and JFE Steel is set to construct the world's largest offshore wind farm off the Fukushima coast in Japan. This project, featuring as many as 143 floating turbines and expected to become operational after 2025, is likely to boost the demand for gelcoats.

- Moreover, the Indian Ministry of New and Renewable Energy (MNRE) has set targets for offshore wind installations, aiming for 30 GW by 2030. The use of an in-mold stable gelcoat is frequently required for the protective coating on blades, as well as wind and tidal turbine rotor blades

- According to Lloyd's Register, by 2030, China is poised to become a prominent maritime powerhouse in the shipping industry. To accomplish this, China plans to construct 40 cruise ships, with a portion intended for the domestic market and others for international markets, during this period.

- At the I2U2 Summit, the leaders disclosed that the UAE will allocate $2 billion for the establishment of a network of comprehensive food parks throughout India. Additionally, the group has confirmed its intention to move forward with a hybrid renewable energy project in India's Gujarat State. This initiative will encompass 300 megawatts (MW) of wind and solar capacity, enhanced by a battery energy storage system.

- As per Invest India, the construction industry in India is expected to reach USD 1.4 Trillion by 2025, and the construction industry in India works across 250 sub-sectors with linkages across sectors and over 54 global innovative construction technologies identified under a Technology Sub-Mission of PMAY-U to start a new era in Indian Construction Sectors.

- Furthermore, the rapidly growing construction industry, primarily in China, is a major factor driving the demand for gelcoat in the construction industry.

Gelcoat Industry Overview

The Gelcoat Market is fragmented in nature. The major players (not in any particular order) include Allnex GMBH, INEOS, Polynt S.p.A., Interplastic Corporation, and BUFA Composite Systems GmbH & Co. KG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Surge in the Construction Industry

- 4.1.2 Increasing Demand in the Automotive and Transportation Industry

- 4.1.3 High Utilization of Polyester-Based Gelcoat

- 4.1.4 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Government Regulations for Gelcoat Manufacturers

- 4.2.2 Transition to Closed Molding Processes

- 4.2.3 Cracking Issues in Gelcoat

- 4.2.4 Other Restraints

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Resin Type

- 5.1.1 Polyester

- 5.1.2 Epoxy

- 5.1.3 Vinyl Ester

- 5.1.4 Others

- 5.2 End-User Industry

- 5.2.1 Marine

- 5.2.2 Automotive and Transportation

- 5.2.3 Construction

- 5.2.4 Wind Energy

- 5.2.5 Healthcare

- 5.2.6 Food and Beverage

- 5.2.7 Electrical and Electronics

- 5.2.8 Others (Aerospace. Retail)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)** /Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Allnex GMBH

- 6.4.4 Ashland

- 6.4.5 Atul Ltd

- 6.4.6 Bang & Bonsomer

- 6.4.7 BUFA Composite Systems GmbH & Co. KG

- 6.4.8 Eastman Chemical Company

- 6.4.9 GRP Factors Ltd

- 6.4.10 Gurit Services AG

- 6.4.11 HK Research Corporation

- 6.4.12 INEOS

- 6.4.13 Interplastic Corporation

- 6.4.14 LyondellBasell Industries Holdings B.V.

- 6.4.15 Poliya

- 6.4.16 Polynt S.p.A.

- 6.4.17 Reichhold LLC

- 6.4.18 Scott Bader Company Ltd.

- 6.4.19 Seahawkpaints.com

- 6.4.20 Sika AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand in the Wind Energy and Aerospace Sectors

- 7.2 Increasing Innovations in the Coatings Sector