PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689861

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689861

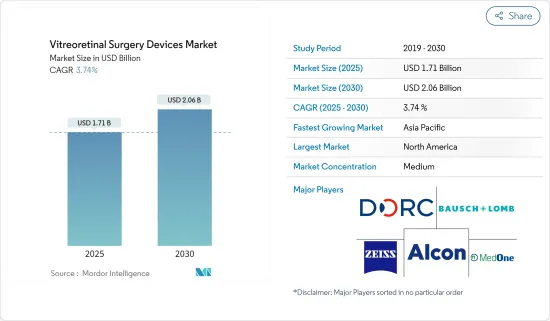

Vitreoretinal Surgery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Vitreoretinal Surgery Devices Market size is estimated at USD 1.71 billion in 2025, and is expected to reach USD 2.06 billion by 2030, at a CAGR of 3.74% during the forecast period (2025-2030).

The COVID-19 pandemic was an unprecedented health concern and adversely affected various surgical procedures. Due to regulatory authorities' strict guidance to prevent any non-emergent surgeries, the volume of surgeries drastically decreased throughout the pandemic. For instance, as per the research study published by PubMed Central in September 2021, the COVID-19 pandemic significantly impacted the clinical care for diabetic retinopathy during the early phase. Thus, COVID-19 had an impact on the studied market. However, with the decreasing number of COVID-19 cases and wide-scale vaccination programs, the studied market was expected to regain its pre-COVID-19 level potential over the coming years.

The increasing incidence of eye disorders such as diabetic retinopathy and macular holes and the increasing geriatric population is attributed to driving the growth of the studied market over the forecast period. For instance, according to the research study published in May 2021 by the National Library of Medicine, diabetic retinopathy remained a common complication of diabetes mellitus and a leading cause of preventable blindness in the adult working population. Among the people with diabetes mellitus, the prevalence of diabetic retinopathy was 22.27%, 6.17% for vision-threatening diabetes mellitus (VTDR), and 4.07% for clinically significant macular edema (CSME).

Many eye disorders are age-associated, like macular degeneration. With the growing global geriatric population, the burden of eye diseases is expected to increase, which is likely to augment the growth of the studied market. For instance, according to World Population Aging Highlights United Nations 2022 report, it was found that in 2022 there were 771 million people aged 65 years or over globally. The older population is projected to reach 994 million by 2030 and 1.6 billion by 2050. As older adults are often associated with eye disorders such as diabetic retinopathy and macular holes, the rising geriatric population is expected to enhance the adoption of vitreoretinal surgery devices to treat such diseases.

The companies are actively involved in new product launch developments and collaborations to expand their footprint. For instance, in January 2021, DORC received Health Canada approval of TissueBlue for Staining of the ILM During Vitreoretinal Surgery. TissueBlue is the first dye approved by Health Canada to aid in ophthalmic surgery by selectively staining the internal limiting membrane (ILM). Such development is expected to drive the market's growth over the forecast period.

Hence, owing to the factors such as the increasing incidence of eye disorders such as macular degeneration, diabetic retinopathy, and macular holes and the increasing geriatric population, the vitreoretinal surgery devices market is expected to grow over the forecast period. However, the side effects of the procedures are expected to restrain the market's growth during the forecast period.

Vitreoretinal Surgery Devices Market Trends

Posterior Vitreoretinal Surgery is Expected to Hold a Significant Market Share Over the Forecast Period

Pars plana vitrectomy (PPV) is a commonly employed technique in vitreoretinal surgery that enables access to the posterior segment for treating conditions such as retinal detachments, vitreous hemorrhage, endophthalmitis, and macular holes in a controlled, closed system. The high prevalence of diseases/disorders associated with the posterior segment of the eye, such as diabetic retinopathy and posterior vitreous detachment, is driving the demand for posterior vitrectomy (surgical procedures used to treat diseases associated with retina and vitreous), which is expected to have a significant impact on the growth of posterior vitreoretinal surgery segment.

For instance, according to an article published by PLOS ONE in August 2021, diabetic retinopathy (DR) is said to be one of the most common serious complications of diabetes mellitus. It is defined as damage to the blood vessels of the eyes caused by high blood glucose levels. The source also stated that the pooled prevalence of this complication in Germany ranges from about 10% to 30%, depending on the healthcare sector. Thus, the high prevalence of diabetic retinopathy is expected to drive segmental growth.

Additionally, according to an article published by WebMD in July 2021, the annual incidence of retinal detachment is approximately one in 10,000 or about 1 in 300 over a lifetime. Hence, the posterior vitreoretinal surgery segment is expected to have a major share of the vitreoretinal surgery devices market. Moreover, as these diseases are often associated with older adults, the rising geriatric population is also expected to enhance market growth.

Therefore, due to the factors such as the high prevalence of diseases/disorders associated with the posterior segment of the eye, such as diabetic retinopathy and posterior vitreous detachment, the posterior vitreoretinal surgery segment is expected to have a significant market share over the forecast period.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

North America will hold a significant share of the vitreoretinal surgery devices market. It is expected to show a similar trend over the forecast period, owing to the region's high prevalence and burden of eye diseases and the increasing geriatric population. For instance, according to the article published by BMC Ophthalmology in May 2022, diabetic retinopathy (DR) is considered a potentially blinding complication of diabetes mellitus that affects almost about 28% of diabetics in the United States every year. Diabetic retinopathy can typically be detected with annual screening, but many Americans with diabetes mellitus do not receive routine surveillance to prevent visual impairment or blindness. The source also stated that undetected diabetic retinopathy might be particularly prevalent in hospital settings, where it is estimated to have a prevalence of around 44% among diabetic inpatients, out of which over half were previously undiagnosed.

Moreover, The rising geriatric population in the country is also expected to enhance the market growth as vitreoretinal surgeries are often recommended to treat eye disorders that mainly occur in older people. For instance, according to the data updated by the United Nations Population Fund dashboard in 2022, an estimated 19% of Canada's total population was 65 years or older in 2022.

The companies are actively involved in product launch developments, innovation, partnerships, and collaborations to expand their footprint. For instance, in March 2022, Carl Zeiss MeditecAG received 510(k) premarket approval from the United States Food and Drug Administration (FDA) for their QUATERA 700 device, which is indicated for the emulsification and removal of cataracts and anterior segment vitrectomy. Such development is expected to drive the market's growth over the forecast period.

Therefore, the factors such as the high prevalence and burden of eye diseases in the region and the increasing geriatric population are expected to drive market growth during the forecast period.

Vitreoretinal Surgery Devices Industry Overview

The Vitreoretinal Surgery Devices Market is moderate due to the presence of companies operating globally and regionally. The competitive landscape includes analysis of companies based on product launches, acquisitions, collaboration, and agreements that hold the market shares and are well known, including Dutch Ophthalmic Research Center International BV, Bausch & Lomb Inc., OCULUS Optikgerate GmbH, and MedOne Surgical Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidence of Eye Disorders

- 4.2.2 Increasing Geriatric Population

- 4.3 Market Restraints

- 4.3.1 Side Effects of the Procedures

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Perfluoro Carbon Liquids

- 5.1.2 Endoillumination Instruments

- 5.1.3 Vitreoretinal Prefilled Silicone Oil Syringes

- 5.1.4 Virectomy System

- 5.1.5 Other Product Types

- 5.2 By Surgery Type

- 5.2.1 Anterior Vitreoretinal Surgery

- 5.2.2 Posterior Vitreoretinal Surgery

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dutch Ophthalmic Research Center International BV

- 6.1.2 Bausch & Lomb Inc.

- 6.1.3 OCULUS Optikgerete GmbH

- 6.1.4 BVI

- 6.1.5 MedOne Surgical Inc.

- 6.1.6 Alcon

- 6.1.7 Carl Zeiss

- 6.1.8 Topcon Corporation

- 6.1.9 Hoya Corporation

- 6.1.10 GEUDER AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS