PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1637878

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1637878

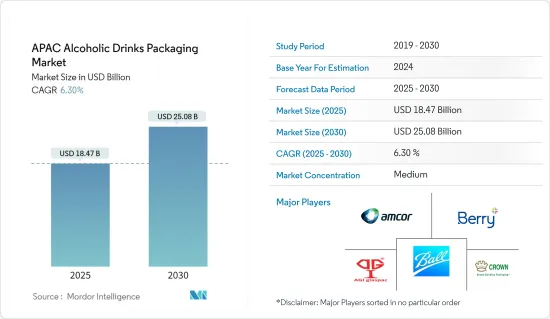

APAC Alcoholic Drinks Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The APAC Alcoholic Drinks Packaging Market size is estimated at USD 18.47 billion in 2025, and is expected to reach USD 25.08 billion by 2030, at a CAGR of 6.3% during the forecast period (2025-2030).

The demand for bottles and cans in beverage packaging is expected to grow as alcoholic beverage consumption rises in the region. Bottles and cans are more convenient to transport and store, making them popular among customers. Due to these factors, the demand for bottles in the Asia-Pacific alcoholic drinks packaging market is expected to increase.

Packaging has been essential in market expansion, with alcoholic beverage makers offering diverse products. Consumer expenditure on recreational activities has increased, as has societal acceptability, resulting in a steady increase in demand for alcoholic drink goods, impacting the packaging industry.

Glass has emerged as one of the fastest-growing alcohol packaging materials due to its recyclability, reusability, and neutral reactivity. Also, the rising popularity of metal cans drives the alcohol packaging market. Metal cans are packaging containers for storing and distributing alcoholic beverages. Its strength and stiffness make filling cans faster and easier without losing alcohol.

Furthermore, various factors influence the alcohol market in the region, including festivities, urbanization, women's empowerment, rising numbers of young people who tend to socialize, etc, push the market growth. Moreover, a lot of growth from new alcoholic drinks categories like light beer, wines, light alcoholic beverages, liqueurs, and single malts also pushed the packaging market in the region over the forecast period.

APAC Alcoholic Drinks Packaging Market Trends

Significant Growth in Metal Packaging to Boost the Market

- The market for alcoholic beverages packaging research market segmentation based on several materials such as plastic, paper, glass, and metal. It also covers products such as bottles, cans, pouches, cartons, and similar containers. Furthermore, the market analysis considers several factors, including sustainability, beverage product production rates, supply and demand, and the influence of pandemics on the market.

- Ball Corporation, Amcor Group Gmbh, Berry Global Inc., and other companies foresee a significant increase in their metal packaging business in India. Because of their sustainability, new categories like whiskey, wine, and hard spirits have moved to aluminum cans.

- Beer enthusiasts and brewers have also recognized the benefits of cans in maintaining the quality and freshness of the beverage. Cans offer superior protection against light and oxygen, which can degrade beer over time. Additionally, metal cans are highly recyclable, requiring less energy than glass bottle recycling. As the region strives to build a greener future, the beer industry's shift toward cans aligns with the nation's sustainability goals.

- Furthermore, businesses are investing in the future of metal packaging because they understand the significant impact of choosing endlessly recyclable beverage packaging on communities and the environment. Companies actively seek expanded categories in India, encompassing a considerably broader range of alcoholic beverages. The companies also closely examine the regulatory developments and expect a favorable environment for cans.

- Engineering Exports Promotion Council India stated India's net export value for aluminum and related products in 2023 was USD 8.8 billion. Aluminum production will experience economies of scale and cost-effectiveness as its export value rises. This might lead to more affordable packaging options for alcoholic beverages, making it a more desirable choice for manufacturers.

- Alcohol producers operating across the region are focused on launching alcoholic beverages in new packages. For instance, in March 2024, United Breweries Limited (UBL) announced the launch of Queenfisher beer in cans. Queenfisher Beer is an all-women initiative, from formulating the limited-edition Queenfisher can brewing it by women brewers.

Beer is expected to take a significant share of the market.

- Beer consumption has risen in the last few years. With over 20 million people reaching the legal drinking age yearly, India remains one of the world's foremost beer markets. United Breweries, India's largest beer manufacturer and maker of the well-known Kingfisher brand, has recently released their latest Kingfisher Instant Beer. The product is packaged in a box with two sachets.

- The glass bottle with a crown closure is the traditional beer packaging in the region. Because glass is widely utilized in alcohol packaging, demand is likely to rise throughout the forecast period. Furthermore, glass prices substantially influence the margin profile of alcohol industries, which swings in response to crude oil price fluctuations.

- Furthermore, gluten-free beers are becoming increasingly popular in this region. Beer consumption is also increasing at over 6% per year in China, India, and Vietnam. As a result, rising innovation in tastes and preparations is anticipated to stimulate beer demand, resulting in beer cans' growth.

- According to the National Bureau of Statistics of China, close to 4 million kiloliters of beer was produced in China in July 2023 which was 2.54 million kiloliters in December 2022. Due to the increase in beer production, packaging businesses may spend money on R&D to develop creative and environmentally friendly packaging options. The quality and appeal of alcoholic beverage packaging in Asia will be improved through eco-friendly packaging, new designs, and materials.

- Moreover, in March 2024, Singapore-founded Lion Brewery Co. is elevating the country's craft beer presence on the global stage by breaking new ground. They are the first craft brewery to pioneer a canned nitro stout with in-line nitro technology and the first Singaporean craft beer to be distributed in Dubai. This marks the first time a Singaporean craft beer brand has produced a canned Nitro Stout beer.

APAC Alcoholic Drinks Packaging Industry Overview

The Asia-Pacific alcoholic drinks packaging market is moderate with the presence of major players. Some of the major players in the market are Amcor Group GmbH, Crown Holdings, Inc., Ball Corporation, AGI Glaspac, Berry Global Inc., and others. Some recent strategic initiatives made in this sector are:

August 2023 - Crown Holdings Inc. announced the acquisition of Helvetia Packaging AG, a beverage can and end manufacturing facility. The acquisition of the Saarlouis plant will expand Crown's beverage can network, with an annual capacity of around 1 billion units. As part of the agreement, Crown will take over the existing Helvetia customer base and associated contracts at closing.

July 2023 - Amcor Rigid Packaging (ARP) launched 100% recycled polyethylene terephthalate (rPET) packaging for Ron Rubin Winery's new BLUE BIN wine range. The range is 750 ml in a bottle. In addition to reducing greenhouse gas emissions compared to conventional wine packaging, rPET packaging offers many environmental advantages.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Sustainable Packaging

- 5.1.2 Increasing Consumption of Alcoholic Drinks in Asia

- 5.2 Market Restraints

- 5.2.1 Government Regulation for Plastic Usage

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Plastic

- 6.1.2 Paper

- 6.1.3 Metal

- 6.1.4 Glass

- 6.2 By Product Type

- 6.2.1 Bottles

- 6.2.2 Cans

- 6.2.3 Pouches

- 6.2.4 Carton

- 6.3 By Country

- 6.3.1 China

- 6.3.2 India

- 6.3.3 Japan

- 6.3.4 Singapore

- 6.3.5 Australia and New Zealand

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.2 Mondi Group

- 7.1.3 Crown Holdings, Inc.

- 7.1.4 Gerresheimer AG

- 7.1.5 Hualian Glass Bottle

- 7.1.6 Ball Corporation

- 7.1.7 AGI Glaspac

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET