PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851421

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851421

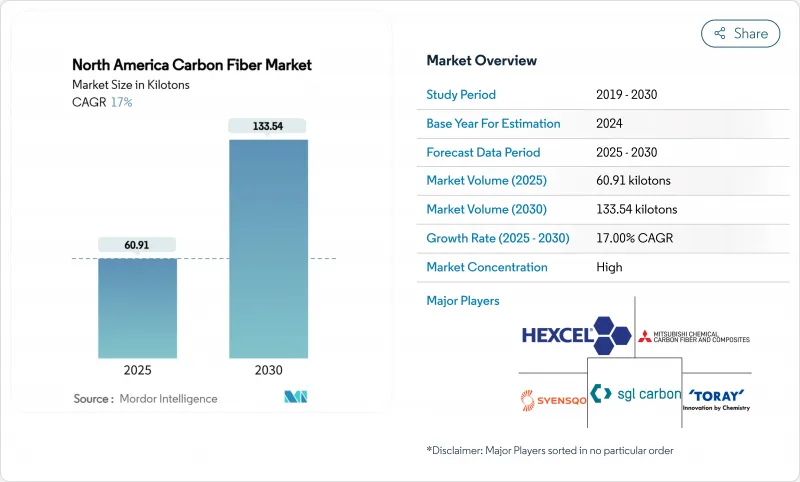

North America Carbon Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The North America Carbon Fiber Market size is estimated at 60.91 kilotons in 2025, and is expected to reach 133.54 kilotons by 2030, at a CAGR of 17% during the forecast period (2025-2030).

Demand rises as aerospace production recovers, electric-vehicle makers cut curb weight and renewable-energy firms build longer wind blades. Polyacrylonitrile (PAN) continues to lead raw-material supply, yet fast-growing petroleum-pitch alternatives signal price-driven substitution. Recycled fibers gain traction because automakers and wind-turbine OEMs seek lower life-cycle emissions. United States output expansions by Hexcel and Toray improve local availability, but precursor sourcing and capital intensity still pose risk. Competitive success now depends on diversified end-use portfolios, agile production lines and close customer integration, rather than reliance on legacy aerospace volumes.

North America Carbon Fiber Market Trends and Insights

Rising Demand from Lightweight Vehicles

Automotive electrification positions the North America carbon fiber market at the center of new lightweight strategies. Automakers use automated-fiber-placement lines to integrate structural parts in mainstream models, as shown by General Motors' pilot trials. Federal R&D funding from the U.S. Department of Energy accelerates ductile carbon-fiber composite development for battery-pack housings. Regulations on fuel economy and consumer range expectations underpin sustained multi-year demand across volume platforms.

Accelerating Usage in Aerospace and Defense

Aerospace keeps its lead within the North America carbon fiber market because next-generation aircraft and hypersonic defense systems require high-modulus fiber. Toray supplies thermoset and thermoplastic prepregs for NASA's HiCAM program to improve fast-build composite wings. Collins Aerospace invested USD 200 million to enlarge Spokane carbon-carbon brake capacity, while GE Aerospace earmarked almost USD 1 billion for U.S. composite part production, reinforcing long-cycle demand visibility.

Regulatory-Driven Supply Risk for Raw Materials

Critical-material reviews by the White House and the Canadian government signal heightened scrutiny of PAN precursor imports. Policy shifts, such as export-control lists or stricter environmental permits, could pinch supply and raise compliance costs for the North America carbon fiber market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Utilization from Wind Energy Sector

- Expansion of High-Performance Sporting Goods

- Limited Recycling Infrastructure and Quality Variance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PAN commanded 91.83% of the North America carbon fiber market in 2024. The segment benefits from proven strength-to-weight ratios and well-understood supply chains. Petroleum-pitch and rayon, in contrast, are set to grow at an 18.91% CAGR because auto and construction buyers prioritize lower cost over ultimate tensile strength. Advanced Carbon Products LLC has developed a mesophase pitch carbon fiber precursor, offering a significant cost-saving opportunity compared to the conventional PAN-based production method.

Demand shifts favor suppliers that diversify precursor choice. Higher yield rates that exceed 70% for pitch versus 55% for PAN can cut per-kilogram costs when furnace energy remains constant. For mass-market uses such as pressure vessels or civil infrastructure, these economics make alternative precursors increasingly credible options.

Virgin fiber retained 76.21% share of the North America carbon fiber market size in 2024 because aerospace and defense require full traceability. Recycled fiber, however, is projected to post a 19.05% CAGR. Vartega reached mechanical properties comparable to virgin fiber but at half the cost and 96-99% lower CO2 footprint.

OEM acceptance of recycled intermediates is rising. Boeing's use of KyronTEX sidewall panels shows that strict cabin-interior requirements can be met with reclaimed content. Automotive injection-molding compounds with recycled strands now cut finished-part cost by up to 30%, spurring volume adoption.

The North America Carbon Fiber Market Report is Segmented by Raw Material (Polyacrylonitrile (PAN), Petroleum Pitch and Rayon), Type (Virgin Carbon Fiber (VCF), Recycled Carbon Fiber (RCF)), Application (Composite Materials, Textiles, and More), End-User Industry (Aerospace and Defense, Alternative Energy, and More), and Geography (United States, Canada, and More). The Market Forecasts are Provided in Terms of Volume (tons).

List of Companies Covered in this Report:

- A&P Technology, Inc.

- ACP Composites Inc.

- DowAksa

- Gurit Services AG

- Hexcel Corporation

- HS HYOSUNG USA

- Jiangsu Hengshen Co., Ltd.

- Mitsubishi Chemical Carbon Fiber and Composites Inc.

- Present Advanced Composites Inc.

- SGL Carbon

- Syensqo

- TEIJIN LIMITED

- Toray Industries Inc.

- Vartega Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand from Lightweight Vehicles

- 4.2.2 Accelerating Usage in Aerospace and Defense

- 4.2.3 Growing Utilization from Wind Energy Sector

- 4.2.4 Expansion of High-Performance Sporting Goods

- 4.2.5 Adoption in Hydrogen Storage Tanks for Heavy-Duty Mobility

- 4.3 Market Restraints

- 4.3.1 High Research and Development, and Capital Expenditure

- 4.3.2 Regulatory-Driven Supply Risk for Raw Materials

- 4.3.3 Limited Recycling Infrastructure and quality variance

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Raw Material

- 5.1.1 Polyacrylonitrile (PAN)

- 5.1.2 Peroleum Pitch and Rayon

- 5.2 By Type

- 5.2.1 Virgin Carbon Fiber (VCF)

- 5.2.2 Recycled Carbon Fiber (RCF)

- 5.3 By Application

- 5.3.1 Composite Materials

- 5.3.2 Textiles

- 5.3.3 Micro-electrodes

- 5.3.4 Catalysis

- 5.4 By End-user Industry

- 5.4.1 Aerospace and Defense

- 5.4.2 Alternative Energy

- 5.4.3 Automotive

- 5.4.4 Construction and Infrastructure

- 5.4.5 Sporting Goods

- 5.4.6 Other End-user Industries (Marine and Maritime)

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

- 5.5.4 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 A&P Technology, Inc.

- 6.4.2 ACP Composites Inc.

- 6.4.3 DowAksa

- 6.4.4 Gurit Services AG

- 6.4.5 Hexcel Corporation

- 6.4.6 HS HYOSUNG USA

- 6.4.7 Jiangsu Hengshen Co., Ltd.

- 6.4.8 Mitsubishi Chemical Carbon Fiber and Composites Inc.

- 6.4.9 Present Advanced Composites Inc.

- 6.4.10 SGL Carbon

- 6.4.11 Syensqo

- 6.4.12 TEIJIN LIMITED

- 6.4.13 Toray Industries Inc.

- 6.4.14 Vartega Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment